|

市場調査レポート

商品コード

1911265

欧州のプレハブ住宅市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Prefabricated Housing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のプレハブ住宅市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

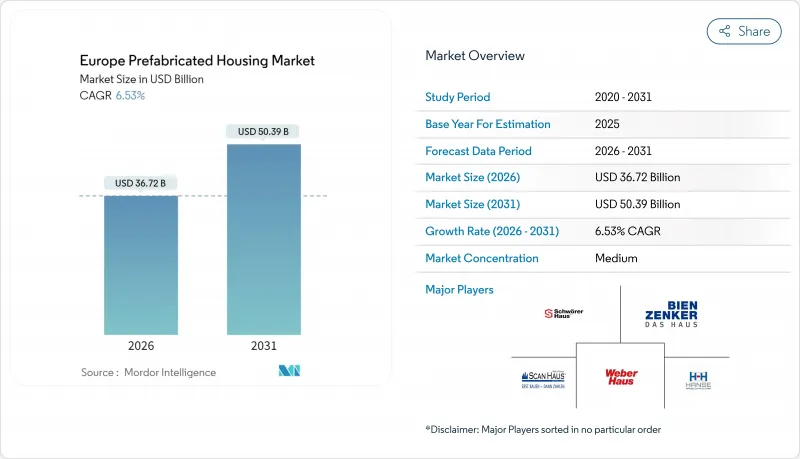

欧州のプレハブ住宅市場は、2025年に344億7,000万米ドルと評価され、2026年の367億2,000万米ドルから2031年までに503億9,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは6.53%と見込まれています。

この成長軌跡は、同セグメントがニッチな建築手法から大陸全体における主流の住宅ソリューションへと移行していることを示しています。排出ゼロ義務化の強化、持続的な住宅不足、オフサイト製造技術の急速な進歩が相まって、採用が加速しています。エネルギー性能規制では再生可能エネルギーシステムを組み込んだ工場生産の外装が優遇され、ロボット技術とBIMを活用した生産により建設期間が最大50%、プロジェクトコストが20%削減されています。

投資家が持続可能な不動産ファンドに過去最高額を投入する中、欧州のプレハブ住宅市場は、特に木材などのカーボンネガティブ素材にグリーンファイナンス優遇措置を結びつける国々において、新築建設活動におけるシェア拡大の機運が高まっています。既存企業が設計から設置まで垂直統合を進め、技術系スタートアップが労働力不足のリスクを軽減する自動化マイクロ工場を導入するにつれ、競合の激化が進んでいます。

欧州プレハブ住宅市場の動向と洞察

EU改修計画とエネルギー性能指令が省エネ型プレハブ改修を促進

建築物のエネルギー性能に関する指令(EPBD)の改正により、加盟国は2030年までに非住宅ストックの下位16%の改修を実施し、同年に新築建物の現場排出量をゼロとする義務を負います。このため各国政府は、予測可能な断熱性能と廃棄物削減を実現する標準化された工場生産の壁・屋根・ファサードモジュールを推進しています。ドイツの実施計画では、建設期間を半減させ、ISO 14001マネジメントシステムに基づく検証可能な炭素削減効果を示す手段として、オフサイト組立を重視しています。グリーン住宅ローン制度は需要をさらに拡大し、認定プレハブ外装を選択する世帯の金利マージンを削減する一方、公共機関は連続契約枠組みを通じて学校や病院の改修を加速させています。

200万戸の低価格住宅不足が連続建設入札を促進

ユーロスタットの推計によれば、欧州全体で約200万戸の手頃な住宅が不足しており、当局は反復可能な体積型またはパネル化設計を指定した一括調達を実施しています。ベルリンの公益企業ゲヴォバッグは、モジュラー入札規則により、1,500戸の社会住宅を18ヶ月未満で完成させ、都心部の平均建設費を50%下回る単価を実現しました。英国の「パン・ロンドン・アコモデーション・コラボレーティブ・エンタープライズ」は、7,500万ポンド規模の可搬式住宅枠組み契約を導入し、社会的目標とエネルギー目標の両方を満たす精密製造への政治的コミットメントを示しました。連続契約が東欧へ移行する中、国境を越えた建築基準に対応する建築システムを標準化するサプライヤーが、規模拡大に最も有利な立場にあります。

