サブスクリプションベースゲーム- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Subscription-Based Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690958

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

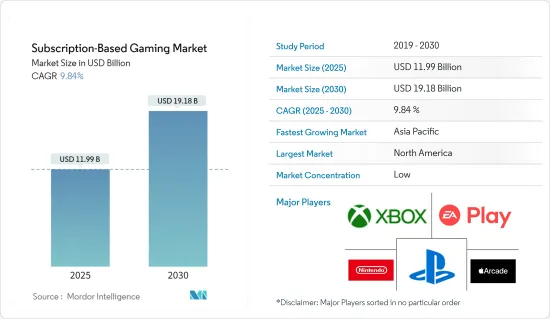

サブスクリプションベースゲーム市場規模は2025年に119億9,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは9.84%で、2030年には191億8,000万米ドルに達すると予測されます。

主要ハイライト

- ゲーム産業における継続的な技術進歩が市場の成長を後押ししています。ゲームライブラリへのアクセスに定期的な料金を課すサブスクリプションサービスが市場に大きく貢献。

- また、5Gのリリースや無制限データプランの登場も、サブスクリプションベースクラウドゲーミングの世界の成功を後押しする主要因になると予想されます。さらに、5Gインフラへのサービスや投資が増加していることも、この成功に不可欠です。Ericssonによると、アジア太平洋の5Gモバイル契約数は2025年までに約15億4,500万件に達するといいます。

- 様々なバンドルサービスの革新が市場を牽引しており、サブスクリプションモデルでは、参入企業は定期的に料金を支払うことで、指定された期間、追加のゲーム内材料や機能にアクセスできます。サブスクリプションモデルは、アプリ内課金としてモバイルゲームでもよく見られます。カジュアルユーザーは無料でゲームをプレイし続けるが、有料ユーザーはプレミアムなゲーム体験を味わうことができます。

- サブスクリプションは通常、ゲーマーにとってより手頃なエントリーポイントを記載しています。加入者は1つのゲームに多額の初期費用を支払う代わりに、月額料金でゲームのライブラリにアクセスできます。

- 市場で事業を展開するサービスプロバイダの数は急速に増加しているため、ベンダーは消費者に利益を提供するために、長期的に維持できない可能性のある損失を余儀なくされる競争空間が形成されています。サービスプロバイダが、提供するサービスの価格を上げることで収益性を高める方向に事業計画を転換すれば、消費者もまた、競合価格で同様のサービスを提供する新規参入企業に乗り換える可能性があります。このようなシナリオは、サービスプロバイダの成長に課題しています。

- ポストCOVIDはまた、人々が自宅で没入ベース体験に取り組む必要性を高めました。さらに、手頃な価格のVR機器と5Gの導入により、世界中の多くのユーザーがモバイルゲームに没頭できるようになりました。2023年7月、Verizonは、2億人以上、つまりアメリカ人の約3人に2人が、同社が提供する世界最速かつ最も信頼性の高い5Gウルトラワイドバンドサービスを享受していると述べました。Verizonの5Gウルトラ・ワイドバンドのパワーとパフォーマンス、高速ダウンロード速度、データ量の多いアクティビティをサポートする能力は、米国の顧客が体験できます。

サブスクリプションベースゲーム市場動向

モバイルゲームセグメントが大きな市場シェアを占める見込み

- モバイルゲーミングは、そのアクセスのしやすさと普及により、ゲーミング・サブスクリプション市場の重要なセグメントとして浮上しています。これらのサブスクリプションは、厳選されたプレミアムモバイルゲームへのアクセスを月額または年額で記載しています。加入者は、含まれるゲームのすべての機能とコンテンツにフルアクセスし、広告のないゲーム体験を楽しむことができます。

- クロスプラットフォームのサブスクリプションは、複数のプラットフォームにまたがるゲームエコシステムの統合が進むにつれて人気が高まっています。加入者は、モバイル機器や、シームレスなゲーム体験を提供するコンソール、PC、ストリーミング機器などの他のプラットフォームでゲームにアクセスすることができます。

- 一部のモバイルゲームでは、オンラインマルチ参入企業モード、限定トーナメント、または対戦プレイのための追加的なソーシャル機会を利用するためのサブスクリプションを必要とするマルチ参入企業エクスペリエンスを提供しています。

