|

市場調査レポート

商品コード

1690934

北米のフードサービス用パッケージング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Foodservice Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のフードサービス用パッケージング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

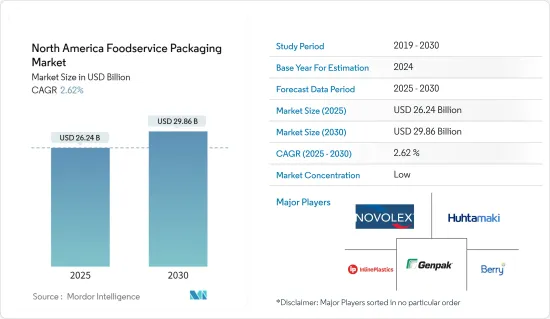

北米のフードサービス用パッケージング市場規模は2025年に262億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.62%で、2030年には298億6,000万米ドルに達すると予測されます。

主なハイライト

- 市場の成長拡大は、消費者のパッケージ食品への依存度の高さと、食品加工事業の地域的プレゼンスの高さによってもたらされました。業務のデジタル化に成功するフードサービス業者の数が増加していることから、オンライン食品注文の需要増に支えられて業界が活性化し、北米に市場成長の機会が生まれると予想されます。

- 北米のフードサービス用パッケージング事業は、基材選択の変化、新市場の拡大、所有者の動態、段ボール箱、カートン、プラスチック包装市場にサービスを提供する数々の開発により、過去10年間一貫した成長を遂げてきました。特に米国では、持続可能性と環境問題が引き続き優先されます。

- 段ボール箱は、様々な食品を出荷するために使用される製品タイプです。主に木材のセルロース繊維でできた板紙で作られていることが多いです。これらの箱は、強く、硬く、柔軟で、長持ちし、軽く、魅力的です。リサイクル可能で、製造時に有害化学物質を使用しないため、環境にも優しいです。段ボール箱は、北米の外食産業で商品の包装に使用されています。ペットボトル包装は、ポリエチレンの主な用途です。ポリエチレンは半結晶性の軽量熱可塑性樹脂で、遮音性、耐薬品性、低吸湿性に優れています。

- 業界にとって最も大きな懸念材料は、この地域の厳しい環境規制です。予測期間中、国や州レベルでのプラスチック製品の使用禁止は、業界に大きな困難をもたらすと予測されます。さらに、マクロ経済的要因による原材料価格の上昇とポリマー樹脂のサプライチェーンの不確実性が、予測期間中の市場の成長に課題する可能性があります。

- 外食産業の利益率はCOVID-19パンデミックの影響を大きく受けています。この業界の企業は、サプライチェーンの混乱と相まって消費の著しい落ち込みを目の当たりにしています。COVID-19パンデミックによる閉鎖は、米国の外食産業に一時的な包装数量の落ち込みという大きな影響を与えたが、業界は経済的課題をものともせず徐々に回復しました。限定レストランやフルサービスのレストランは、パンデミック後に消費者向けの包装を強化すると予想されます。経済が再開し、消費者が新しい食習慣を受け入れるにつれて、外食産業向け包装はこうした進化するニーズに対応できるよう適応しなければならず、市場の成長を促進します。

北米のフードサービス用パッケージング市場の動向

最も高い成長率を示すのは段ボール箱とカートンセグメント

- 段ボール箱は一度しか使用されず、その後リサイクルされるため、二次汚染のリスクを最小限に抑えることができます。さらに、製造に使用される高熱により、バクテリアやその他の汚染物質がないことが保証されます。輸送、保管、配送中の食品に清潔で安全な環境を提供するため、北米のフードサービス用パッケージング市場での採用が加速しています。

- 段ボール箱は安全性を誇り、食品に直接触れることが認められています。さらに、これらの箱は食品安全材料でコーティングすることができ、食品包装用としての魅力を高めています。食品安全コーティングの標準的なオプションの1つは、直接食品に触れるための規制基準に準拠した水性または植物性のコーティングです。このコーティングは保護層として使用でき、箱から食品への潜在的な物質の移行を防ぐことができます。無毒性で耐湿性に優れ、包装が無傷のまま食品に安全であることを保証するよう設計されており、調査された市場での成長を支えています。

- 持続可能性は、食品包装を含むすべての産業で重要な役割を果たしています。段ボール箱は再生可能な資源から作られているため、この点で高い評価を得ています。段ボール箱の大半はリサイクル材料から製造され、再利用が容易なため循環型経済を支えており、環境フットプリントを削減することで、予測期間中の北米市場での成長を支えています。

- 米国のパルプ・製紙会社であるInternational Paper Companyの報告によると、米国における段ボール包装の出荷量は、同国における包装製品の出荷量の増加に伴い増加しており、調査対象市場における同セグメントの将来的な成長の可能性を示しています。

