慢性静脈閉塞症治療:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Chronic Venous Occlusions Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690953

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

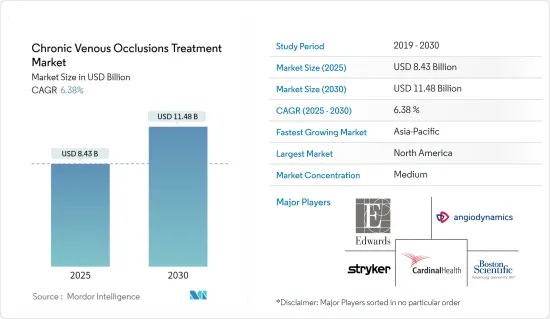

慢性静脈閉塞症治療の市場規模は2025年に84億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.38%で、2030年には114億8,000万米ドルに達すると予測されます。

慢性静脈閉塞症治療は、慢性静脈疾患の治療に用いられます。静脈閉塞とは、静脈が血栓、筋肉、動脈、他の静脈などの近くの構造物によって閉塞、狭窄、圧迫されることです。その結果、血液が溜まって逆流し、その部位に痛みや腫れが生じます。

静脈閉塞性疾患の世界の有病率の高さが市場の成長を後押ししています。例えば、2024年5月にInternational Wound Journalに掲載された研究によると、慢性静脈疾患の平均有病率は58.4%、静脈瘤の有病率は22.1%でした。このような世界レベルでの高い有病率は、市場の成長を後押ししています。

主要な市場プレーヤーは、特に血管疾患治療用の低侵襲デバイスの製品ポートフォリオを強化するために、買収などの戦略的な動きをますます強めています。

例えば、2024年5月、シーメンス・ヘルティニアーズ社は子会社のバリアン社を通じてイノバ・バスキュラー社の買収を決定しました。医療機器業界で著名なInnova Vascular社は、血管疾患治療に特化した最先端の低侵襲機器を専門としています。主力製品であるラグナ血栓除去システムは、その卓越した柔軟性、追跡可能性、多様なサイズで高く評価されています。

これらの特性により、ヘルスケアプロバイダーは、患者のプロファイルや血栓のバリエーションにかかわらず、静脈血栓塞栓症に効果的に対処することができます。この買収により、シーメンス・ヘルティニアーズは血栓治療に対する製品ラインアップを大幅に強化し、予測期間中に同市場が大きく成長する舞台を整えました。

さらに、製薬会社は静脈不全の治療に関する認識を高めるためのイニシアチブを率先して推進するようになっており、予測期間中の市場成長を後押ししています。例えば、2023年7月、LES LABORATOIRES SERVIER社は静脈疾患啓発に特化した包括的キャンペーンを展開しました。ヘルスケア専門家や患者と密接に協力することで、同社は静脈不全の理解を深め、症状管理を強化することを目指しています。製薬企業によるこのような協調的な取り組みは、今後数年間の市場成長を牽引するものと思われます。

このように、静脈疾患の有病率の高さ、静脈疾患に対する意識の高まり、新製品の発売といった上述の要因のおかげで、市場の成長はその大半を牽引しています。しかし、治療に伴うコストやリスクは市場の成長を妨げる可能性があります。

慢性静脈閉塞症治療市場の動向

深部静脈不全セグメントが予測期間中の市場成長を牽引すると予測

慢性静脈閉塞症治療薬は、主に抗生物質と抗凝固薬で構成されています。これらの薬剤は、血管内の血栓を予防または治療することを目的としています。このような血栓は、脳卒中、心臓発作、深部静脈血栓症、肺塞栓症などの深刻なリスクをもたらします。抗凝固薬は血栓の形成を予防し、血栓溶解薬は既存の血栓を溶解します。

深部静脈血栓症の管理に有効な抗凝固薬には、エノキサパリン、ダルテパリン、ティンザパリンなどの低分子量ヘパリン(LMWH)から、未分画ヘパリン(UFH)、第Xa因子阻害薬、直接トロンビン阻害薬、ワルファリンなどのビタミンK拮抗薬まで、さまざまなものがあります。

