水道メーター産業- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Water Meter Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 161 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683857

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

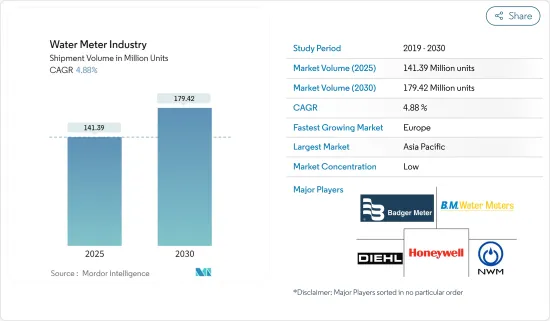

水道メーター業界は、出荷台数ベースで2025年の1億4,139万台から2030年には1億7,942万台に成長し、予測期間(2025年~2030年)のCAGRは4.88%と予測されています。

水道メーターは、住宅、商業、工業など様々な最終用途事例で使用される水の流量と量を測定するために使用される装置を指します。長年にわたり、水道メーター技術は大きく進化してきました。最も一般的に使用されている水道メーターの種類には、流速計、変位計、電磁式水道メーター、超音波式水道メーターなどがあります。

主なハイライト

- 長年にわたり、人口増加、急速な都市化と工業化、一人当たりの消費量の増加により、水の消費量は大幅に増加しています。例えば、米国の芝生管理サービスプロバイダーであるLawnStarterによると、2022年の一人当たりの水消費量は米国がトップ(2,842立方メートル)で、カナダ、ニュージーランド、コスタリカなどの国がこれに続きます。

- 消費量の増加の結果、近年いくつかの地域が水不足の問題に直面し始めており、水の浪費を最小限に抑える必要性や水の保全に対する需要の高まりといった動向が生まれています。

- さらに、技術の進歩や、消費者や企業による節水への政府や個人の取り組みの高まりも、調査対象市場の成長に寄与しています。

- さらに、使用事例と適用領域の拡大により、新技術が広く受け入れられるようになり、革新的な計量ソリューションの開発につながっています。例えば、機械式、電磁式、超音波式は水道メーター市場で広く使用されている主要技術の一つです。

- しかし、スマート水道メーターのコストが高いことや、認知度が低いために設置率が低いことなどが、調査した市場の成長にとって依然として大きな課題となっています。

- さらに、高速接続などのスマート水道メーターをサポートするインフラの不足も、特に新興国市場の成長を妨げています。

水道メーター業界の動向

大きく成長するスマート水道メーター

- スマート水道メーターは、適切な請求と効果的な水管理を促進するために、様々な消費ポイントからの水の使用量を測定し、公益事業者に伝達することができる装置です。スマートメーターは通常、センサーと電子計算ユニット(ECU)を備え、メーターと供給業者間の通信を容易にします。機械的な水道メーターとは異なり、これらのメーターは、より正確な測定を提供する電磁または超音波技術を通じて水の使用量を追跡することができます。

- スマート水道メーターの普及を促進する主な特徴には、高度計測インフラ(AMI)システムの存在があり、水道事業者は、流量や圧力の異常など他のマトリックスとともに、リアルタイムの水道使用量を遠隔で追跡することができます。また、空室や改ざんも特定できるため、漏水による損失を追跡するための非常に効果的なソリューションとなります。スマート水道メーターは、ダイナミックな水道料金の請求に有利で、毎月手作業で監視する必要がなくなります。また、リアルタイムでウェブベースのメータリングをサポートし、電力会社が自動的に請求書を作成し、特定の時間内に消費者と共有できるようにします。

- 例えば、アメリカン・ウォーターは、廃水の処理と汲み上げに3億2,200万米ドルを投資しており、水の消費量を追跡し、水の浪費を減らすことが重要になってきています。また、いくつかの使用事例は、無収水量(NRW)問題の削減における高度な技術ソリューションの利点を裏付けています。

