東南アジアおよび中東・アフリカの小型武器・弾薬:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Southeast Asia, Middle-East And Africa Small Arms And Ammunition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690926

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

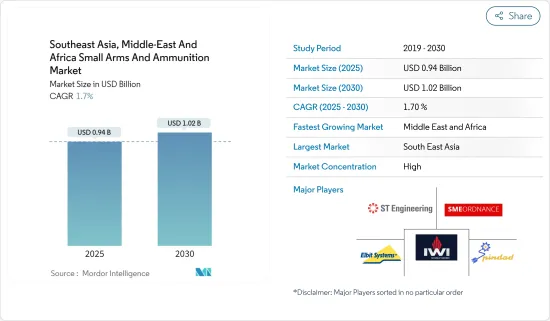

東南アジアおよび中東・アフリカの小型武器・弾薬市場規模は2025年に9億4,000万米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは1.7%で、2030年には10億2,000万米ドルに達すると予測されます。

近隣諸国との緊張が高まる中、東南アジアや中東のいくつかの国では、小型武器や弾薬の調達を強化しています。軍事・法執行要員の訓練が一貫して需要の原動力であることに変わりはないが、国境紛争、過激派の脅威、内乱といった要因が、こうした武器の必要性を増幅させています。

近年、政府の後押しを受けて、UAE、サウジアラビア、東南アジアの一部の国々の武器・弾薬メーカーが、市場での存在感を着実に高めています。トルコ、UAE、サウジアラビアで急成長する国防部門は、既存・新規市場参入者双方に新たな課題を突きつける構えです。

弾薬の国内生産を強化する動きが鮮明になっており、費用対効果の高い労働力を求める外国企業にとって、これらの国々は魅力的な進出先となりつつあります。しかし、この動向は現地の防衛企業に課題を突きつける可能性がある一方で、先進兵器を導入する新規参入企業に門戸を開くことにもなります。しかし、技術的な制約が今後数年間の需要見通しを弱める可能性があることは注目に値します。

東南アジアおよび中東・アフリカの小型武器・弾薬市場動向

予測期間中は軍事セグメントが市場を独占する見込み

軍事セグメントは現在、市場で圧倒的な地位を占めており、予測期間中もこのリードを維持する見通しです。世界の軍事行動の増加に伴い、軍隊は戦闘需要を満たすためにより強力な小型武器にますます目を向けるようになっています。軍用装甲の進歩に伴い、周期的な衝撃を与え、敵により大きなダメージを与える銃器が重視されるようになっています。多くの国が、最新の小火器を積極的に調達し、兵器庫を整備しています。例えば、2022年4月のインド防衛エキスポで、インドネシア警察はKale Kalip(トルコ)からトルコ製半自動拳銃KMR762を確保しました。同時に、インドネシア陸軍はKNG-C5ライフルを発注しました。さらに2022年3月、インドネシアは半自動狙撃銃KMR 762ライフルを武器庫に加えました。2023年9月、バングラデシュ警察は、散弾銃弾35,000発、空砲弾6,000発、催涙ガス弾3.22,000発、狙撃ライフル30丁、その他暴動鎮圧に不可欠な物品を含む大幅な調達を行い、在庫を増強しました。

中東や東南アジアの武器・弾薬製造部門では、現地化の取り組みが急増しています。これらの地域の政府は、軍事調達戦略において、現地生産と再投資オフセットを義務付ける傾向が強まっています。2022年11月、マレーシアのMaruss Sdn BhdとインドネシアのPT Pindadは、武器製造に関する極めて重要な覚書に調印しました。この提携は、さまざまな口径の弾薬供給と並んで、小型武器とその部品の受託製造に踏み込むことを目的としています。このような取り組みにより、軍事分野の成長が促進されることになります。

サウジアラビアは予測期間中に著しい成長を遂げる見込み

予測期間中、サウジアラビアは、防衛能力の強化や次世代兵器への前進に向けた政府の多額の投資により、大幅な市場成長が見込まれています。2023年、サウジアラビアは世界第5位の国防支出国となり、755億米ドルの予算が割り当てられ、顕著な伸びを示しました。

現在の地政学的情勢を考えると、サウジアラビアの近隣諸国(北はイラク、ペルシャ湾を挟んでイラン、南はイエメンなど)は大きな脅威となっており、弾薬の購入を優先する必要があります。準軍事部隊を含む50万人を超える軍事力を持つサウジの要員は、主にFN F2000(5.56x45ミリ)、ブッシュマスターM4タイプ(5.56x45ミリ)、FNファイブセブン(5.7x28ミリ)、ORSIS T-5000(7.62x51ミリNATO)などの銃器に依存しています。

