|

市場調査レポート

商品コード

1911452

紙および板紙包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Paper And Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 紙および板紙包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

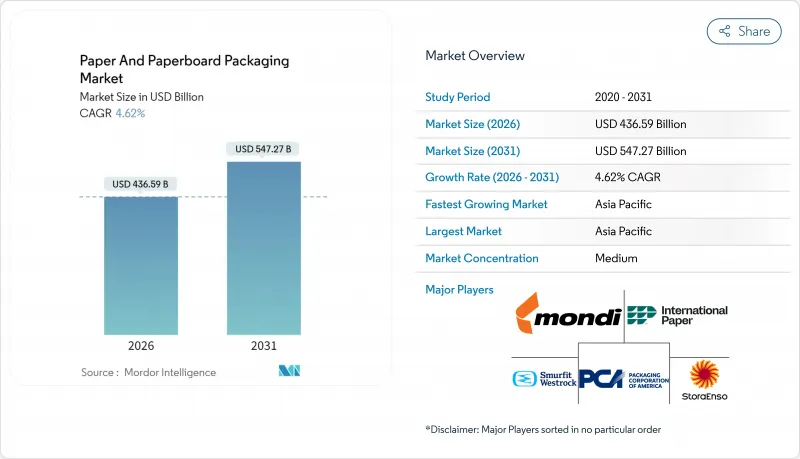

2026年の紙および板紙包装市場の規模は4,365億9,000万米ドルと推定され、2025年の4,173億1,000万米ドルから成長が見込まれます。

2031年の予測では5,472億7,000万米ドルに達し、2026年から2031年にかけてCAGR4.62%で拡大する見通しです。

需要は三つの構造的な追い風により拡大しています:欧州連合におけるリサイクル義務の強化、電子商取引における保護輸送形態の必要性、そしてアジア太平洋地域における急速な生産能力の増強です。強度対重量比の優位性と自動包装ラインとの互換性から、段ボール箱は主力形態であり続けています。一方、液体用カートンは飲料や乳製品分野で普及が進んでいます。欧州における2030年までのリサイクル率70%達成目標や、米国が2040年までに問題のあるプラスチックを段階的に廃止する方針といった規制上の期限が、代替素材への移行を後押ししています。スマーフィット・カッパとウェストロックの合併に代表される業界再編は、規模の拡大をもたらし、プレイヤーが変動の激しい古段ボール(OCC)やバージンパルプの原料価格を管理する助けとなります。同時に、繊維混合技術の革新により軽量化が実現され、輸送時の排出量を削減するとともに、ブランドの持続可能性目標を支援します。

世界の紙・板紙包装市場の動向と洞察

Eコマース主導のSKU爆発的増加

オンラインマーケットプレースでは数千種類の商品バリエーションが掲載され、これらは損傷なく消費者に届けられる必要があります。このため、コンバーターは短納期印刷とオーダーメイド段ボール設計へと向かっています。パッケージング・コーポレーション・オブ・アメリカ(PCA)は、小売業者が二次包装をアップグレードし、空隙充填を最小限に抑え、容積重量割増料金を削減した結果、2024年に段ボール出荷量が9.2%増加したと報告しています。追加開封不要でブランドグラフィックを提示する棚出し可能なフォーマットはCAGR5.81%で拡大しており、デジタル印刷の速度によりコンバーターは小ロット注文を経済的にバッチ処理できます。インターナショナル・ペーパー社の2024年純売上高186億米ドルは、工場がライナーボードと特殊フルートグレードの間で生産能力を転換できる場合の量的な成長余地を裏付けています。リサイクル義務化はプラスチック製メール袋よりも紙製ソリューションを優遇し、紙包装市場が小包市場の成長を引き続き取り込むことを保証しています。

プラスチック使用禁止と課税

各国政府は使い捨てプラスチックに対し、即時発効する全面禁止や課税措置を講じています。ニューサウスウェールズ州では2025年1月より、プラスチックコーティングされたコーヒーカップやカトラリーの使用制限を開始しました。欧州では、製品安全表示規則もブランドを単一素材の板紙へ誘導しており、明確なリサイクルロゴが付いています。ビレルド社の高性能ブラウンバリア袋紙は、工業用袋のポリエチレンコーティングに取って代わり、認証済みバイオベース含有量によるプレミアム価格を確保しています。米国環境保護庁が2040年までのプラスチック廃棄物ゼロ化を計画する中、ブランドオーナーは複数年の供給契約を締結し、追加のクラフトライナー生産能力を支えています。

変動する古紙(OCC)とバージンパルプ価格

パルプ及び古紙指数は2024年に7.2%上昇し、ヘッジプログラムを持たないコンバーターを圧迫しました。ストーラ・エンソ社は、90億ユーロ(97億米ドル)の売上にもかかわらず、木材繊維のインフレが逆風であると指摘しています。スポットOCCに依存する小規模工場は、四半期契約で追加料金を転嫁するのに苦戦しており、樹脂コストがより安定しているプラスチック代替品とのマージンが縮小しています。

