産業用バルブ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Industrial Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1852153

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

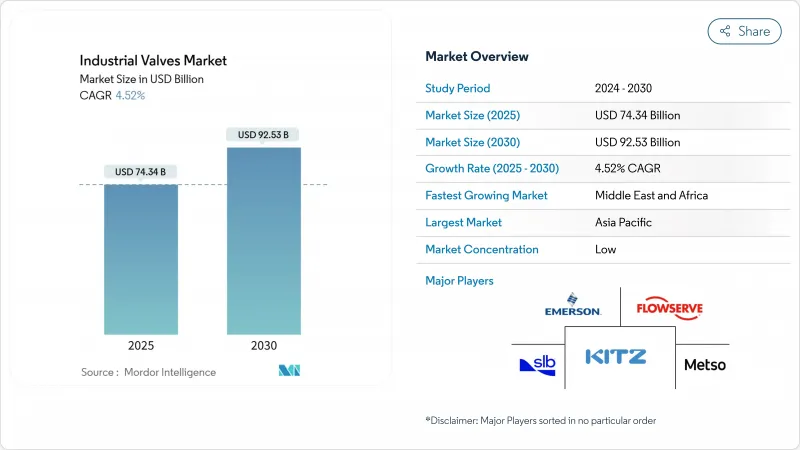

産業用バルブ市場規模は2025年に743億4,000万米ドルと推定・予測され、2030年には925億3,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは4.52%です。

この着実な拡大は、水素、LNG、海水淡水化インフラの同時成長と、石油・ガス海洋支出の循環的回復に支えられています。予知保全への投資の増加や排ガス規制の厳格化によって交換サイクルが加速する一方、ニッケル基合金のサプライチェーンのボトルネックによって材料の代替が余儀なくされています。ティアワン・サプライヤーは、水素サービス用バルブの認証取得やデジタル診断の統合を競っているため、競合の激しさは増しており、こうした力学が相まって、産業用バルブ市場はエネルギー転換期にも底堅さを維持しています。

世界の産業用バルブ市場の動向と洞察

水素と炭素回収プロジェクト

欧州と北米では、水素バレーと炭素回収ハブが拡大しており、水素脆化とCO2腐食に耐える高圧・高純度バルブが急務となっています。欧州大陸では既に512の水素施設が稼動しており、その生産能力は11.23Mtに達しています。プロジェクト開発者は、電解槽のバランスオブプラントサービス用に、認証済みのクォーターターン設計を引き続き支持しています。バルブサプライヤーは、エマソンのHV-7000シリーズのような専用設計の製品で対応しており、自動車への燃料補給用に700バールまでの2段階減圧を実現しています。水素の準備態勢を固めようとする動きは、認定コストを上昇させるが、同時に割高な価格設定ウィンドウを生み出し、産業用バルブ市場に有意義なボリュームを追加します。水素の厳しい排ガス規制は、低透過ステムシールを備えたメタルシートボールバルブへの需要をさらに高める。公的資金による政策枠組みが2030年までに900億ユーロを水素に充当する予定であることから、プロジェクトパイプラインは十分な規模があり、特殊バルブパッケージの持続的な2桁台の受注増を支えています。

LNGターミナルの建設

世界のLNG消費量は、中国の工業用ユーザーと南アジア・東南アジアの新規需要センターが牽引し、2040年までに増加すると予想されています。中国だけが世界の再ガス化能力増設をリードし、米国は2024年の2%増から2025年にはLNG輸出を18%増加させる勢いです。液化トレインや再ガス化バースを新設するごとに、数千の極低温ボールバルブ、プラグバルブ、ゲートバルブが必要になります。米国メキシコ湾岸では最大20%の人件費インフレが発生しているもの、供給契約は堅調に推移しており、LNGインフラは産業用バルブ市場の当面の起爆剤となります。オリジナル機器の販売が主流であるが、既存ターミナルのデボトルネック解消を目的としたターンバック・プロジェクトにより、スマートアクチュエータとポジショナーの有利なレトロフィット収益が追加されます。

ニッケル基合金の不足

電池セクターの普及により、ニッケル需要は2019年から2023年の間に200%以上増加し、バルブグレード合金の供給が逼迫しています。マット原料の93%はインドネシアから中国への流れによって管理されているため、高合金鋳物のリードタイムは現在40週間を超えており、極低温バルブやサワーバルブの納入を妨げています。メーカーは、低ニッケル二相鋼の代替に軸足を移しつつあるが、認定サイクルの切り替えは遅れています。9%ニッケル鋼またはインコネルトリムを必要とするLNGおよび水素プロジェクトの足かせとなり、産業用バルブ市場の目先の成長は縮小しています。