- 例えば、フィリピンのマニラ首都圏東部地区の大手水道供給会社であるマニラ・ウォーターによると、ネットワークの再構成、メーター管理プログラム、供給量の正確な測定、積極的な供給・圧力管理などの積極的な技術ソリューションの採用により、同社は1997年に63%だったNRWを、2022年には12.69%まで削減し、これはアジアで最も低い数値の1つとなっています。このように、技術改善、社会意識、水危機問題の高まりは、市場の成長にプラスの影響を与えると予想されます。

- また、スマートメーターは、IoT対応の流量計や、遠隔操作可能なバルブが組み込まれ、使用量に関するリアルタイム分析を提供するなどの機能により、水の消費量を調整するのに役立ちます。様々な調査によると、スマート水道メーターが施設内に設置された場合、20~50%の範囲で削減されることが示唆されています。

- スマート水道メーターは、新技術の採用も顕著に伸びており、メーターの機能と使用事例の拡大に役立っています。例えば、シリコンラボの低デューティサイクルの最適化と独創的な超低消費電力SoC設計は、スマート水道メーターの動作寿命を大幅に向上させ、バッテリーを使用した場合、10年に達します。さらに同社は、独自の無線プロトコルであるサブGHz帯Wi-SUNメッシュなどのソリューションも提供し、スマート水道メーターの普及を最大化しています。

欧州が大きな市場シェアを占めると予想される

- 英国は、効率化を推進し、水道業界に持続可能性をもたらすための政府と公益事業供給者からのいくつかのイニシアチブによって、欧州地域における水道メーターの主要な採用国の一つであり続けると予想されています。さらに、同国は干ばつのリスクの高まりに直面しており、国家インフラ委員会は最近、水消費を管理し、十分な需要削減を実現し、同国の干ばつ回復力を向上させるために効率を高めるために、水道業界における高度計測インフラ(AMI)の展開を推進するよう促しました。

- フランスは水道メーターをいち早く導入した国のひとつであり、いくつかの大手ベンダーがフランスに進出しています。例えば、大手電力会社のヴェオリアは、リヨンとイル・ド・フランスでの提携を含め、フランスと欧州で300万台のTeleOスマートメーターを設置しました。同様に、スエズ・グループは、ダンケルク、ル・マンなどで水道メーターON'connectを展開しました。フランスでは、スマート水道メーターを支えるインフラも大きく発展しており、市場の成長をさらに後押ししています。例えば、2023年2月、スウェーデンのIoT事業者であるNetmoreは、フランスでLoRaWANネットワークの展開を開始し、スマート水道メーターやその他のIoT、大規模ユーティリティ・プロジェクトをターゲットとしています。

- 近年、スペインの多くの都市が水危機に直面し始めているため、干ばつと水不足はスペインで高まる懸念の一つとなっています。このため、公益事業供給者や政府は、より良い水管理のための主要な取り組みや技術の導入に関心を寄せています。生態系移行省による最近の報告書によると、スペインの約27%が「警戒」または「緊急」に分類される干ばつに見舞われています。

- このような問題に対応するため、スペイン政府は2023年5月、最も暑く乾燥した月によって悪化する長引く干ばつに対処するため、消費者と農家を支援する22億ユーロ(~19億英ポンド、~23億4,000万米ドル)の計画を承認しました。投資とは別に、節水イニシアチブ全体を成功させるために、関係当局や団体が発行したガイドラインに従うよう消費者に奨励するために、政府や電力会社によっていくつかの取り組みも行われています。水道メーターは、このようなイニシアチブをサポートする重要な技術の1つと考えられているため、調査された市場は積極的な成長を示すと予想されています。

- ドイツは、欧州地域における水道メーターの重要なマーケットプレースの一つです。同国は、堅牢な水道インフラを有しており、随時アップグレードが行われているため、市場情勢に機会を生み出しています。例えば、欧州国家計量機関協会(EURAMET)によると、欧州地域ではドイツだけで約4,500万個の水道メーターが設置されており、その生産額は約10億ユーロ(~10億6,000万米ドル)です。さらに、漏水検知や水使用量に関する情報への便利なアクセスに対する消費者の需要が高まっていることから、同国ではスマート水道メーターの普及がさらに進むと予想されています。