- モバイルゲームのサブスクリプションの中には、教育または学習指向のゲームに焦点を当てたものがあり、モバイルデバイスで楽しく教育的な活動に幼児を参加させたいと考えている親や教育者向けに提供されています。こうしたサブスクリプションには、学習効果を高めるよう設計されたさまざまな教育ゲームやインタラクティブコンテンツが含まれていることが多いです。

- スマートフォンユーザーの世界の増加は、定額制モバイルゲームサービスにとって大きな成長機会となります。GSMAによると、2030年までに北米のスマートフォン普及率は90%に上昇すると予想されており、CISやアジア太平洋などの地域はさらに著しい成長を遂げると予測されています。

アジア太平洋は市場の大幅な成長が見込まれる

- アジア太平洋では、高速ブロードバンドや5Gネットワークが都市部や農村部で広く利用できるようになるなど、インターネットインフラが大きく進歩しています。このような接続性の向上により、クラウドベースゲームを最小限の待ち時間とバッファリングでシームレスにストリーミングできるようになり、この地域におけるサブスクリプションベースゲームの需要を促進しています。

- 中国は世界最大のゲーム人口を誇っており、さまざまな年齢層や属性にわたって数百万人のゲーマーがいます。産業団体CGIGCによると、2023年7月、中国のビデオゲーム参入企業人口は6億6,800万人に増加しました。娯楽、社会活動、競技スポーツとしてのゲームの人気は、サブスクリプション・ベースゲームプラットフォームが提供する多様なゲーム体験への需要を後押ししています。

- 中国政府は、ゲームを含む技術革新とデジタルエンターテインメント産業を支援してきました。クラウドインフラ、ゲームコンテンツ、デジタルサービスの開発を促進する施策やイニシアティブは、中国におけるゲーム定額制市場の成長に貢献しています。例えば、2023年12月、国家新聞出版局(NPPA)は、WeChatを介した105の新しいオンラインゲームを承認し、この動きはオンラインゲーム産業の繁栄と健全な発展を支援する意思表示であると説明しました。

- 2023年12月、国家通商産業省によると、シンガポールは世界のゲーマーの45%が住むアジアのゲームとeスポーツのハブになる可能性があるといいます。シンガポールの人口のほぼ3分の1がゲーマーであり、シンガポールは定額制ゲームにとって有利な市場となっています。

- この地域におけるサブスクリプションベースゲームの需要の高まりは、先進的なインターネットインフラ、強力なゲーム文化、技術革新、政府の支援、戦略的パートナーシップ、消費者の嗜好の変化によって後押しされています。

サブスクリプションベースゲーム産業概要

サブスクリプションベースゲーム市場は、Xbox(Game Pass)、(Microsoft Corporation)、PlayStation Now(Sony Corporation)、Apple Arcade(Apple Inc.)、Nintendo Switch Online(Nintendo)(Nintendo)、EA Play(Electronic Arts Inc.)などの主要企業が存在し、細分化されています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2024年4月:Vodafone Ideaは、パリを拠点とするCareGameと提携し、クラウドゲームプラットフォームを発表。このサービスは「トライ&バイ」モデルで提供され、無料トライアル期間を経て、ユーザーは月額利用料を支払う必要があります。

- 2023年10月:Sonyはクラウドゲームへの取り組みを強化し、PlayStation Plus加入者に対し、『スパイダーマン:マイルス・モラレス』や待望の『バイオハザード4』リメイク版などの有名タイトルを、数週間以内にPlayStation 5で直接ストリーミング配信する機会を記載しています。さらに、PS5のクラウドゲーミングをスマートフォンなど他の様々なデバイスにも拡大することを示唆しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エコシステム分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場の促進要因

- サービスのバンドル化とデバイスに依存しない機能への最近の動き

- サブスクリプションベースモデルはユーザーに高い柔軟性を提供

- 市場課題

- サービスの可用性を確保するための地域情勢への依存度の高さ

- モバイルセグメントにおける認知度の相対的低下と普及不足

- COVID-19が市場に与える影響の評価

- サブスクリプションベースゲームモデルにおける最近の提携とパートナーシップ

第6章 市場セグメンテーション

- ゲームタイプ別

- コンソールゲーム

- PCベースゲーム

- モバイルゲーム

- 地域別

- 北米

- 欧州

- アジア

- オーストラリアとニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Xbox(Game Pass)(Microsoft Corporation)

- PlayStation Now(Sony Corporation)

- Apple Arcade(Apple Inc.)

