アジア太平洋産業用バルブ:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Industrial Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690933

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

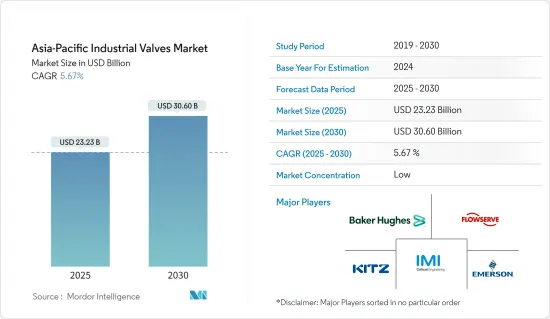

アジア太平洋の産業用バルブ市場規模は2025年に232億3,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは5.67%で、2030年には306億米ドルに達すると予測されます。

主要ハイライト

- COVID-19パンデミックは産業用バルブ市場にとって大きな課題でした。世界中のメーカーのサプライチェーンに直接影響を与え、ウイルス拡散のリスクを最小限に抑えるために生産設備を停止しました。

- 市場を牽引する要因は、水処理プラントや石油・ガス産業からのバルブ需要の増加です。

- さらに、下流市場でより幅広い用途にバルブを使用できるようにする必要性が、アジア太平洋のバルブ市場の成長に寄与しています。

- アジア太平洋産業用バルブ市場では中国が最大のシェアを占めています。

アジア太平洋産業用バルブ市場動向

石油・ガス産業での需要拡大

- 上流の石油・ガス産業は、何百万もの坑口の「クリスマスツリー」に装着するバルブの最大のユーザーであり、通常1本あたり3~5個のバルブ(サイズ 2~8')を含みます。

- 各国にわたるパイプラインの増加に伴い、炭化水素を貯蔵するための貯蔵基地の必要性も高まります。そのため、アジア太平洋諸国は需要を満たすために貯蔵ターミナルへの投資を計画しています。

- アジア太平洋は石油・ガス下流市場を独占しており、需要の大半は中国、東南アジア諸国、インドからもたらされています。エネルギー需要は20年間で50~60%成長すると予想されています。

- 中国は2030年までに、約85億米ドルを投資して23のガス貯蔵施設を建設する予定です。貯蔵施設の完成と今後予定されているガス・パイプラインは、中流部門を活性化させると予想されます。その結果、石油製品の需要は10年代半ばまでに650MTを超えると予想され、中でも輸送部門の需要が370MT近くと最も高いです。

- この地域では、いくつかの石油化学プロジェクトの建設が計画されています。例えば、中国では2021~2025年にかけて512の石油化学プロジェクトが操業を開始すると予想されています。国際エネルギー機関(IEA)が発表した石油化学報告書によると、欧州を除くほぼすべての地域で、2050年までに一次化学品の生産が増加する可能性があります。しかし、最も生産能力が伸びるのはアジア太平洋です。

- また、中国はエネルギー供給を確保するため、シェールオイル田のような国内プロジェクトを強化することで、増大するガス輸入依存を削減することを目標としています。政府は、特にシェールガスのような非在来型ガス源からの国内生産を促進するための新たな取り組みに資金を提供すると予想されます。また、中国のシェールガス生産量は2035年までに約2,800億立方メートルに達すると推定されています。従って、シェールガス生産を促進するための中国政府の努力と計画は、今後数年間に産業用バルブにとって好機を生み出すと予想されます。

- このような要因は、産業用バルブの需要を増大させると予想されます。

インドが最速の成長を記録する見込み

- インドは、製造業と機械のセグメントで最も急成長している国の一つであり、産業用バルブのニーズを生み出しています。インド政府は、製造部門を設立する企業に対して便宜を図っています。また、製造部門を後押しするために様々な施策を打ち出しています。例えば、India Brand Equity Foundation(IBEF)によると、2023年、インドの製造業輸出は過去最高を記録し、4,474億6,000万米ドルに達し、4,220億米ドルだった前年から6.03%の伸びを示しました。

- インドは世界第3位の電力生産・消費国であり、2024年1月31日現在の設備容量は429.96GWです。

- インドは鉱業が盛んです。22年度には合計1,319の鉱山が報告されており、そのうち545が金属鉱物、775が非金属鉱物に特化しています。さらに、India Brand Equity Foundation(IBEF)が発表したデータによると、2022~2023年度のインドの鉄鉱石輸出額は17億5,000万米ドルで、2021~2022年度は31億8,000万米ドルでした。

- インドの製薬産業は世界的に重要な地位を占めており、生産量は第3位、生産額は第14位です。India Brand Equity Foundation(IBEF)の予測によると、同産業の市場規模は2024年に650億米ドルに達し、2030年には2倍の1,300億米ドル、2047年には驚異的な4,500億米ドルに急増します。

