天然食品着色料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Natural Food Colorants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 156 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690831

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

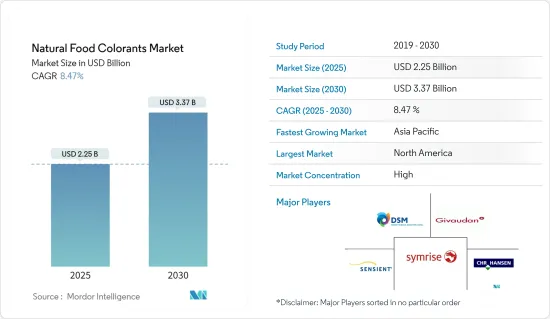

天然食品着色料の市場規模は2025年に22億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.47%で、2030年には33億7,000万米ドルに達すると予測されています。

COVID-19の大流行によって、食品の出所を知りたいという消費者の欲求が高まる一方、食品の値ごろ感は世界中の消費者の間でより大きな関心事として続いています。さらに、消費者は、原材料の原産地が特定されていない謎めいた輸入品を多く消費することで感染することを恐れているため、地元産の食品に対する需要が高まっています。このことは、天然着色料の地場メーカーだけでなく、食品業界に新規参入するプライベートブランド企業にも利益をもたらしています。

世界のCOVID-19パンデミックの蔓延を抑制し、最終的には食い止めるという継続的な要求が生まれる中、世界の科学界や医学界は、健康と免疫力を向上させるために栄養補助食品の使用を推奨しており、これは天然着色料業界にとって有利です。

スーパーフードの高い機能性は、「天然」という用語に対する肯定的な認識とともに、市場における天然食品着色料の需要を高める主な要因となっています。消費者は、シンプルで分かりやすいラベルの製品を使用することに大きな魅力を感じており、食品会社は、業界に存在する他の代替品よりも着色食品を選ぶことを後押ししています。

しかし、高い抽出コストと高価な原材料は、主に発展途上国の食品メーカーが、より健康的な食品を常に追い求める大手企業やブランドのように進歩的であることを妨げています。この要因は、天然食品着色料が業界で上回ることを制限する、重大な市場制約として強く認識されています。

天然食品着色料の市場動向

食材の着色へのスポットライトの輝き

食品着色料は、食品を着色するという形で、現在付加価値製品と倫理的消費者主義によって牽引されている食品業界にとって革命に勝るとも劣らないものであることが証明されています。消費者の関心は、健康志向であるだけでなく、倫理的に調達され、環境への影響をまったく、あるいは最小限にとどめる食品に向けられています。さらに、これは天然食品着色料の需要を押し上げ、市場の商業的可能性を最大限に引き出すために、これまでにない技術を導入する研究開発活動に重点を置いています。例えば、2019年、Naturexはスピルリナベースの着色食品であるVegebrite(R)Ultimate Spirulinaを発表しました。これは水ベースの抽出プロセスを使用し、クリーンラベルとトレハロースフリーの処方を提供することで100%天然のソリューションを保証します。様々な濃度と形態で入手可能です。

このような消費者行動の変化と食品着色料の市場力学は、食品メーカーが食品に人工添加物を配合するのをやめさせようとしています。その結果、Kellogg's、General Mills、Nestle SA、Campbell、Kraftなどの大手食品会社は、予測期間中、自社製品の処方から人工添加物や着色料の使用を制限することを確約しており、天然着色料の有望な未来を描いています。

アジア太平洋地域が市場の急成長地域

アジア太平洋地域の主要な天然着色料メーカーは、様々な応用技術を有しており、幅広い飲食品用途で着色料の性能を試験するために利用することができます。これには、清涼飲料、アルコール飲料、菓子類、冷菓、ヨーグルト、焼き菓子、加工食品などが含まれるが、これらに限定されないです。天然着色料は、様々な理由からアジアの飲食品業界で使用されています。食品をより魅力的に見せたり、様々な用途に関連する風味を強調したり識別したりします。同地域ではハーブやスパイスが広く栽培されているため、アジアの原料会社はターメリック、赤唐辛子、ハイビスカスなど様々なスパイスから食品着色添加物の開発を始めました。パプリカ、クルクミン、ハイビスカスの組み合わせから、黄色、赤色、ピンク色、オレンジ色などの複数の色合いを提供しています。これらの着色料は、デザートや飲料用途で人気があります。

特に中国は、2020年のAPAC市場全体で50%以上のシェアを占めており、アジア太平洋で最大の市場を占めています。中国の食品着色料市場は、食品を魅力的に見せる天然由来の食品着色料の高度な使用によって牽引されています。中国料理で使用される人気の高い天然食品着色料には、カルミン、ビキシン、ノルビキシン、カロテノイド、クルクミン、アントシアニン、ベタニン、フィコビリンなどがあります。

天然食品着色料産業の概要

調査対象市場は、Chr. Hansen Holding AS、Givaudan(Naturex)、Koninklijke DSM NV、Sensient Technologies、Symrise AGなど、2020年の市場シェアにより主要企業として浮上した数社で固められています。調査対象となった市場の主要企業は、製品革新と事業拡大への依存を強めており、中でも最も採用されている戦略となっています。過去数年間、研究開発への大規模な投資が行われ、その結果、市場に数多くの新製品が導入されました。さらに、DDW、The Color House、Sensient Technologiesなどのメーカーでは、合併・買収も重要な戦略となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- ベーカリー

- 乳製品

- アイスクリーム

- その他の製品

- 飲料

- アルコール飲料

- ノンアルコール飲料

- 菓子類

- 栄養補助食品

- スナックとシリアル

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- 英国

- ドイツ

- イタリア

- ロシア

- スペイン

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 市場シェア分析

- 主要企業の戦略

- 企業プロファイル

- Chr. Hansen Holding AS

- Synthite Industries Private Ltd

- Kalsec Inc.