- さらに、頑丈な構造、多用途性、安全な特性により、段ボール箱と段ボールケースは食品包装に好まれる選択肢としての地位を確保しています。それらは中の食品を保護・保存し、消費者への安全な輸送を保証します。その持続可能な性質と相まって、段ボール箱は食品業界に利益をもたらし、調査された市場におけるこのセグメントの成長を支える、適切なwin-winソリューションです。

クイックサービスレストランが最も高い市場シェアを占める

- QSRにおける持続可能なフードサービス包装の使用は極めて重要になっています。自宅で食事を準備する時間がないため、夕食の選択肢としてファーストフードを選ぶ人が増えています。外食産業は、持続可能な包装スタイルを用いて食事を安全かつ手頃な価格で包装し、顧客に手早く簡単に食事を運ぶ方法を提供することができます。

- QSRで使用される外食用品のほとんどは、発泡ポリスチレン(EPS)、ポリエチレンテレフタレート(PET)、ポリプロピレン(PP)、ポリ乳酸などのプラスチック製か、紙、板紙、成型パルプなどの紙製です。QSRは、従来のレストランやカフェよりも高品質な飲食品を迅速に提供します。これらのサービスを提供する際に公正な流通と高いレベルの一貫性を実現するため、いくつかのQSRは管理された量を供給するディスペンサーを導入し、市場の成長を支えています。

- QSRの中には、レストランの利便性と、顧客がセルフサービスの要素を通じて自分らしさを表現する自由を、容量管理されたディスペンサーによって組み合わせているところもあり、QSRが卓越した顧客サービスを提供し、製品の無駄を省き、コストを削減するのに役立っています。この地域のQSRでは、こうした少量の小袋やパケット用のパッケージング・ソリューションに対する需要が高まっており、予測期間中に市場の成長機会が生まれると予想されます。

- 米国を拠点とするファーストフードやQSRチェーンは、包装食品の需要増に対応するためカナダでポートフォリオを拡大しており、これが市場の成長を支えることになろう。例えば、2024年6月には、ハンバーガーとフライドポテトで知られる米国のファーストフードチェーンShake Shackがトロントにカナダ1号店をオープンし、予測期間中、フードサービス業界におけるパッケージングソリューションの需要を促進すると思われます。

- さらに、2023年8月には、コンテクスチュアル・モバイル広告会社のInmobiが、米国で最も好まれるファーストフードとしてピザとハンバーガーを注文する人が増えていると報告しました。このような要因は、同国におけるフードサービス用パッケージング市場の需要を創出し、予測期間中の同地域市場の成長を支える可能性があります。

北米のフードサービス用パッケージング産業の概要

北米の外食産業向け包装市場は予測期間中、Inline Plastics、Berry Global Inc.、Novolex Holdings LLC、Genpak LLC、Huhtamaki America Inc.など多くの企業が存在し、非常に細分化されます。同地域では地元ベンダー間の競合が激化しています。フードサービス用パッケージングのサプライヤーは幅広いため、バイヤーは複数のベンダーから選ぶことができます。

- 2024年5月- フードサービス製造会社のGenpak社は、アラバマ州モンゴメリー工場の改修に2,280万米ドルを投資しました。このアップグレードにより、同工場は地元の従業員を倍増させることができ、安全性の強化や、コンビニエンスストアからレストランまで幅広い顧客向けの同メーカーの食品包装ソリューションの効率向上に焦点を当てたアップグレードが含まれます。

- 2024年4月- 北米企業のNovolex Holdings LLCは、ロードアイランド州を拠点とする再利用可能なシステムと容器のブランドOZZIへの戦略的投資を発表。この投資の一環として、ノボレックスの事業部門であり、外食産業向け循環型ソリューションのリーダーであるエコプロダクツが、OZZIの成長を加速させる。OZZIの製品・ソリューションファミリーには、O2GO容器、カップ、フードサービス用パッケージング用カトラリーなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 米国におけるコンビニエンス食品需要の高止まり

- 持続可能性重視の高まりにより、ベンダーは再生プラスチックに注目

- 市場の課題

- 環境圧力による包装に関する政府規制の増加とポリマー価格の不透明さ

- 市場機会

- 業界エコシステム分析-材料サプライヤー、コンバーター、流通業者、最終用途団体、顧客、リサイクル

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- ミクロ経済要因が市場に与える影響の評価

第5章 市場セグメンテーション

- 包装形態別

- 段ボール箱とカートン

- プラスチックボトル

- トレー、皿、食品容器、ボウル

- カップと蓋

- クラムシェル

- その他の包装形態(カトラリー、スターラー/ストローなど)

- エンドユーザー別

- クイックサービスレストラン

- フルサービスレストラン

- コーヒー・スナック

- 小売店

- 公共公益・ホスピタリティ

- その他のエンドユーザー

- 国別

- 米国

- カナダ

第6章 競合情勢

- 企業プロファイル

- Pactiv Evergreen Inc.

