|

市場調査レポート

商品コード

1940782

米国の水道メーター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United States Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の水道メーター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

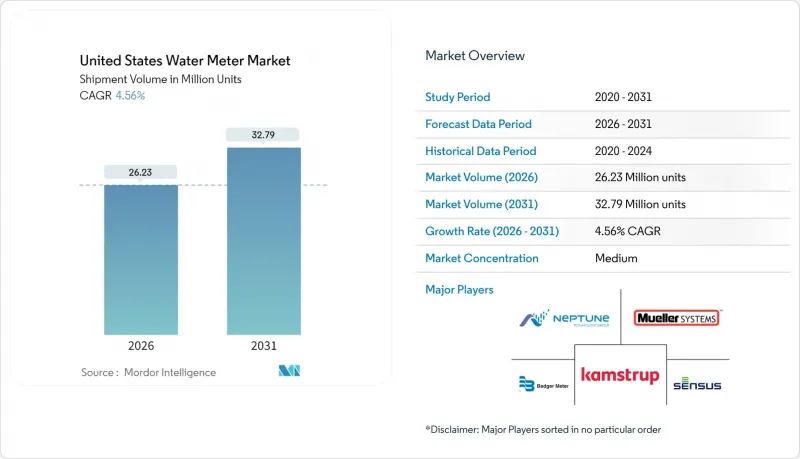

米国における水道メーター市場は、2025年に2,509万ユニットと評価され、2026年の2,623万ユニットから2031年までに3,279万ユニットに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは4.56%と見込まれています。

連邦政府による継続的な資金提供、干ばつによる節水要請、そして事後対応型保守から予知保全型資産管理への移行が、この上昇傾向を支えています。公益事業者は、収益化されていない水の削減、規制報告義務の充足、そしてより広範なスマートシティ目標を支えるデータプラットフォーム構築のため、先進的な計測システムの導入を優先しています。ベンダー戦略は現在、測定可能な運用上の利益を示す統合型ハードウェア+分析ソリューションの提供に重点を置いており、初期メーターコストを超えた差別化された価値を創出しています。通信技術の革新、特にセルラーNB-IoTおよびLTE-Mは、地方地域における導入障壁を低減し、次世代メーターの対象基盤を拡大しています。

米国の水道メーター市場の動向と洞察

老朽化した水道インフラの更新サイクル

慢性的な配管故障(年間25万件の破損)により、水道事業者は1990年代に設置された水道メーターを含む資産の全面的な更新を迫られています。寿命を迎えた機械式メーターは、20年間校正が不要な超音波式デバイスへの切り替えの好機となります。これによりライフサイクルコスト全体が削減されます。ベテランオペレーターの相次ぐ退職により、現場の専門知識が減少する中、分析技術で補う自動データ収集の必要性がさらに高まっています。連邦補助金と更新プログラムを連動させることで、水道事業者は単なる同型交換を避け、今後数十年にわたり将来を見据えたスマートインフラを導入しています。

連邦IIJA資金とメーター更新の連動

インフラ投資雇用法(IIJA)は水道事業に550億米ドルを割り当てており、その適格基準では効率改善を証明可能な計測技術を導入する公益事業者を明確に優遇しています。これは処理施設中心だった従来の連邦プログラムからのパラダイムシフトです。双方向計測は公平な投資目標達成のコンプライアンス指標として機能し、補助金申請者は機械式メーターでは提供できない配水システム性能と顧客サービス基準における定量化可能な向上を証明せざるを得ません。

小規模事業体における初期設備投資負担

3,300接続未満の事業者は、調達規模や内部プロジェクトチームが不足しているため、メーター1台あたりのコストが500米ドルを超え、大規模事業者の2倍となります。債務容量が限られているため、従来の債券による資金調達は往々にして利用できません。メーター所有権をベンダーが保持し月額料金を請求する「サービスとしてのメーター(Metering-as-a-Service)」契約が、資本支出を運営予算に移行させ、性能リスクを供給者に移転する実行可能な代替手段として台頭しています。

セグメント分析

スマート水道メーターはCAGR5.53%で拡大していますが、2025年時点でも機械式メーターが米国の水道メーター市場シェアの64.15%を占めています。水道事業者は、超音波式の高精度性、統合型漏水検知機能、および出張点検を削減するリモートファームウェア更新を重視しています。カムストループ社のflowIQ 2200は、機械式メーターでは計測できなかった1世帯あたり1日約6ガロン(約22.7リットル)の漏水を捕捉します。ラスベガス・バレー水道局による40万戸の住宅用メーター交換評価では、運用コスト削減により5年以内に高単価を相殺できることが示されました。一方、初期費用の低さをデータインテリジェンスより優先する資金制約のある地域では機械式メーターが継続使用されていますが、交換サイクルの到来により、これらの事業体も同様の性能格差に直面することになります。