- Givaudan SA

- Symrise AG

- DDW Inc.

- Koninklijke DSM NV

- Sensient Technologies

- Archer Daniels Midland Company

第7章 市場機会と今後の動向

目次

The Natural Food Colorants Market size is estimated at USD 2.25 billion in 2025, and is expected to reach USD 3.37 billion by 2030, at a CAGR of 8.47% during the forecast period (2025-2030).

The COVID-19 pandemic has increased consumers' desire to know where their food comes from, while food affordability continues as a greater concern among consumers worldwide. Moreover, the demand for locally produced food has escalated because the consumers are afraid of being infected by consuming more imported products that have a mysterious and unspecified ingredient origin. This has, in turn, benefited the new private label entrants in the food industry, as well as the local manufacturers of natural colorants.

As the situation generates continuous demands to suppress and ultimately stifle the spread of the global COVID-19 pandemic, the world's scientific and medical communities recommend the use of nutraceuticals to improve health and immunity, which is advantageous for the natural food colorant industry.

The high functionality of superfood, along with the positive perception of the term 'natural,' has been the primary attribute raising the natural food colorant demand in the market. Consumers are greatly fascinated to use products with simple and understandable labels, which is pushing food companies to instead opt for coloring foodstuffs than other alternatives present in the industry.

However, the high cost of extraction and expensive raw materials discourage food manufacturers, primarily in developing countries, from being as progressive as big firms and brands that are constantly rooting for healthier food products. This factor is strongly identified as a significant market constraint, restricting natural food colorant to outperform in the industry.

Natural Food Colorants Market Trends

Brightening Spotlight on Coloring Foodstuff

Food colors, in the form of coloring foodstuffs, have proven as no less than a revolution for the food industry that is currently being driven by value-added products and ethical consumerism. Consumers redirect their interest toward food products that are not only health-oriented but are ethically sourced, leaving none or least impact on the environment. Moreover, this thrusts the demand for natural food colorants and stresses R&D activities to introduce unprecedented technologies in order to exploit the maximum commercial potential of the market. For instance, in 2019, Naturex introduced Vegebrite(R) Ultimate Spirulina, a spirulina-based coloring foodstuff that uses a water-based extraction process to ensure a 100% natural solution by delivering clean-label and trehalose-free formulations. It is available in various concentrations and formats.

This changing consumer behavior and market dynamics for food colorants are pushing food manufacturers to quit formulating artificial additives in food products. As a result, major food companies, such as Kellogg's, General Mills, Nestle SA, Campbell, and Kraft, have assured to restrict the use of artificial additives and colorants from their product formulations, portraying promising future for natural colorants, during the forecast period.

Asia-Pacific is the Fastest-growing Region in the Market

The leading natural food colorant manufacturers across the region possess a variety of application technologies, which they can utilize to test the performances of colors in a wide range of food and beverage applications. These include but are not limited to soft drinks, alcoholic drinks, confectionery, frozen desserts, yogurts, baked goods, and processed foods. Natural food colors are used in the Asian food and beverage industry for various reasons. They make food products more visually appealing and emphasize or identify flavors normally associated with various applications. Owing to the wide cultivation of herbs and spices in the region, Asian ingredient companies started developing food coloring additives from various spices like turmeric, red chilies, and hibiscus. They offer multiple tints of yellow, red, pink, and orange colors from the combinations of paprika, curcumin, and hibiscus. These colorants are popular in desserts and beverage applications.

Notably, China represents the largest market in Asia-Pacific as the country accounted for more than 50% share across the APAC market in 2020. The Chinese food colorants market is driven by the advanced usage of naturally derived food colorants making the food appear attractive. A few of the popular natural food colorants used in Chinese food cuisines are carmine, bixin and norbixin, carotenoids, curcumin, anthocyanin, betanin, and phycobilin.

Natural Food Colorants Industry Overview

The market studied is consolidated with few companies that emerged as the leading players owing to their market share in 2020, including Chr. Hansen Holding AS, Givaudan (Naturex), Koninklijke DSM NV, Sensient Technologies, and Symrise AG. The key players in the market studied are increasingly relying on product innovation and business expansion as the most adopted strategies among all others. There has been an extensive investment in R&D in the past years, which led to the introduction of numerous new products in the market. Moreover, merger and acquisition was another important strategy among manufacturers like DDW, The Color House, and Sensient Technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Bakery

- 5.1.2 Dairy-based Products

- 5.1.2.1 Ice Cream

- 5.1.2.2 Other Products

- 5.1.3 Beverages

- 5.1.3.1 Alcoholic Beverages

- 5.1.3.2 Non-alcoholic Beverages

- 5.1.4 Confectionery

- 5.1.5 Nutraceuticals

- 5.1.6 Snacks and Cereals

- 5.1.7 Other Applications

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 Italy

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 France

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East & Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Egypt

- 5.2.5.4 South Africa

- 5.2.5.5 Rest of Middle-East & Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Chr. Hansen Holding AS

- 6.3.2 Synthite Industries Private Ltd

- 6.3.3 Kalsec Inc.

- 6.3.4 Givaudan SA

- 6.3.5 Symrise AG

- 6.3.6 DDW Inc.

- 6.3.7 Koninklijke DSM NV

- 6.3.8 Sensient Technologies

- 6.3.9 Archer Daniels Midland Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 156 Pages

- 納期

- 2~3営業日