セグメント分析

ボールバルブは、漏れのないシャットオフ、素早い1/4回転動作、ピガブルパイプラインとの互換性により、2024年の産業用バルブ市場の40%を占めています。最近の製品革新は、水素透過に耐えるポリマーシート設計に重点を置いており、より幅広いボールバルブ製品群の中でプレミアムニッチを可能にしています。同時に、逆流防止に重要な逆止弁は、LNGタンク・農場ポンプ隔離や自治体の水道網への投資の増加に支えられ、CAGR 7.11%で成長すると予測されています。静音作動のデュアルプレートスタイルは、ウォーターハンマーを軽減し、下流の資産を保護するため、シェアを伸ばしています。

ボール、バタフライ、プラグ構造の1/4回転バルブは、2024年の売上高の54%を占めています。そのコンパクトなフットプリント、低トルク、短い作動時間は、製油所のマニホールドや配水ループにおける調達の選択を支え続けています。多回転バルブは、精密な絞りが最も重要な場合に成長が加速する(CAGR 5.8%)が、ISO-5211の取り付けパッドがアクチュエーターの統合を容易にするため、自動化指令の増加は依然として1/4回転設計を支持しています。エマソンのAVENTICS XVシリーズなどの新製品は、旧世代の2倍のエアフローを実現し、空気圧ネットワークのサイクルタイムを短縮します。

地域分析

産業用バルブ市場は、アジア太平洋地域が2024年の支出額の40%を占めてリードしています。この地域の勢いは、中国の石油化学コンビナート、インドの分散型水処理施設の建設、LNG受入ターミナルの台頭から生じています。中国は2030年までに世界の再ガス化プロジェクトの大部分を開始すると予測されており、極低温隔離弁や緊急遮断弁に対する現場での要求が高まっています。

米国では2025年に18%のLNG輸出拡大が計画されており、圧力開放、アンチサージ、ブローダウンパッケージの設置が短期的に相次ぐ。予測分析によってターンアラウンド・サイクルが短縮されるメキシコ湾岸の化学工業地帯では、デジタル改修が加速しています。カナダの炭素回収奨励策も、CO2輸送ネットワークにおける耐腐食性合金バルブの需要を刺激しています。

欧州市場は、加速する水素への取り組み、環境コンプライアンス、老朽化したインフラの更新を反映しています。中東とアフリカはCAGR 6.51%で最も急成長している地域です。サウジアラビアとアラブ首長国連邦はGCC海水淡水化処理量の65%を占めており、2050年までに8,000万m3/日に拡大することが、バルブ調達のパイプラインの大きさを示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 水素と炭素回収プロジェクトの拡大が欧州と北米の高圧バルブ需要を牽引

- バルブを必要とするAPAC全域のLNGターミナル建設

- GCCにおける海水淡水化プラント投資の加速がバルブの売上を押し上げる

- 予知保全プラットフォームの急速な導入で北米化学プラントのバルブの交換サイクルが上昇

- オフショア深海エネルギー・電力設備投資回復がバルブ受注を刺激

- 市場抑制要因

- ニッケル基合金鋳物のサプライチェーン不足でリードタイムが40週間を超える

- ダクタイル鋳鉄の価格変動が欧州の公益事業バイヤーの総所有コストを増加させる

- 排ガス規制の強化が中堅・中小メーカーの資格取得コストを上昇させる

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品・サービスの脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- ボールバルブ

- バタフライバルブ

- ゲートバルブ

- グローブバルブ

- プラグバルブ

- その他のタイプ

- 製品別

- クォーターターンバルブ

- マルチターンバルブ

- その他の製品

- バルブ機能別

- アイソレーションバルブ

- レギュレーションバルブ

- 逆止弁および安全弁

- ボディ素材別

- スチール(炭素鋼およびステンレス鋼)

- 合金ベース(デュプレックス、インコネルなど)

- 鋳鉄/ダクタイル鋳鉄

- 極低温ニッケル合金

- その他

- 用途別

- 石油・ガス

- 電力

- 上下水道管理

- 化学

- 新エネルギー

- その他の用途

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- インドネシア

- ベトナム

- マレーシア

- タイ

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- 北欧諸国

- トルコ

- ロシア

- スペイン

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Alfa Laval

- AVK International A/S

- Baker Hughes Company

- Circor International Inc.

- Crane Company

- Curtiss-Wright Corporation

- Danfoss A/S

- Emerson Electric Co.

- Flowserve Corporation

- Georg Fischer Ltd.

- Hitachi Ltd

- Honeywell International Inc.

- IMI Critical Engineering(IMI PLC)

- ITT Inc.

- KITZ Corporation

- KLINGER Holding

- Metso

- Mueller Co. LLC

- Nibco Inc.

- Okano Valve Mfg. Co. Ltd.

- SAMSON AKTIENGESELLSCHAFT

- SLB

- Technipfmc PLC

- The Weir Group PLC

- Valvitalia SpA

- Velan

- Xylem

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日