二桁の投入コスト上昇がプレハブ住宅の価格優位性を損なう

EU建設コスト指数は2024年12月に117.00ポイントに達し、セメント価格が前年比27.5%上昇、構造用鋼材が42%急騰したことを反映しています。プレファブ工法は従来、現場施工工法より15%安価でしたが、コスト重視のプロジェクト、特に低価格住宅では現在、価格差が消滅するリスクに直面しています。持続可能な森林管理の割当により広葉樹の伐採が制限され、製材用丸太価格が上昇し、モジュール生産者の利益率が縮小しています。固定価格の公共契約に縛られた企業は顕著な利益率圧迫に直面しており、先物購入契約を通じて原材料リスクをヘッジする必要性が高まっています。

セグメント分析

2025年、木材は欧州のプレハブ住宅市場シェアの53.62%を占めました。これは、分類体系(タクソノミー)連動型資金調達と整合する炭素固定化の利点によるものです。このセグメントは2031年までCAGR7.05%で推移し、鉄鋼やコンクリートを上回る成長が見込まれます。スウェーデンでは公共事業において大規模木造構造を優先する建築基準改正が導入され、クロスラミネート材の需要が加速しています。KLEUSBERG社が開発した木鋼ハイブリッドフレームは、構造剛性を維持しつつ中層都市再開発への木材適用範囲を拡大。コンクリートは基壇・基礎に不可欠ですが、再生骨材を組み込むことで埋蔵炭素を削減するプリントレンガ代替材によりシェアが漸減中です。

ガラスや先進複合材などの二次材料は、太陽光発電セルを統合した高機能ファサードシステムなど、特定の性能ニーズを満たします。鋼材は長スパンを必要とするボリュームポッドで依然重要ですが、輸入価格の上昇により、供給業者は軽量合金やモジュラー接続詳細を採用し、使用量を削減する方向へ移行しています。EUの循環型経済政策は確立されたリサイクルループを持つ材料を優遇しており、この基準は現在プレファブ供給チェーンに参入しつつあるアルミニウムカーテンウォールシステムに有利に働きます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUの「改修の波」およびエネルギー性能指令(EPBD)の義務化が、省エネ型プレハブ改修の推進を後押ししております。

- 手頃な価格の住宅が200万戸不足している状況が、連続建設入札の急増を後押ししています。

- 熟練労働者不足によるギャップを埋める工場自動化とロボティクス。

- グリーンファイナンス分類体系が木材モジュールの住宅ローン金利低減への道を開きます。

- NATO及び民間防災契約が迅速展開型ボリュームユニットの需要を加速させております。

- BIM統合型3Dプリント技術により基礎工事のリードタイムを25%短縮

- 市場抑制要因

- 二桁の投入コストインフレがプレハブ住宅の価格優位性を損なう

- 全国的に統一されていない建築基準法と保証規則が承認手続きを遅延させております

- 道路護送及び幅制限により、大型モジュールの物流コストが増加します

- 「カタログ住宅」というイメージが密集した都市中心部での需要を抑制しています

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- プレハブ住宅に用いられる様々な構造の概要

- プレハブ住宅のコスト構造分析

第5章 市場規模と成長予測

- 素材タイプ別

- コンクリート

- ガラス

- 金属

- 木材

- その他材料

- 住宅タイプ別

- 一戸建て

- 集合住宅

- 製品タイプ別

- モジュラー住宅

- パネル化・部品化システム

- 製造住宅

- その他のプレハブ住宅タイプ

- 国別

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- スウェーデン

- デンマーク

- ノルウェー

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- SchworerHaus

- Hanse Haus GmbH

- WeberHaus GmbH & Co.

- Bien-Zenker GmbH

- DFH Haus Holding AG(Massa/Allkauf)

- ScanHaus Marlow GmbH

- Goldbeck GmbH(Modular Housing)

- HUF Haus GmbH

- Danwood S.A.

- Kampa GmbH

- FingerHaus GmbH

- Baufritz GmbH & Co.

- Luxhaus GmbH

- Kleusberg GmbH

- Redbloc Elemente GmbH

- Laing O'Rourke(Explore Modular EU)

- Skanska AB(BoKlok Europe)

- Bouygues Construction(Housing Europe)

- Eiffage Construction Europe

- Lindbacks Bygg

- Clayton Homes

- Skyline Champion Corp.

- Cavco Industries Inc.

- Sekisui House Ltd(European arm)