- Dart Container Corporation

- Amhil North America

- Genpak LLC

- Huhtamaki America Inc.

- Berry Global Inc.

- Inline Plastics

- Novolex Holdings LLC

- Sabert Corporation

- Silgan Plastic Food Container

- Bennett Plastics Inc.

- B&R Plastics Inc.(Gilster-Mary Lee Corp.)

- Graphic Packaging

- Amcor PLC

- Sonoco Products Company

第7章 フードサービス用パッケージング業界の流通・サプライヤー一覧

The North America Foodservice Packaging Market size is estimated at USD 26.24 billion in 2025, and is expected to reach USD 29.86 billion by 2030, at a CAGR of 2.62% during the forecast period (2025-2030).

Key Highlights

- The market's growth expansion has been brought on by consumers' heavy reliance on packaged foods and the significant regional presence of food processing businesses. The rising number of foodservice suppliers successfully digitalizing their operations is expected to fuel the industry, supported by the increasing demand for online food ordering, creating an opportunity for market growth in North America.

- The North American foodservice packaging business has experienced consistent growth over the last decade due to changes in substrate choice, new market expansion, ownership dynamics, and numerous developments serving the market for corrugated boxes, cartons, and plastic packaging. Sustainability and environmental issues will continue to be prioritized, especially in the United States.

- Corrugated boxes are types of packaging used to ship different food products. They are often constructed of paperboard, primarily made of cellulose fibers from wood. These boxes are strong, stiff, flexible, long-lasting, light, and attractive. Due to their recyclable nature and lack of use of hazardous chemicals during production, the boxes are advantageous for the environment. Corrugated boxes are used in the North American foodservice industry to package goods. Plastic bottle packing is the principal application for polyethylene. It is a semi-crystalline, lightweight thermoplastic resin with excellent sound insulation, chemical resistance, and low moisture absorption.

- The industry's most significant source of worry is the region's strict environmental restrictions. Over the projection period, bans on plastic items at the national and state levels are projected to present significant difficulties to the industry. Additionally, the growth of raw material prices and the supply chain uncertainty in polymer resins due to macroeconomic factors may challenge the market's growth during the forecast period.

- The foodservice industry's profit margins have been significantly affected by the COVID-19 pandemic. Businesses in this industry are witnessing a notable drop in consumption, coupled with disruptions in their supply chains. The COVID-19 pandemic-induced lockdowns substantially impacted the US foodservice industry with a temporary dip in packaging volumes, and the industry gradually recovered, defying economic challenges. Limited and full-service restaurants are expected to ramp up their consumer-facing packaging post-pandemic. As the economies reopen and diners embrace new eating habits, foodservice packaging must adapt to cater to these evolving needs, driving market growth.

North America Foodservice Packaging Market Trends

Corrugated Boxes and Cartons Segment to Exhibit the Highest Growth Rate

- Corrugated boxes are used only once and then recycled, minimizing the risk of cross-contamination. Additionally, the high heat used in manufacturing ensures they are free from bacteria and other contaminants. They provide a clean, safe environment for food items during transit, storage, and delivery, which is boosting their adoption in the foodservice packaging market in North America.

- Corrugated boxes boast a safety feature and are approved for direct food contact. Moreover, these boxes can be coated with food-safe materials, bolstering their appeal for food packaging. One standard option for a food-safe coating is a water-based or vegetable-based coating that complies with regulatory standards for direct food contact. This coating can be used as a protective layer, preventing any potential migration of substances from the box to the food. It is designed to be non-toxic and moisture-resistant, ensuring the packaging remains intact and safe for food items, supporting its growth in the market studied.

- Sustainability plays a crucial role in all industries, including food packaging. Corrugated boxes score highly in this regard as they are made from renewable resources. Most are manufactured from recycled materials and support circular economies as they can be easily recycled again, which reduces their environmental footprint, thereby supporting their growth in the North American market during the forecast period.

- The International Paper Company, a US-based pulp and paper company, reported the shipments of corrugated packaging in the United States to be growing in line with the increasing growth of shipments of packing products in the country, showing the future growth potential of the segment in the market studied.

- Additionally, with their sturdy construction, versatility, and safe properties, corrugated boxes and cartons have secured their place as a preferred choice in food packaging. They protect and preserve the food products inside and ensure their safe transportation to consumers. Coupled with their sustainable nature, corrugated boxes are a proper win-win solution, benefiting the food industry and supporting the segment's growth in the market studied.