- Nintendo Switch Online(Nintendo Co. Ltd)

- EA Play(Electronic Arts Inc.)

- Google Play Pass(Google LLC)

- Humble Bundle Inc.

- GeForce Now(NVIDIA)

- Uplay Pass(Ubisoft)

- Amazon Luna(Amazon Inc.)

- Tencent Holdings Ltd

- Epic games Inc.

- Prime Gaming(Amazon Inc.)

第8章 投資分析と市場展望

目次

The Subscription-Based Gaming Market size is estimated at USD 11.99 billion in 2025, and is expected to reach USD 19.18 billion by 2030, at a CAGR of 9.84% during the forecast period (2025-2030).

Key Highlights

- Continuous technological advancements in the gaming industry are propelling the market's growth. Subscription services, which charge a regular fee for access to a game library, significantly contribute to the market.

- The release of 5G and the emergence of unlimited data plans are also expected to be key factors aiding the success of subscription-based cloud gaming across the world, as most gamers today prefer playing games on their mobile devices. In addition, the increasing services and investments in 5G infrastructure are vital to this success. According to Ericsson, 5G mobile subscriptions in Asia-Pacific will reach around 1,545 million by 2025.

- Various bundling service innovations drive the market, and the subscription model allows players to pay regularly to access additional in-game material and features for a specified length of time. The subscription model is also commonly seen in mobile gaming as an in-app purchase. While casual users will continue to play the games for free, those who pay can experience a premium gaming experience.

- Subscriptions typically offer a more affordable entry point for gamers. Instead of paying a significant upfront cost for a single game, subscribers gain access to a library of games for a monthly fee, which can often be lower than the cost of purchasing even one new game.

- The number of service providers operating in markets is increasing rapidly, thus creating a competitive space where vendors are forced to offer benefits to consumers at a loss that may not be sustainable over a long period. Once the service provider switches the business plan to turn toward profitability by increasing the prices of the services offered, the consumers may also switch to newer players offering similar services at competitive prices. Such scenarios are challenging the growth of the service providers.

- The Post COVID also increased the need for people to engage in immersive experiences at home. In addition, affordable VR equipment and 5G implementation allowed many users worldwide to engage in mobile gaming. In July 2023, Verizon stated that over 200 million people, or around two of every three Americans, enjoyed the world's fastest and most reliable 5G Ultra Wideband service offered by the company. The power and performance of a Verizon 5G Ultra Wideband, with fast download speeds and the capability to support data-intensive activities, can be experienced by customers in the United States.

Subscription Based Gaming Market Trends

The Mobile Gaming Segment is Expected to Hold Significant Market Share

- Mobile gaming has emerged as a significant segment in the gaming subscriptions market due to its accessibility and widespread adoption. These subscriptions offer access to a curated selection of premium mobile games for a monthly or yearly fee. Subscribers can enjoy ad-free gaming experiences with full access to all features and content of the included games.

- Cross-platform subscriptions have become popular with the increasing integration of gaming ecosystems across multiple platforms. Subscribers can access games on their mobile devices and other platforms such as consoles, PCs, or streaming devices that offer seamless gaming experiences.

- Certain mobile games offer a multiplayer experience that requires a subscription for access to online multiplayer modes, exclusive tournaments, or additional social opportunities for competitive play.

- Some mobile gaming subscriptions focus on educational or learning-oriented games, catering to parents and educators looking to engage their children in fun and educational activities on mobile devices. These subscriptions often include various educational games and interactive content designed to enhance learning outcomes.

- The increasing number of smartphone users globally provides a significant growth opportunity for subscription-based mobile game services, as they offer a convenient, affordable, and diverse gaming experience to a broad audience. According to the GSMA, by 2030, North America's smartphone adoption rate is expected to increase to 90%, with regions like CIS and Asia-Pacific projected to register more significant growth.