水道メーター業界の概要

水道メーター市場は非常に断片化されており、Badger Meter Inc.、Diehl Metering GMBH(Diehl Stiftung &Co. KG)、Bm Water Meters、Ningbo Water Meter(Group)、Honeywell International Inc.などの大手企業が存在します。市場のプレーヤーは、製品提供を強化し、持続可能な競争優位性を獲得するために、パートナーシップや買収などの戦略を採用しています。

- 2023年4月-Badger Meter Inc.は、テキサス州ヒューストンで開催されるTexas Water 2023において、今日の上下水道事業者が直面する課題に対処するためのスマートウォーターソリューションの包括的ポートフォリオを展示すると発表しました。同社は、Eシリーズ超音波メータ、BEACON Software as a Serviceなど、水質、配水、分析モニタリングの全機能について説明する予定。

- 2023年5月-Diehl Metering GmbHは、英国のSouth West Water社が、グリーン・リカバリー・イニシアチブの一環として、Diehl Metering社およびLoRaWANのスペシャリストであるNetmore社との提携を選択したと発表しました。このプロジェクトの焦点は、効率性と持続可能性の向上を目指したAMI(高度計測インフラ)ネットワークの開発です。5年間の契約により、同社は約7万6,000台のALTAIR水道メーターにLoRaWAN接続を装備し、インテリジェントな監視と漏水検知のためのIoT接続の実装を支援します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 技術の進化

- 産業バリューチェーン分析

- マクロ動向が市場に与える影響

第5章 市場力学

- 市場促進要因

- 水道インフラ整備への投資拡大

- 第二世代水道メーターの普及率拡大

- 市場の課題/抑制要因

- 高い設置コストと長い投資回収期間

- 水道メーターの交換サイクルの長期化

第6章 市場セグメンテーション

- タイプ別

- スマート水道メーター

- 基本型水道メーター

- 地域別

- 北米

- 米国

- カナダ・中米

- 欧州

- 英国

- フランス

- スペイン

- イタリア

- アジア

- 中国

- オーストラリア・ニュージーランド

- 日本

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Badger Meter Inc.

- Diehl Metering GMBH(Diehl Stiftung & Co. KG)

- BM Water Meters

- Ningbo Water Meter(Group)Co. Ltd

- Honeywell International Inc.

- Sensus USA Inc.(Xylem Inc.)

- Master Meter Inc.(ARAD Group)

- Neptune Technology Group Inc.

- Tongtuo Water Meter Factory

- Suntront Tech Co. Ltd

- Azbil Kimmon Co., Ltd.

- Itron Inc.

- Kamstrup As

- Landis+GYR Group AG

第8章 市場の将来展望

目次

The Water Meter Industry in terms of shipment volume is expected to grow from 141.39 million units in 2025 to 179.42 million units by 2030, at a CAGR of 4.88% during the forecast period (2025-2030).

Water meter refers to devices used to measure the flow and volume of water used across various end-use cases, including residential, commercial, industrial, etc. Over the years, the water meter technology has evolved significantly. The most common types of water meters in use include velocity, displacement, and electromagnetic or ultrasonic water meters.

Key Highlights

- Over the years, water consumption has increased significantly due to population growth, rapid urbanization and industrialization rates, and growing per capita consumption. For instance, according to LawnStarter, an American lawn maintenance service provider, in 2022, the United States was the leading country in per-capita water consumption (2,842 cubic meters), followed by countries such as Canada, New Zealand, Costa Rica, etc.

- As a result of the growing consumption, several regions have started facing water shortage issues in recent years, giving rise to trends such as the need to minimize water wastage and the growing demand for water preservation, which is anticipated to remain among the key drivers for the growth of the market studied during the forecast period.

- Moreover, technological advancements and rising government and individual efforts by consumers and businesses to save water also contribute to the growth of the market studied.