サウジアラビアは多額の軍事費を支出しているにもかかわらず、現在、地元の防衛企業を支援しているのはわずか2%に過ぎず、世界有数の武器・弾薬輸入国となっています。この依存度を下げるため、政府はビジョン2030の一環として、2030年までに国産軍備費を50%に引き上げることを目指しています。ビジョン2030の重要なイニシアチブは、サウジアラビア軍だけでなく中東や北アフリカの他の国々のために様々な弾薬を生産する国営企業であるサウジアラビア軍産業(SAMI)の設立です。

東南アジアおよび中東・アフリカの小型武器・弾薬産業の概要

東南アジアおよび中東・アフリカの小型武器・弾薬市場を独占しているのは主要企業です。イスラエル兵器産業(IWI)社、エルビット・システムズ社、PT Pindad、SME Ordnance Sdn Bhd社(SMEO)、シンガポール・テクノロジー・エンジニアリング社などです。

近年、政府の後押しを受けて、UAE、サウジアラビア、東南アジアやアフリカの一部の国の国内武器・弾薬メーカーが市場での存在感を着実に高めています。トルコ、UAE、サウジアラビアの防衛セクターの台頭は、既存および新興の市場参入企業への課題となります。特筆すべきは、これらの地域のプレーヤーが最先端技術を提供するだけでなく、NATO軍が使用する装備品の水準に匹敵することです。国際的なOEMと競い合う中で、これらの企業はその先進的な製品で人気を集め、投資家や注文の数を増やしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 武器

- 拳銃

- ライフル

- マシンガン

- ショットガン

- 弾薬

- 致死性

- 非致死性

- 武器

- エンドユーザー

- 民間

- 法執行機関

- 軍事

- 地域

- 東南アジア

- シンガポール

- マレーシア

- インドネシア

- その他の東南アジア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- イスラエル

- バーレーン

- クウェート

- カタール

- オマーン

- その他中東とアフリカ

- 東南アジア

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Singapore Technologies Engineering Ltd

- PT Pindad

- ME Ordnance Sdn Bhd Company(smeo)

- Elbit Systems Ltd

- Saudi Arabian Military Industries(SAMI)

- Oman Munition Production Company(OMPC)

- Jorammo

- Kenya Ordnance Factories Corporation

- Defence Industries Corporation of Nigeria

- Israel Weapon Industries(IWI)Ltd

第7章 市場機会と今後の動向

目次

The Southeast Asia, Middle-East And Africa Small Arms And Ammunition Market size is estimated at USD 0.94 billion in 2025, and is expected to reach USD 1.02 billion by 2030, at a CAGR of 1.7% during the forecast period (2025-2030).

Amid escalating tensions with neighboring nations, several countries in Southeast Asia and the Middle East are ramping up their acquisitions of small arms and ammunition. While military and law enforcement personnel training remains a consistent driver of demand, factors like border disputes, militant threats, and civil unrest amplify the need for these armaments.

Over recent years, bolstered by government backing, local arms and ammunition manufacturers in the UAE, Saudi Arabia, and select Southeast Asian nations have steadily expanded their market presence. The burgeoning defense sectors in Turkey, the UAE, and Saudi Arabia are poised to pose fresh challenges for both incumbent and new market entrants.

With a clear push toward bolstering domestic ammunition production, these nations are becoming attractive destinations for foreign companies eyeing cost-effective labor. However, while this trend may pose challenges for local defense firms, it also opens the door for new players to introduce advanced weaponry. Yet, it's worth noting that technological constraints could temper the demand outlook in the coming years.

Southeast Asia, Middle-East And Africa Small Arms And Ammunition Market Trends

The Military Segment is Expected to Dominate the Market During the Forecast Period

The military segment currently holds a dominant position in the market and is poised to maintain this lead through the forecast period. As global military engagements rise, armed forces are increasingly turning to more potent small arms to meet combat demands. With advancements in military armor, there is a heightened emphasis on firearms that deliver cyclical impacts, inflicting greater damage on adversaries. Many nations are actively procuring and advancing their arsenals with the latest small arms. For example, at the April 2022 Indian Defense Expo, the Indonesian Police secured Turkish Semi-automatic KMR762 pistols from Kale Kalip (Turkey). Concurrently, the Indonesian Army placed orders for KNG-C5 rifles. Additionally, in March 2022, Indonesia added a semi-automatic sniper KMR 762 rifle to its arsenal. In September 2023, the Bangladeshi Police bolstered its inventory with a significant procurement, including 35 lakh shotgun bullets, 6 lakh blank cartridges, 3.22 lakh tear gas shells, 30 sniper rifles, and other essential riot control items.