Asia-Pacific is Expected to Witness Significant Growth in the Market

- Asia-Pacific has witnessed significant advancements in internet infrastructure, with the widespread availability of high-speed broadband and 5G networks in urban and rural areas. This improved connectivity enables seamless streaming of cloud-based games with minimal latency and buffering, thus driving the demand for subscription-based gaming in the region.

- China boasts the world's largest gaming population, with millions of gamers across various age groups and demographics. According to the industry association CGIGC, in July 2023, China's video game player population grew to 668 million. The popularity of gaming as a form of entertainment, social activity, and competitive sport fuels the demand for diverse gaming experiences offered by subscription-based gaming platforms.

- The Chinese government has supported technological innovation and digital entertainment industries, including gaming. Policies and initiatives promoting the development of cloud infrastructure, gaming content, and digital services contribute to the growth of the gaming subscriptions market in China. For instance, in December 2023, the National Press and Publication Administration (NPPA) approved 105 new online games via WeChat, describing the move as a show of support for the prosperity and healthy development of the online game industry.

- In December 2023, according to the Ministry of State for Trade and Industry, Singapore had the potential to become a hub for gaming and esports in Asia, where 45% of the world's gamers live. Almost a third of Singapore's population class themselves as gamers, making the country a lucrative market for subscription-based gaming.

- The growing demand for subscription-based gaming in the region is fueled by advanced internet infrastructure, a strong gaming culture, technological innovation, government support, strategic partnerships, and changing consumer preferences.

Subscription Based Gaming Industry Overview

The gaming subscriptions market is fragmented with the presence of major players like Xbox (Game Pass), (Microsoft Corporation), PlayStation Now (Sony Corporation), Apple Arcade (Apple Inc.), Nintendo Switch Online (Nintendo Co. Ltd), and EA Play (Electronic Arts Inc.). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- April 2024: Vodafone Idea announced a cloud gaming platform in collaboration with Paris-based CareGame, offering a selection of premium AAA games for subscribers. The service is being provided in a "try-n-buy" model with a free trial period, after which users have to pay a monthly subscription.

- October 2023: Sony bolstered its cloud gaming endeavors, offering PlayStation Plus subscribers the opportunity to stream renowned titles such as "Spider-Man: Miles Morales" and the highly-anticipated "Resident Evil 4" remake directly to their PlayStation 5 consoles in the weeks ahead. Additionally, the tech giant has hinted at the prospect of extending PS5 cloud gaming to various other devices, including smartphones, in the foreseeable future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Recent Move Toward Bundling of Services and Device Agnostic Capabilities

- 5.1.2 Subscription-based Model Provides Higher Flexibility to Users

- 5.2 Market Challenges

- 5.2.1 High Dependence on Local Landscape for Ensuring Availability of Services

- 5.2.2 Relatively Lower Awareness and Lack of Penetration in the Mobile Segment

- 5.3 Assessment of the Impact of COVID-19 on the Market

- 5.4 Recent Collaborations and Partnerships in the Subscription-based Gaming Model

6 MARKET SEGMENTATION

- 6.1 By Gaming Type

- 6.1.1 Console Gaming

- 6.1.2 PC-based Gaming

- 6.1.3 Mobile Gaming

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Xbox (Game Pass) (Microsoft Corporation)

- 7.1.2 PlayStation Now (Sony Corporation)

- 7.1.3 Apple Arcade (Apple Inc.)

- 7.1.4 Nintendo Switch Online (Nintendo Co. Ltd)

- 7.1.5 EA Play (Electronic Arts Inc.)

- 7.1.6 Google Play Pass (Google LLC)

- 7.1.7 Humble Bundle Inc.

- 7.1.8 GeForce Now (NVIDIA)

- 7.1.9 Uplay Pass (Ubisoft)

- 7.1.10 Amazon Luna (Amazon Inc.)

- 7.1.11 Tencent Holdings Ltd

- 7.1.12 Epic games Inc.

- 7.1.13 Prime Gaming (Amazon Inc.)

8 INVESTMENT ANALYSIS AND MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日