|

市場調査レポート

商品コード

1940748

英国のサイバー保険:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United Kingdom Cyber Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のサイバー保険:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

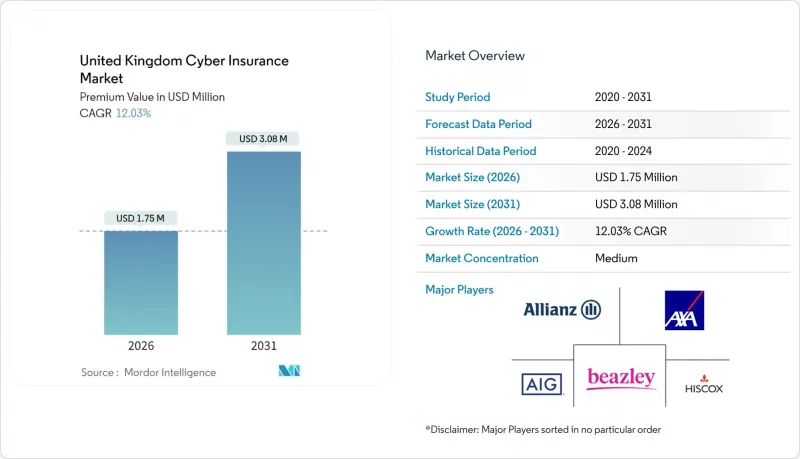

英国のサイバー保険市場は、2025年の156万米ドルから2026年には175万米ドルへ成長し、2026年から2031年にかけてCAGR12.03%で推移し、2031年までに308万米ドルに達すると予測されています。

構造的な需要は、義務化された情報漏洩通知規則、ハイブリッドワークへの持続的な移行、そしてロイズの世界的に認知されたキャパシティハブから生じています。2024年には英国企業の50%が被害に遭うと推定されるランサムウェア活動の活発化が、単独保険の採用を加速させています。小規模・零細企業におけるデジタル化の進展は、英国サイバー保険市場において急成長セグメントを開拓する一方、保険料のインフレと厳格化されたサブリミットが普及を抑制しています。再保険キャパシティの逼迫とシステミックリスクの不確実性は、成熟した市場が選択的引受と積極的なリスク管理モデルへ移行していることを示しています。

英国サイバー保険市場の動向と洞察

ランサムウェアの頻度と深刻化の加速

ランサムウェア攻撃は、重要インフラと中堅企業を標的とする資金力のあるエコシステムへと発展しました。二重・三重の身代金要求戦術により、フォレンジック調査費、法的費用、事業中断コストが増大し、平均保険金支払額は従来のモデルを上回っています。MOVEitを例とするサプライチェーン攻撃は、サードパーティ製ソフトウェアへの依存を通じて、セキュリティ対策が成熟した組織さえも危険に晒します。保険会社は現在、滞留時間を短縮しデータを迅速に復旧させるため、継続的監視サービスとインシデント対応リテーナーを保険契約に組み込んでおります。市場のキャパシティは、脅威インテリジェンスのテレメトリを活用してほぼリアルタイムで価格設定を精緻化できる保険会社を優遇する傾向にあります。

GDPRおよびICO違反通知義務に伴う罰金

72時間開示ルールにより、企業はインシデント対応手順書を正式化し、規制対応や罰則軽減をカバーする高額補償限度額の購入が求められます。ICOの執行は、特に医療・金融分野において、不十分な技術的統制に対して数百万ポンド規模の罰金を科す姿勢を示しています。保険会社は、保険約款を説明責任原則に照らし合わせ、認証済み統制に対して保険料割引を適用することで引受を差別化しています。国境を越えたデータ転送が標準契約条項に依存する中、保険会社は法的コンサルティングやエスクローサービスへの拡張条項を追加しています。規制の明確化が進むことで、コンプライアンス補償は任意の付帯特約から、購入の核心的要因へと変容しています。