セグメント分析

2025年、段ボール板紙は紙包装市場の42.85%を占めました。これは厳格なEC物流基準とリサイクル性要件の恩恵によるものです。国際紙業(International Paper)がマクロ需要の低迷の中でも産業包装分野で安定した利益率を維持していることから、このセグメントの営業レバレッジが顕著です。液体用カートンは数量ベースではごく一部ながら、乳製品・飲料ブランドがPEFC認証の再生可能素材カートンへ多層プラスチックパウチから切り替える動きにより、5.54%のCAGRで拡大しています。折り畳み式カートンは化粧品・医薬品分野で存在感を維持しており、高精細オフセット印刷によるグラフィックが店頭での訴求力を高めています。技術革新は油分・湿気に耐えつつ製紙工場のパルプ化工程で繊維回収を可能とする水性バリア材に焦点が当てられています。

軽量化は依然として主要なコスト抑制策です。主要段ボールメーカーは、必要なエッジクラッシュ強度を少ない繊維量で達成する高澱粉デュアルウォールフルートを採用しています。ビレルド社の14億スウェーデンクローナ(約1億3,000万米ドル)規模のグレード転換プログラムは、坪量を10%低減した食品用カートンボードの生産を目指しています。EUのリサイクル義務化により、サプライヤーは単一素材設計へ移行を迫られており、紙包装市場における段ボール・カートングレードの長期的な優位性が確保されています。

2025年の売上高に占める食品・飲料分野の割合は41.10%に達し、厳格な衛生基準と消費者のリサイクル可能なテイクアウト容器への要望を裏付けています。グラフィック・パッケージング社の最新10-K報告書では、冷凍食品用板紙トレイが市場平均を上回る成長を示したと記載されています。パーソナルケアブランドは、ラミネートを自然派イメージを伝えるエンボス加工クラフトスリーブに代替することで、セグメントのCAGRを6.30%に押し上げています。医薬品包装は、改ざん防止用ティアストリップやシリアル化規制にシームレスに対応するバーコード付きインサートが効果を発揮しています。

ブランドオーナーはまた、サプライヤー選定において再生可能エネルギーを優先し、スコープ3排出量を購買決定に連動させています。モンディ社は現在、売上の87%が再利用可能またはリサイクル可能な基準を満たしていると報告しています。この嗜好が紙包装市場の規模見通しを支えており、視認性の高い消費者向け用途においてプラスチックの余地はほとんど残されていません。

地域別分析

アジア太平洋地域は2025年時点で紙包装市場の最大シェア46.80%を占め、中国の過去最高となる1億2,965万トンの紙生産量と、2031年までの地域CAGR4.95%が牽引しています。低コストな労働力、統合されたパルプ供給網、急成長する電子商取引量が投資パイプラインを支えています。九龍紙業(Nine Dragons)単独でも、ファストフードチェーン向けに200万トンの漂白箱板紙生産能力を増強中です。日本と韓国は、回収率80%超を実現するリサイクルシステムで地域を補完し、輸出市場向けの高再生紙含有ライナーボードを可能にしています。

北米は豊富な森林資源と高度な加工ラインを組み合わせ、高グラフィック段ボールや成形パルプ緩衝材を優位としています。パッケージング・コーポレーション・オブ・アメリカは2024年に84億米ドルの売上を記録し、安定した国内需要を証明しました。欧州ではより厳格な規制路線を採っています。包装・包装廃棄物規制により2030年までに義務付けられるリサイクル率は70%に引き上げられ、軽量板紙の革新が促進されています。ストーラ・エンソ社のフィンランドにおける新板紙ラインは、循環型経済のスコアカードを満たすプレミアムコート紙グレードへの資本再配分を体現しています。

ラテンアメリカおよび中東・アフリカ地域は、都市化が進む新興市場として包装製品消費を牽引しています。クラビンの森林統合モデルはメルコスール加盟国への競争力ある納入コストを実現し、ブラジルは輸出用ライナーボードの炭素強度低減につながる二国間グリーン燃料貿易を模索中です。インフラ不足や通貨変動が当面の成長を抑制するもの、ブランドオーナーは長期的な数量拡大を見込み、紙包装市場の地理的拡大を推進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引主導のSKU急増

- プラスチック使用禁止措置および課税

- 地方都市におけるファストフード展開

- 産業用堆肥化基準の台頭

- 消費者向け医薬品フルフィルメント

- 持続可能性を重視した包装の変革

- 市場抑制要因

- 変動する古紙パルプ(OCC)およびバージンパルプの価格

- 森林破壊に起因するNGOからの圧力

- 大手オンライン小売業者による自社内段ボール加工

- カーボンボーダー調整費用

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の激しさ

- 貿易シナリオ(HSコード-4819)

- 主要国における輸出入データ(数量ベース、2021-2024年)

- 主要国における輸出入データ(金額ベース、2021-2024年)

第5章 市場規模と成長予測

- 製品タイプ別

- 折り畳み式カートン

- 段ボール包装

- 液体用カートン

- その他の製品タイプ

- エンドユーザー業界別

- 食品・飲料

- 医療・製薬

- パーソナルケアおよび化粧品

- 電気・電子機器

- 産業および自動車

- 包装形態別

- 主要小売パッケージ

- 二次輸送パック

- 棚出し用/ディスプレイ用パック

- 保護用インサートおよび緩衝材

- 材質グレード別

- バージンファイバー

- 再生繊維

- ハイブリッド/混合繊維

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- マレーシア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- DS Smith plc

- Packaging Corporation of America

- Stora Enso Oyj

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Billerud AB

- Sonoco Products Company

- Nine Dragons Paper(Holdings)Ltd.

- Svenska Cellulosa AB(SCA)

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Mayr-Melnhof Karton AG

- Pratt Industries Inc.

- Klabin S.A.

- Georgia-Pacific LLC