米国の水道メーター市場におけるスマートメーターの規模は、実証可能な効率指標に資金を連動させる連邦助成制度の後押しを受け、2031年までに1,447万台に達すると予測されています。超音波式プラットフォームは寿命にわたって校正を維持するため、ドリフトが生じ定期的なベンチテストを必要とする機械式部品とは対照的に、保守予算を削減します。この信頼性の優位性は、労働力減少に直面する水道事業者に共感を呼びます。メーター修理の減少は人員削減ニーズの低下につながります。スマートシティプラットフォームが水道データを統合するにつれ、リアルタイム消費量情報の戦略的意義が機械式設置ベースを継続的に侵食していくでしょう。

2025年時点で自動検針システム(AMR)は米国の水道メーター市場規模の57.12%を占めていましたが、公益事業者が双方向アーキテクチャへ移行する中、高度計量インフラ(AMI)が6.05%という最速の成長率を示しています。AMIは間隔データの詳細化、遠隔遮断、ネットワーク全体のファームウェア更新をサポートし、包括的な資産管理環境を構築します。タコマ公共事業局はAMIを活用し、時間帯別料金制度を導入した結果、6ヶ月以内に測定可能な消費量シフトを達成しました。

公益事業経営陣は規制順守も指摘しています。多くの州委員会が干ばつ対策計画の検証に時間単位または日単位の検針を義務付けているためです。自動検針システム(AMR)は人口密度が低い地域では引き続き有用ですが、チップセットのコスト削減とセルラー通信網の拡大によりコスト差は縮小傾向にあります。予測期間において、AMIが提供するリアルタイムの状況把握機能は、非収益水(NRW)を積極的に管理しようとする業界の動きと合致し、シェア拡大が継続すると見込まれます。

米国の水道メーター市場は、メータータイプ(スマート水道メーターと機械式/基本メーター)、通信技術(高度計量インフラ、自動検針、手動/巡回検針)、ネットワーク接続方式(セルラー、RFメッシュ/900MHz、PLC/有線)、エンドユーザーセクター(住宅用など)、公益事業規模区分(ティア1、ティア2、ティア3)で分類されます。市場予測は数量(台数)ベースで提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 支援的な州規制と節水義務

- 老朽化した水道インフラの更新サイクル

- 公益事業会社による非収益水削減への取り組み

- スマートシティおよびIoT導入の波

- NB-IoTのカバー範囲拡大による地方部への展開促進

- 連邦IIJA資金はメーター更新に紐づいています

- 市場抑制要因

- 小規模公益事業体における先行設備投資負担

- サイバーセキュリティおよびデータプライバシーリスク

- 超音波式メーターの半導体供給の変動性

- 公益事業従事者の分析スキル不足

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- マクロ経済動向の影響

第5章 市場規模と成長予測

- メータータイプ別

- スマート水道メーター

- 機械式/基本メーター

- コミュニケーションテクノロジー別

- 高度計量インフラ(AMI)

- 自動検針システム(AMR)

- 手動/歩行検針

- ネットワーク接続別

- セルラー通信(LTE-M/NB-IoT)

- RFメッシュ/900MHz

- PLC/有線

- エンドユーザーセクター別

- 住宅

- 商業

- 産業

- 自治体ユーティリティ

- 公益事業規模別

- Tier-1(40万接続超)

- Tier-2(4万5,000~40万)

- Tier-3(4万5,000接続未満)

第6章 競合情勢

- 市場集中度分析

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Badger Meter, Inc.

- Sensus USA Inc.

- Neptune Technology Group Inc.

- Mueller Systems, LLC

- Kamstrup Water Metering LLC

- Diehl Metering LLC USA

- Itron, Inc.

- Aclara Technologies LLC

- Landis+Gyr Technology Inc.

- Master Meter, Inc.

- Zenner USA, Inc.

- Metron-Farnier, LLC

- Carlon Meter, Inc.

- Elster AMCO Water, LLC

- Datamatic, Inc.

- Spire Metering Technology, LLC

- Arad Technologies USA, Inc.

- Honeywell International Inc.

- Xylem Inc.

- B Meters USA, Inc.

- Trimble Water, Inc.

- SmartCover Systems, Inc.