- 石油・ガス産業はインドの8つの基幹産業のひとつであり、経済の他の重要な部門すべての意思決定に大きな影響を与える役割を担っています。インドの石油需要は世界で急増し、2030年には日量1,000万バレルに達すると予測されています。

- 国際エネルギー機関(IEA)によると、インドの天然ガス消費量は250億立方メートル(bcm)増加し、2024年まで年平均9%の成長が見込まれています。

- これらの要因によって、予測期間中にインドの産業用バルブの需要が増加する可能性が高いです。

アジア太平洋産業用バルブ産業概要

アジア太平洋の産業用バルブ市場はセグメント化されており、どの企業も大きなシェアを獲得していないです。同市場の主要参入企業には、Emerson Electric Co.、KITZ Corporation、Flowserve Corporation、Baker Hughes、IMI Critical Engineeringなどがいる(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 水処理プラントにおけるバルブ需要の増加

- 石油・ガス産業におけるバルブ需要の増加

- その他の促進要因

- 抑制要因

- 高い設備投資が市場成長の妨げに

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ別

- バタフライバルブ

- ボールバルブ

- グローブバルブ

- ゲートバルブ

- プラグバルブ

- その他

- 製品別

- 1/4回転弁

- マルチターンバルブ

- その他製品(コントロールバルブ)

- 用途別

- 電力

- 上下水道管理(海水淡水化を含む)

- 金属・鉱物・鉱業

- その他

- 化学製品別

- 石油・ガス

- 上流

- 中流

- 下流

- 食品加工

- パルプ・製紙

- その他

- 地域別

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Alfa Laval

- AVK Holding AS

- Baker Hughes

- CIRCOR International Inc.

- Crane Co.

- Curtiss-Wright Corporation

- Danfoss AS

- EBRO ARMATUREN Gebr. Brer GmbH

- Emerson Electric Co.

- Flowserve Corporation

- Georg Fischer Ltd

- Hitachi Metals Ltd

- Honeywell International Inc.

- IMI Critical Engineering

- ITT Inc.

- KITZ Corporation

- NIBCO

- Okano Valve Mfg. Co. Ltd

- PARKER HANNIFIN CORP.

- SAMSON AKTIENGESELLSCHAFT

- Schlumberger Limited

- The Weir Group PLC

- Valvitalia SpA

- Velan Inc.

第7章 市場機会と今後の動向

目次

The Asia-Pacific Industrial Valves Market size is estimated at USD 23.23 billion in 2025, and is expected to reach USD 30.60 billion by 2030, at a CAGR of 5.67% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic was a major challenge for the industrial valves market. It directly affected the manufacturer's supply chain across the globe and shut down the production facilities to minimize the risk of spreading the virus.

- The factors driving the market are increasing demand for valves from water treatment plants and the oil and gas industry.

- Further, the need to enable valves for a wider range of applications in the downstream market is contributing to the growth of the Asia-Pacific valves market.

- China accounts for the largest share of the Asia-Pacific industrial valves market.

Asia-Pacific Industrial Valves Market Trends

Growing Demand in the Oil and Gas Industry

- The upstream oil and gas industry is the largest user of valves to outfit millions of wellhead 'Christmas trees' that usually include 3 to 5 valves per tree in sizes of 2' to 8', as well as to segment and control flow through millions of miles of gathering pipelines (2' to 20' valves) and cross-country trunk pipelines (up to 60' or larger) required to bring the crude oil and gas to refineries, and the refined product (gasoline, diesel, natural gas) to end-user markets.

- With the increase in pipelines across the countries, the need for storage terminals to store hydrocarbons also increases. Therefore, Asia-Pacific countries plan to invest in storage terminals to meet the demand.

- Asia-Pacific has dominated the oil and gas downstream market, with most of the demand coming from China, Southeast Asian countries, and India. The energy demand is anticipated to grow by 50-60% in two decades.

- China is expected to build 23 gas storage facilities by 2030, with an investment of around USD 8.5 billion. Completing the storage facilities and the upcoming gas pipelines in the country are expected to boost the midstream sector. As a result, the demand for petroleum products is expected to cross 650 MT by the mid-decade, with the transportation segment having the highest demand of nearly 370 MT.

- Several petrochemical projects are planned to be constructed in the region. For instance, China is expected to have 512 petrochemical projects commence operations in 2021-2025. According to a petrochemicals report published by the International Energy Agency (IEA), nearly all regions except Europe may increase the production of primary chemicals by 2050. However, the most significant capacity growth is seen in Asia-Pacific.