- Moreover, owing to the expanding use cases and application area, new technologies are gaining widespread acceptance, leading to the development of innovative metering solutions. For instance, instance Mechanical, Electromagnetic, and Ultrasonic are among the key technologies widely in use in the water meter market.

- However, factors such as a higher cost of smart water meters and a lower installation rate, owing to a lower awareness, remain among the major challenging factors for the growth of the market studied.

- Additionally, the lack of supporting infrastructure for smart water meters, such as high-speed connectivity, also hampers the growth of the market studied, especially across developing regions.

Water Meter Industry Trends

Smart Water Meter to Witness Major Growth

- Smart water meters are devices that can measure and communicate water usage from various consumption points to the utility provider to facilitate proper billing and effective water management. Smart meters are usually equipped with sensors and an electronic computing unit (ECU) that facilitates communication between the meter and the supplier. Unlike mechanical water meters, these meters are more capable of tracking water usage through electromagnetic or ultrasonic technologies that provide more accurate measurements.

- Major features driving the adoption of smart water meters include the presence of an advanced metering infrastructure (AMI) system, which enables utility providers to remotely track real-time water consumption, along with other matrices, including flow and pressure anomalies. They can also locate vacancies and tampering, making them a highly effective solution to track losses caused by leaks. Smart water meters favor dynamic water billing, eliminating the need for manual supervision every month. They also support real-time, web-based metering to help utility providers automatically generate bills and share them with consumers within a specific time.

- Expanding water-stressed areas, especially in arid regions across the world along with treatment of waste water, For instance as of American Water invested 322 million USD in treatment and pumping for Waste Water, is driving the demand for smart water meters, as it is becoming important to track water consumption and reduce wastage of water. Several use cases also confirm the benefits of advanced technological solutions in reducing the issue of Non-Revenue Water (NRW).

- For instance, according to Manila Water, a major water supplier in the East Zone of Metro Manila, Philippines, the adoption of proactive technical solutions, including the reconfiguration of the network, meter management programs, accurate measurement of supply volumes, and the active supply and pressure management helped the company to reduce the NRW from 63% in 1997 to 12.69% in 2022, which is one of the lowest in Asia. Thus, technological improvements, social awareness, and the growing water crisis issue are expected to influence the market's growth positively.

- Smart meters also help in regulating water consumption owing to features such as IoT-enabled water flow meters, which come embedded with a valve that can be controlled remotely and provide real-time analytics about usage. Various surveys suggest a reduction in the range of 20-50% when smart water meters are installed within a facility.

- Smart water meters are also witnessing notable growth in the adoption of new technologies, helping expand the capability and use cases of these meters. For instance, Silicon Labs' Low Duty Cycle optimization and ingenious ultra-low power SoC design significantly enhance the operational life of smart water meters with ten years with a battery. Furthermore, the company also offers solutions such as proprietary wireless protocols sub-GHz Wi-SUN mesh to maximize the reach of smart water meters.

Europe is Expected to Hold Significant Market Share

- The United Kingdom is anticipated to remain among the leading adopters of water meters in the European region, driven by several initiatives from the government and utility suppliers to drive efficiency and bring sustainability to the water supply industry. Furthermore, with the country facing an increased risk of drought, the National Infrastructure Commission recently urged to drive the deployment of advanced metering infrastructure (AMI) within the water industry to take control of water consumption, deliver enough demand reduction, and increase efficiency to improve the country's drought resilience.

- France has been among the early adopters of water meters, and several major vendors are present in France. For instance, Veolia, a major utility company, installed three million TeleO smart meters in France and Europe, including partnerships in Lyon and Ile-de-France. Similarly, the Suez group rolled out its version of water meters, ON'connect, in Dunkirk, Le Mans, and elsewhere. The country is also witnessing significant developments in the supporting infrastructure of smart water meters, which further support the growth of the market studied. For instance, in February 2023, Netmore, a Swedish IoT operator, started rolling out a LoRaWAN network in France, targeting smart water metering and other IoT and large-scale utility projects.