保険料のインフレと補償範囲のサブリミット

年間15~25%の保険料上昇は多くの企業のリスク予算を上回り、購入者は補償限度額の引き下げまたは自己負担額の増加を受け入れることを余儀なくされています。事業中断、ブリック化、評判毀損に対するサブリミットは、請求時に初めて判明する大きな補償の空白を生じさせます。既に資金繰りが逼迫している中小企業は、市場撤退によるリスク回避的な選択を行い、保険会社の高リスクプールを拡大させるリスクがあります。再保険コストの上昇は、透明性が限られる中、小売価格に直接反映されます。このフィードバックループは、保険数理上の確実性が向上し、代替的なリスク移転手段が登場しない限り、持続可能な成長を脅かします。

セグメント分析

2025年時点で、英国サイバー保険市場シェアの70.10%を単独商品が占めており、一般的な補償上限に制約されない特化型保険への需要の高さが示されています。このセグメントはCAGR12.78%で拡大が見込まれ、英国サイバー保険市場の主要な成長エンジンとしての地位を強化しています。購入者は、規制当局が数百万ポンドの罰金を科す可能性がある状況において、商業複合保険パッケージにおけるサイレント・サイバーの補償範囲の空白が許容できない不確実性をもたらすことを認識しています。単独保険形態に重ねて適用されるアクティブ保険モデルは、監視・脅威インテリジェンス・迅速対応リテーナーを統合し、平均封じ込め時間(MTTC)の短縮と被害深刻度の低減を実現します。パッケージ型付帯保険は初めて保険加入する零細企業には依然有効ですが、補償限度額の制約やインシデント対応能力の不足から、サイバーセキュリティ成熟度の向上に伴い採用は減少傾向にあります。

単独保険会社は、契約者ネットワークからの独自テレメトリーを活用し、契約期間中の価格設定の精緻化と特約の自動化を実現します。このフィードバック豊富な環境により、リスク管理が改善され次第、契約期間中の限度額引き上げやランサムウェア免責額の削減が可能となります。平均保険料は中小企業で2,000~1万5,000ポンド、大企業で50,000~50万ポンドの範囲であり、売上高という表向きの数値ではなく、リスクの細分化された露出度を反映しています。技術分野特化型特約では、ソースコードエスクロー、暗号資産盗難、AIモデルポイズニングをカバーしており、商品多様化の進展が伺えます。パッケージ型セグメントは、広範さよりも簡便性を重視する長期保険契約のマイクロビジネスをターゲットとする組み込み型ブローカープラットフォームと連携することで、一桁台の成長を維持できる可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ランサムウェアの頻度と深刻度の加速

- GDPRおよびICO違反通知罰金の義務化

- ポストCOVIDにおけるリモートワークの攻撃対象領域拡大

- 中小企業向けデジタルブローカープラットフォーム(組み込み型サイバー保険)

- 英国政府によるサイバー・エッセンシャルズ制度の導入状況

- NHSおよびCNIにおけるゼロトラスト調達義務

- 市場抑制要因

- 保険料のインフレと補償範囲のサブリミット

- 英国市場における保険統計上の損失履歴の不足

- 戦争除外条項及びシステミックリスクの不確実性

- 再保険キャパシティの逼迫(MOVEit後)

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- パッケージ製品

- スタンドアロン

- 企業規模別

- 大企業

- 中堅企業

- 小規模・零細企業

- 業界別

- BFSI

- IT・通信

- 小売・電子商取引

- ヘルスケア・ライフサイエンス

- 製造業

- 政府・公共部門

- 教育

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- AIG

- Beazley

- Hiscox

- Allianz

- AXA XL

- Zurich

- Chubb

- Tokio Marine Kiln

- CNA Hardy

- QBE

- RSA

- Sompo International

- Corvus London Markets

- Lloyd's syndicates(collective)

- Marsh McLennan

- Aon

- WTW

- Howden

- Gallagher

- CFC Underwriting

- Coalition