The arms and ammunition manufacturing sector in the Middle East and Southeast Asia witnessed a surge in localization efforts. Governments in these regions are increasingly mandating local production and re-investment offsets in their military procurement strategies. In November 2022, Malaysia's Maruss Sdn Bhd and Indonesia's PT Pindad inked a pivotal memorandum of understanding (MoU) for arms manufacturing. This collaboration aims to delve into contract manufacturing for small arms and their components alongside ammunition supplies of varying calibers. Such initiatives are set to propel the growth of the military segment.

Saudi Arabia is Anticipated to Witness Significant Growth During the Forecast Period

During the forecast period, Saudi Arabia is poised for significant market growth, driven by the government's substantial investments in bolstering its defense capabilities and advancing to the next generation of weaponry. In 2023, the nation ranked as the world's fifth-largest defense spender, allocating a budget of USD 75.5 billion, marking a notable increase.

Given the current geopolitical landscape, Saudi Arabia's neighboring nations-such as Iraq to the north, Iran across the Persian Gulf, and Yemen to the south-present considerable threats, underscoring the nation's need to prioritize ammunition purchases. With a military force exceeding half a million, including paramilitary units, Saudi personnel predominantly rely on firearms like the FN F2000 (5.56x45 mm), Bushmaster M4-Type (5.56x45 mm), FN Five-seven (5.7x28 mm), and ORSIS T-5000 (7.62x51 mm NATO).

Despite its significant military spending, only 2% currently supports local defense firms, making Saudi Arabia the world's leading arms and ammunition importer. To reduce this reliance, as part of Vision 2030, the government aims to elevate local military equipment spending to 50% by 2030. A key initiative under Vision 2030 is the establishment of Saudi Arabian Military Industries (SAMI), a state-owned entity producing a range of ammunition not just for Saudi forces but also for other nations in the Middle East and North Africa.

Southeast Asia, Middle-East And Africa Small Arms And Ammunition Industry Overview

Key players dominate the small arms and ammunition market in Southeast Asia and the Middle East and Africa. These include Israel Weapon Industries (IWI) Ltd, Elbit Systems Ltd, PT Pindad, SME Ordnance Sdn Bhd Company (SMEO), and Singapore Technologies Engineering Ltd.

In recent years, bolstered by government backing, domestic arms and ammunition manufacturers in the UAE, Saudi Arabia, and select nations in Southeast Asia and Africa have steadily expanded their market presence. The rising defense sectors in Turkey, the UAE, and Saudi Arabia are set to challenge both established and emerging market entrants. Notably, these regional players not only offer cutting-edge technology but also match the caliber of equipment used by NATO forces. As they vie with international OEMs, these firms are gaining traction for their advanced offerings and attracting a growing number of investors and orders.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness-Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Arms

- 5.1.1.1 Handguns

- 5.1.1.2 Rifles

- 5.1.1.3 Machine Guns

- 5.1.1.4 Shotguns

- 5.1.2 Ammunition

- 5.1.2.1 Lethal

- 5.1.2.2 Non-lethal

- 5.1.1 Arms

- 5.2 End User

- 5.2.1 Civil

- 5.2.2 Law Enforcement

- 5.2.3 Military

- 5.3 Geography

- 5.3.1 Southeast Asia

- 5.3.1.1 Singapore

- 5.3.1.2 Malaysia

- 5.3.1.3 Indonesia

- 5.3.1.4 Rest of Southeast Asia

- 5.3.2 Middle East and Africa

- 5.3.2.1 Saudi Arabia

- 5.3.2.2 United Arab Emirates

- 5.3.2.3 Turkey

- 5.3.2.4 Israel

- 5.3.2.5 Bahrain

- 5.3.2.6 Kuwait

- 5.3.2.7 Qatar

- 5.3.2.8 Oman

- 5.3.2.9 Rest of Middle East and Africa

- 5.3.1 Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Singapore Technologies Engineering Ltd

- 6.2.2 PT Pindad

- 6.2.3 ME Ordnance Sdn Bhd Company (smeo)

- 6.2.4 Elbit Systems Ltd

- 6.2.5 Saudi Arabian Military Industries (SAMI)

- 6.2.6 Oman Munition Production Company (OMPC)

- 6.2.7 Jorammo

- 6.2.8 Kenya Ordnance Factories Corporation

- 6.2.9 Defence Industries Corporation of Nigeria

- 6.2.10 Israel Weapon Industries (IWI) Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日