慢性静脈閉塞症に合わせた新規経口抗凝固薬の採用が増加していることが、このセグメントの成長を後押ししています。

バイオシミラーの登場は市場競争を激化させ、慢性静脈閉塞症治療薬のコストを引き下げる方向にあります。このコスト削減は患者の利便性を高め、このセグメントの成長に直接影響を与えます。2023年9月、フレゼニウス・カビ・カナダはエノキサパリンのバイオシミラーであるELONOXの公的償還承認をカナダの全州で取得しました。ELONOX。カナダ保健省は、ELONOX(エノキサパリンナトリウム)を深部静脈血栓症を含む血栓塞栓症予防薬として特に承認しました。保健当局によるこのような償還は、アクセシビリティと適応性の向上に寄与し、セグメントの成長をさらに促進します。

深部静脈血栓症を対象とした臨床研究への注目の高まりは、セグメント成長の重要なドライバーになると予想されます。Bayer社は2024年2月、革新的な抗a2抗プラスミン(抗a2ap)抗体であるBAY3018250のDVT患者を対象とした第II相臨床試験を開始しました。本試験の結果は、本抗体が重篤な疾患に対する重要な治療手段となる可能性を示すものと期待されます。バイエルはこの結果を受け、DVT患者を対象としたこの抗体の臨床試験を次の段階に進めたいと考えています。このような取り組みは患者にとって有望であり、このセグメントの成長を後押しするものです。

したがって、バイオシミラーの台頭、DVTの臨床試験の増加、Bayerの新薬臨床試験のような大手企業による戦略的な動きなどの要因が重なり、今後数年間は同セグメントの大幅な成長が見込まれます。

予測期間中は北米が市場を独占

北米が慢性静脈閉塞症治療市場を独占する見通しです。同市場は、先進的なヘルスケアインフラ、高い静脈疾患有病率、医療機器や医薬品に対する強固な規制承認によって支えられています。

同地域の市場は、静脈疾患の高い有病率に牽引されて成長を遂げています。例えば、2023年4月、米国国立衛生研究所(NIH)は、2,500万人以上の米国人が静脈瘤に苦しんでおり、そのうち600万人が重度の静脈疾患に直面していると報告しました。これは、慢性静脈疾患が重大な健康問題であることを浮き彫りにしています。このような疾患による負担の増大が慢性静脈閉塞症治療の普及を促し、市場の成長に拍車をかけています。

さらに、2023年10月にKoninklijke Philips N.V.が非悪性の腸大腿部閉塞性疾患を対象にデュオ静脈ステントシステムを評価したVIVID試験など、進行中の臨床試験が市場をさらに押し上げることになります。Duo HybridステントとDuo ExtendステントからなるDuoシステムは、腸大腿静脈セグメントの多様な解剖学的・機械的ニーズに対応します。機器の有効性と安全性を確保するためのこれらの試験は、市場の今後の成長にとって極めて重要です。

また、深部静脈血栓症治療用に設計されたPharmascience Canada社のPms-rivaroxabanのようなジェネリック医薬品の変種が2023年11月に導入されることで、市場のアクセシビリティと適応性が高まる。このような新薬の上市は、今後数年間の市場成長の原動力となると思われます。

心血管疾患や静脈疾患の有病率が上昇していることに加え、進行中の臨床試験や製品の上市が勢いを増していることから、慢性静脈閉塞症治療市場は予測期間中に大きく成長するものと思われます。

慢性静脈閉塞症治療産業の概要

慢性静脈閉塞症治療市場は半固定的であり、複数のプレーヤーが存在します。市場開拓企業は、合併、買収、提携、共同開発など多様な戦略を駆使して新薬や新デバイスを開発しています。主な参入企業には、Cardinal Health、Stryker、Cook Medical、Boston Scientific Corporation、Edward Lifesciences、AngioDynamicsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高度な治療法とデバイスの利用可能性の増加

- 静脈閉塞性疾患の有病率の増加

- 市場抑制要因

- 治療に伴うリスクや合併症と結びついたコスト意識

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 治療タイプ別

- 慢性深部静脈血栓症

- 下肢静脈瘤

- 深部静脈不全

- その他の治療タイプ

- 製品タイプ別

- デバイス

- 治療薬

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Cardinal Health

- Stryker

- Cook Medical

- Boston Scientific Corporation

- Edward Lifesciences

- AngioDynamics

- SIGVARIS GROUP

- Johnson & Johnson Inc.(Janssen Global Services LLC)

- Penumbra Inc.