- Also, China targets to slash its growing dependence on gas imports by boosting domestic projects like shale fields to secure its energy supply. The government is expected to fund new efforts to boost domestic production, particularly from unconventional sources like shale gas. It is also estimated that China's shale gas production will reach around 280 billion cubic meters by 2035. Thus, the Chinese government's effort and plan to boost its shale gas production are expected to create an opportunity for industrial valves in the coming years

- Such factors are expected to augment the demand for industrial valves.

India is Expected to Register the Fastest Growth

- India is one of the fastest-growing countries in terms of manufacturing sectors and machinery, giving rise to the need for industrial valves. The government provides benefits to companies setting up manufacturing units. It also outlines various policies to boost the manufacturing sector. For instance, as per the India Brand Equity Foundation (IBEF), in 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year, when exports stood at USD 422 billion.

- India is the third-largest producer and consumer of electricity worldwide, with an installed power capacity of 429.96 GW as of January 31, 2024.

- India boasts a thriving mining industry. In FY22, the country had a total of 1,319 reporting mines, with 545 dedicated to metallic minerals and 775 to non-metallic minerals. Moreover, according to the data published by the Indian Brand Equity Foundation (IBEF), during 2022-2023, India's iron ore exports amounted to USD 1.75 billion compared to USD 3.18 billion during 2021-2022.

- India's pharmaceutical industry holds a significant position on the global stage, ranking third in production volume and 14th in production value. Projections from the India Brand Equity Foundation (IBEF) suggest that the industry's market size is set to hit USD 65 billion in 2024, double to USD 130 billion by 2030, and soar to a staggering USD 450 billion by 2047.

- The oil and gas industry is among the eight core industries in India, playing a major role in influencing decision-making for all the other important sections of the economy. India's oil demand is projected to rise rapidly in the world, reaching 10 million barrels per day by 2030.

- According to the International Energy Agency (IEA), natural gas consumption in India is expected to grow by 25 billion cubic meters (bcm), registering an average annual growth of 9% until 2024.

- These factors will likely increase the demand for industrial valves in India during the forecast period.

Asia-Pacific Industrial Valves Industry Overview

The Asia-Pacific industrial valves market is fragmented, with no player capturing a significant share of the market. Some of the major players in the market include (not in any particular order) Emerson Electric Co., KITZ Corporation, Flowserve Corporation, Baker Hughes, and IMI Critical Engineering.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Valves from Water Treatment Plants

- 4.1.2 Increasing Demand for Valves in the Oil and Gas Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Capital Investment to Hamper the Market Growth

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 By Type

- 5.1.1 Butterfly Valve

- 5.1.2 Ball Valve

- 5.1.3 Globe Valve

- 5.1.4 Gate Valve

- 5.1.5 Plug Valve

- 5.1.6 Other Types

- 5.2 By Product

- 5.2.1 Quarter-turn Valve

- 5.2.2 Multi-turn Valve

- 5.2.3 Other Products (Control Valves)

- 5.3 By Application

- 5.3.1 Power

- 5.3.2 Water and Wastewater Management (Including Desalination)

- 5.3.2.1 Metal, Mineral, and Mining

- 5.3.2.2 Other Applications

- 5.3.3 By Chemicals

- 5.3.4 Oil and Gas

- 5.3.4.1 Upstream

- 5.3.4.2 Mid-stream

- 5.3.4.3 Downstream

- 5.3.5 Food Processing

- 5.3.6 Pulp and Paper

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Malaysia

- 5.4.6 Thailand

- 5.4.7 Indonesia

- 5.4.8 Vietnam

- 5.4.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Alfa Laval

- 6.3.2 AVK Holding AS

- 6.3.3 Baker Hughes

- 6.3.4 CIRCOR International Inc.

- 6.3.5 Crane Co.

- 6.3.6 Curtiss-Wright Corporation

- 6.3.7 Danfoss AS

- 6.3.8 EBRO ARMATUREN Gebr. Brer GmbH

- 6.3.9 Emerson Electric Co.

- 6.3.10 Flowserve Corporation

- 6.3.11 Georg Fischer Ltd

- 6.3.12 Hitachi Metals Ltd

- 6.3.13 Honeywell International Inc.

- 6.3.14 IMI Critical Engineering

- 6.3.15 ITT Inc.

- 6.3.16 KITZ Corporation

- 6.3.17 NIBCO

- 6.3.18 Okano Valve Mfg. Co. Ltd

- 6.3.19 PARKER HANNIFIN CORP.

- 6.3.20 SAMSON AKTIENGESELLSCHAFT

- 6.3.21 Schlumberger Limited

- 6.3.22 The Weir Group PLC

- 6.3.23 Valvitalia SpA

- 6.3.24 Velan Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日