- Drought and water scarcity are among the rising concerns in Spain as, in recent years, a number of cities in Spain have started facing a water crisis. This drives the attention of utility suppliers and the government toward the adoption of major initiatives and technology for the better management of water. According to a recent report by the Ecological Transition Ministry, around 27% of Spain is experiencing droughts classified as "alert" or "emergency," as water reserves in the country are only at 50% of capacity nationally.

- Responding to such issues, in May 2023, the Spanish government approved a EUR 2.2 billion (~GBP 1.9 billion and ~USD 2.34 billion) plan to help consumers and farmers cope with an enduring drought exacerbated by the hottest and driest months. Apart from the investments, several initiatives are also being undertaken by the government and utility suppliers to encourage the consumers to follow the guidelines issued by related authorities and organizations to make the entire water conservation initiative a success. As water meters are considered one of the key technologies that help support such initiatives, the market studied is anticipated to witness positive growth.

- Germany has been among the significant marketplaces for water meters in the European region. The country has a robust water supply infrastructure, which has witnessed time-to-time upgrades, thereby creating opportunities in the market's landscape. For instance, according to the European Association of National Metrology Institutes (EURAMET), across the European region, Germany alone has about 45 million water meters installed, and they also represent a production value of almost EUR 1 billion (~USD 1.06 billion). Furthermore, with the consumer demand for convenient access to leakage detection and information about water usage growing, the uptake of smart water meters is anticipated to grow further in the country.

Water Meter Industry Overview

The Water Meter Market is highly fragmented, with the presence of major players like Badger Meter Inc., Diehl Metering GMBH (Diehl Stiftung & Co. KG), Bm Water Meters, Ningbo Water Meter (Group) Co. Ltd, and Honeywell International Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- April 2023 - Badger Meter Inc. announced that it will showcase an inclusive portfolio of smart water solutions to address challenges facing today's water and wastewater utilities during Texas Water 2023 in Houston, Texas. The company will discuss the full range of water quality, distribution, and analytical monitoring capabilities, such as E-series Ultrasonic meters, BEACON Software as a Service, etc.

- May 2023 - Diehl Metering GmbH has announced that South West Water in the United Kingdom has chosen to partner with Diehl Metering and LoRaWAN specialist Netmore as part of its green recovery initiative. The focus of this project is the development of an AMI (Advanced Metering Infrastructure) network aimed at improving efficiency and sustainability. Under the five-year agreement, the company will equip approximately 76,000 ALTAIR water meters with LoRaWAN connectivity and help implement IoT connectivity for intelligent monitoring and leak detection.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Technology Evolution

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Investment in Water Infrastructure Upgradation Activities

- 5.1.2 Growth in Adoption Rate of Second-generation Water Meters

- 5.2 Market Challenges/Restraints

- 5.2.1 High Installation Cost and Longer ROI Period

- 5.2.2 Longer Replacement Cycle of Water Meters

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Smart Water Meter

- 6.1.2 Basic Water Meter

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada and Central America

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 France

- 6.2.2.3 Spain

- 6.2.2.4 Italy

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Australia and New Zealand

- 6.2.3.3 Japan

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Badger Meter Inc.

- 7.1.2 Diehl Metering GMBH (Diehl Stiftung & Co. KG)

- 7.1.3 BM Water Meters

- 7.1.4 Ningbo Water Meter (Group) Co. Ltd

- 7.1.5 Honeywell International Inc.

- 7.1.6 Sensus USA Inc. (Xylem Inc.)

- 7.1.7 Master Meter Inc. (ARAD Group)

- 7.1.8 Neptune Technology Group Inc.

- 7.1.9 Tongtuo Water Meter Factory

- 7.1.10 Suntront Tech Co. Ltd

- 7.1.11 Azbil Kimmon Co., Ltd.

- 7.1.12 Itron Inc.

- 7.1.13 Kamstrup As

- 7.1.14 Landis+GYR Group AG

8 FUTURE OUTLOOK OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 161 Pages

- 納期

- 2~3営業日