- Becton, Dickinson and Company

第7章 市場機会と今後の動向

目次

The Chronic Venous Occlusions Treatment Market size is estimated at USD 8.43 billion in 2025, and is expected to reach USD 11.48 billion by 2030, at a CAGR of 6.38% during the forecast period (2025-2030).

Chronic venous occlusion treatment is used to treat chronic venous diseases. Venous occlusion is when veins are blocked, narrowed, or compressed by nearby structures such as clots, muscles, arteries, or other veins. This can result in blood pooling and flowing backward, causing pain and swelling in the area.

The high prevalence of venous occlusion diseases globally drives the market's growth. For instance, a study published in the International Wound Journal in May 2024 revealed that the mean prevalence of chronic venous diseases was 58.4%, and the prevalence of varicose veins was 22.1%. Such a high prevalence of disease at the global level propels the market's growth.

Major market players are increasingly making strategic moves, such as acquisitions, to bolster their product portfolios, particularly in minimally invasive devices for vascular disease treatment.

For instance, in May 2024, Siemens Healthineers, through its subsidiary Varian, finalized the acquisition of Innova Vascular. Innova Vascular, a prominent player in the medical device industry, specializes in cutting-edge, minimally invasive devices tailored for vascular disease treatment. The flagship product, the Laguna Thrombectomy System, is lauded for its exceptional flexibility, trackability, and diverse range of sizes.

These attributes enable healthcare providers to address venous thromboembolism across patient profiles and clot variations effectively. With this acquisition, Siemens Healthineers has significantly bolstered its offerings for blood clot treatments, setting the stage for substantial growth in this market during the forecast period.

Additionally, pharmaceutical companies are increasingly spearheading initiatives to raise awareness about treating venous insufficiency to propel market growth during the forecast period. For example, in July 2023, LES LABORATOIRES SERVIER rolled out a comprehensive campaign dedicated to venous disease awareness. By closely collaborating with healthcare professionals and patients, the company aims to deepen the understanding of venous insufficiency and enhance symptom management. These concerted efforts from pharmaceutical entities are poised to drive market growth in the coming years.

Thus, owing to the abovementioned factors, such as the high prevalence of venous diseases, increasing awareness of venous diseases, and the launch of new products, the growth of the market is the majority driving it. However, the cost compilations and risk associated with treatment may hinder the growth of the market.

Chronic Venous Occlusions Treatment Market Trends

The Deep Vein Insufficiency Segment is Expected to Drive the Market Growth During the Forecast Period

Chronic venous occlusion treatment therapeutics primarily consist of antibiotics and anticoagulants. These medications aim to either prevent or treat blood clots within blood vessels. Such clots pose severe risks, including stroke, heart attack, deep vein thrombosis, and pulmonary embolism. Anticoagulants prevent clot formation, while thrombolytics dissolve existing clots.

Effective anticoagulants for managing deep venous thrombosis encompass a range, from low molecular weight heparins (LMWHs) like enoxaparin, dalteparin, and tinzaparin to unfractionated heparin (UFH), factor Xa inhibitors, direct thrombin inhibitors, and vitamin K antagonists such as warfarin.

The segment's growth is propelled by the rising adoption of new oral anticoagulants tailored for chronic venous occlusion.