Quick-service Restaurants Hold the Highest Market Share

- The use of sustainable foodservice packaging in QSRs has become crucial. More people are turning to fast food as a supper option because they have less time to prepare meals at home. Foodservice businesses may package meals safely and affordably using sustainable packaging styles, giving clients a quick and easy way to transport meals.

- Most of the foodservice items used in QSRs are either made of plastic, such as expanded polystyrene (EPS), polyethylene terephthalate (PET), polypropylene (PP), and polylactic acid, or paper, including paper, paperboard, and molded pulp. QSRs deliver high-quality food and beverages more quickly than traditional restaurants or cafes. To achieve fair distribution and a high level of consistency in offering these services, several QSRs have implemented dispensers that supply a controlled volume, supporting market growth.

- Some QSRs combine restaurant conveniences with the freedom for customers to express their uniqueness through self-service elements through controlled-volume dispensers, which can help QSRs deliver exceptional customer service, reduce product waste, and save money. The demand for packaging solutions for these small-volume sachets or packets across QSRs in the region is expected to create a growth opportunity for the market over the forecast period.

- Fast food and QSR chains based in the United States are expanding their portfolios in Canada to address the increasing demand for packaged foods, which would support market growth. For instance, in June 2024, the US fast-food chain Shake Shack, known for its burgers and fries, opened its first Canadian location in Toronto, which would fuel the demand for packaging solutions in the foodservice industry during the forecast period.

- Additionally, in August 2023, Inmobi, a contextual mobile advertising company, reported that people were ordering pizza and burgers as the most preferred fast food items in the United States. Such factors could create demand for the foodservice packaging market in the country and support the regional market's growth during the forecast period.

North America Foodservice Packaging Industry Overview

The North American foodservice packaging market will be highly fragmented over the forecast period, with the presence of many players, such as Inline Plastics, Berry Global Inc., Novolex Holdings LLC, Genpak LLC, and Huhtamaki America Inc. There will be increasing competition among local vendors in the region. Owing to the wide range of foodservice packaging suppliers, buyers can choose from multiple vendors.

- May 2024 - Foodservice manufacturing company Genpak invested USD 22.8 million in renovating its Montgomery, Alabama, plant. The upgrades allowed the facility to double its local workforce and included safety enhancements and upgrades focused on better efficiency for the manufacturer's food packaging solutions for clients ranging from convenience stores to restaurants.

- April 2024 - Novolex Holdings LLC, a North American company, announced a strategic investment in Rhode Island-based reusable systems and container brand OZZI. As a part of this investment, Eco-Products, a Novolex business unit and leader in circular solutions for the foodservice industry, will help accelerate OZZI's growth. The OZZI family of products and solutions includes O2GO containers, cups, and cutlery for foodservice packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Convenience Food Remains High in the United States

- 4.2.2 Increasing Emphasis on Sustainability is Causing Vendors to Focus on Recycled Plastic

- 4.3 Market Challenges

- 4.3.1 Increasing Governmental Regulations on Packaging Due to Environmental Pressure and Uncertainty in Polymer Prices

- 4.4 Market Opportunities

- 4.5 Industry Ecosystem Analysis - Material Suppliers, Convertors, Distributors, End-use Organizations, Customers, and Recycling

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET SEGMENTATION

- 5.1 By Packaging Format

- 5.1.1 Corrugated Boxes and Cartons

- 5.1.2 Plastic Bottles

- 5.1.3 Trays, Plates, Food Containers, and Bowls

- 5.1.4 Cups and Lids

- 5.1.5 Clamshells

- 5.1.6 Other Packaging Formats (Cutlery, Stirrers/Straws, etc.)

- 5.2 By End User

- 5.2.1 Quick-service Restaurants

- 5.2.2 Full-service Restaurants

- 5.2.3 Coffee and Snack Outlets

- 5.2.4 Retail Establishments

- 5.2.5 Institutions and Hospitality

- 5.2.6 Other End Users

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Pactiv Evergreen Inc.

- 6.1.2 Dart Container Corporation

- 6.1.3 Amhil North America

- 6.1.4 Genpak LLC

- 6.1.5 Huhtamaki America Inc.

- 6.1.6 Berry Global Inc.

- 6.1.7 Inline Plastics

- 6.1.8 Novolex Holdings LLC

- 6.1.9 Sabert Corporation

- 6.1.10 Silgan Plastic Food Container

- 6.1.11 Bennett Plastics Inc.

- 6.1.12 B&R Plastics Inc. (Gilster-Mary Lee Corp.)

- 6.1.13 Graphic Packaging

- 6.1.14 Amcor PLC

- 6.1.15 Sonoco Products Company