The advent of biosimilars is poised to intensify market competition, driving down the costs of chronic venous occlusion drugs. This cost reduction enhances patient accessibility, directly influencing the segment's growth. In September 2023, Fresenius Kabi Canada achieved public reimbursement approval for ELONOX, its enoxaparin biosimilar, across all Canadian provinces. ELONOX. Health Canada specifically endorsed ELONOX (enoxaparin sodium) for thromboembolic disorder prophylaxis, including deep vein thrombosis. Such reimbursement by health authorities contributes to increased accessibility and adaptability and further propels segmental growth.

The increasing focus on clinical studies targeting deep vein thrombosis is anticipated to be a significant driver for segmental growth. A case in point is Bayer AG, which, in February 2024, initiated a Phase II clinical trial for BAY3018250, an innovative anti-a2 antiplasmin (anti-a2ap) antibody, in DVT patients. The trial's results are expected to highlight the antibody's potential as a crucial treatment avenue for severe medical conditions. Buoyed by these findings, Bayer is keen to advance the antibody to the next phase of clinical trials, with a specific focus on DVT patients. Such initiatives hold promise for patients and bolster the segment's growth.

Therefore, the confluence of factors, including the rise of biosimilars, an uptick in clinical studies for DVT, and strategic moves by major players, like Bayer's new drug trials, is poised to drive significant growth in the segment in the coming years.

North America Dominates the Market During the Forecast Period

North America is poised to dominate the chronic venous occlusion treatment market. It is buoyed by its advanced healthcare infrastructure, high venous disease prevalence, and robust regulatory approvals for medical devices and drugs.

The region's market is witnessing growth, driven by the high prevalence of venous diseases. For instance, in April 2023, the National Institutes of Health (NIH) reported that over 25 million Americans suffer from varicose veins, with a staggering 6 million facing severe venous disease. This highlights the gravity of chronic venous conditions as a significant health concern. The rising burden of these conditions has driven the adoption of chronic venous occlusion treatments, fueling market growth.

Moreover, ongoing clinical trials, such as the VIVID trial in October 2023, which assessed the Duo venous stent system by Koninklijke Philips N.V. for nonmalignant iliofemoral occlusive disease, are set to propel the market further. The Duo system, comprising the Duo Hybrid and Duo Extend stents, caters to the diverse anatomical and mechanical needs of the iliofemoral venous segment. These trials to ensure device efficacy and safety are pivotal for the market's future growth.

Also, the introduction of generic drug variants, like Pharmascience Canada's Pms-rivaroxaban in November 2023, designed for deep vein thrombosis treatment, enhances market accessibility and adaptability. Such launches will drive the market's growth in the coming years.

Given the rising prevalence of cardiovascular and venous diseases, alongside the momentum from ongoing clinical trials and the launch of products, the chronic venous occlusion treatment market is set for substantial growth during the forecast period.

Chronic Venous Occlusions Treatment Industry Overview

The chronic venous occlusion treatment market is semi-consolidated, with several players. Companies in the market use diverse strategies such as mergers, acquisitions, partnerships, and collaborations to develop new drugs and devices. Some of the major players in the market include Cardinal Health, Stryker, Cook Medical, Boston Scientific Corporation, Edward Lifesciences, and AngioDynamics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Availability of Advanced Treatments and Devices

- 4.2.2 Increasing Prevalence of Venous Occlusion Diseases

- 4.3 Market Restraints

- 4.3.1 Cost Consciousness Coupled with Risk and Complications Associated with Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Treatment Type

- 5.1.1 Chronic Deep Vein Thrombosis

- 5.1.2 Varicose Veins

- 5.1.3 Deep Vein Insufficiency

- 5.1.4 Other Treatment Types

- 5.2 By Product Type

- 5.2.1 Devices

- 5.2.2 Therapeutics

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cardinal Health

- 6.1.2 Stryker

- 6.1.3 Cook Medical

- 6.1.4 Boston Scientific Corporation

- 6.1.5 Edward Lifesciences

- 6.1.6 AngioDynamics

- 6.1.7 SIGVARIS GROUP

- 6.1.8 Johnson & Johnson Inc. (Janssen Global Services LLC)

- 6.1.9 Penumbra Inc.

- 6.1.10 Becton, Dickinson and Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日