米国のマネージドサービス産業:市場シェア分析、産業動向、成長予測(2025年~2030年)

United States (US) Managed Services Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690744

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

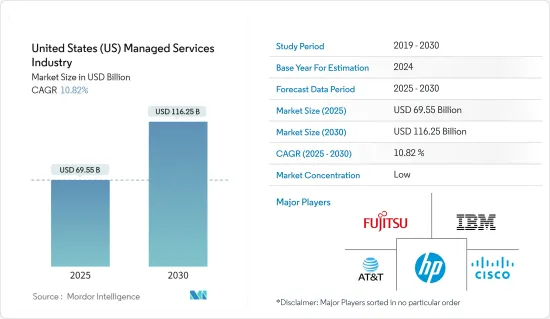

米国のマネージドサービス産業は、2025年の695億5,000万米ドルから2030年には1,162億5,000万米ドルに成長し、予測期間(2025~2030年)のCAGRは10.82%になると予測されます。

主要ハイライト

- マネージドサービスは、特定のIT機能やプロセスをサードパーティプロバイダにアウトソーシングすることで、業務の効率化とコスト削減を目指すものです。このアプローチは、サービス品質、業務効率、顧客満足度を高めると同時に、経費を削減します。

- 市場調査によると、モノのインターネット(IoT)デバイスの急増により、マネージドIoTサービスの需要が高まっており、これらの接続デバイスの安全確保、モニタリング、最適化の必要性が強調されています。これを受けて、ITインフラプロバイダはIoTソリューションの共同開発を進めています。

- ハイブリッドITは、オンプレミスのインフラとクラウドベースのソリューションを組み合わせたものです。モノのインターネット(IoT)の台頭により、企業は顧客エンゲージメント戦略の見直しを迫られています。マネージドサービスプロバイダ(MSP)は、IoTエコシステム内のセキュリティを強化し、堅牢な保護を確保する上で重要な役割を果たしています。

- 米国のマネージドサービス市場展望では、多様な技術の統合と産業規制の遵守がしばしば課題となっています。企業は、マネージドサービスの導入と運用に影響を与える標準や法的要件の網の目をくぐり抜けなければならないです。

- COVID-19の大流行とそれに続く閉鎖が発生した当初は、企業が生き残りに注力し、不要不急の投資を遅らせたため、需要が一時的に落ち込みました。このため、マネージドサービス契約の導入が遅れました。しかし、リモートワークの急増は、セキュリティ、クラウド移行、コラボレーションツール、ネットワーキングの必要性を浮き彫りにし、マネージドサービスプロバイダ(MSP)に産業の成長機会をもたらしました。

米国マネージドサービス産業の動向

クラウドが市場を大きく成長させる

- クラウドベースのマネージドサービスは柔軟性と拡大性を提供し、サービスプロバイダにクラウド環境内の問題へのリモートアクセス、モニタリング、解決を可能にします。さらに、AI/ML、ビッグデータ分析、脅威インテリジェンス、先進的自動化プラットフォームなどの技術の採用が、クラウドベースのサービスへの移行を促進していることが市場データから明らかになっています。市場の参入企業は、産業の動向に応じて革新的で協調的なサービスを開始しています。

- 例えば、2023年11月、世界のサイバーセキュリティプロバイダであるソニックウォールは、何百ものマネージドサービスプロバイダ(MSP)に対応するマネージドセキュリティサービスプロバイダ(MSP)であるSolutions Granted Inc.(SGI)を買収しました。この買収は、ソニックウォールのパートナーに対するコミットメントを強化するものです。米国を拠点とするセキュリティオペレーションセンターサービス(SOCaaS)、マネージドディテクション・アンド・レスポンス(MDR)、その他MSPやMSSP向けにカスタマイズ型マネージドサービスなど、ソニックウォールのポートフォリオを拡大します。

- クラウドマネージドサービス産業では、IT・通信セグメントが大きなシェアを占めています。2023会計年度、米国連邦政府は連邦政府の主要なIT投資に約244億米ドルを割り当てました。クラウドマネージドサービスは、IT運用の合理化、セキュリティの強化、拡大可能なソリューションの提供を可能にすることから米国で支持を集めており、安定した市場成長率を反映しています。

- これらのサービスは、クラウドインフラの遠隔管理と保守を容易にするため、企業は外部の専門知識を活用しながら中核目標に集中することができ、産業の成長を促進します。クラウドの導入が急増し、デジタル領域におけるイノベーションと効率性が促進されるにつれて、マネージドサービスの需要は増加するとみられます。

ITと電気通信が最大のエンドユーザー業種に

- 米国の通信産業は、マネージドセキュリティサービスに対する需要が旺盛で、産業の主要動向の1つとして認識されています。これは主に、通信会社が顧客情報やネットワークインフラの詳細など、膨大な量の機密データを扱っているため、サイバー攻撃の格好の標的になっているためです。さらに、通信ネットワークの複雑さとサイバー脅威の進化により、効果的な保護のためには専門的な知識が必要となります。

- 5Gネットワークの登場により、エンドユーザーのセキュリティと質の高い体験を確保することに焦点が移っており、この変化は通信管理サービスの産業概要で強調されています。VIAVISIONによると、2023年4月現在、5Gネットワークへのアクセスは米国の503都市で利用可能であり、これは世界のどの国よりも多く、従来の技術中心のアプローチから脱却し、ネットワークの管理と最適化に大きな転換が求められています。その結果、この移行を支援する通信管理サービスへの需要が高まり、市場成長に寄与しています。

- 2023年7月、マネージドIT、サイバーセキュリティ、クラウドソリューションの大手プロバイダであるデータプライズは、テキサス州を拠点とするセキュリティマネージドサービスプロバイダのレベルセックを買収しました。この買収により、データプライズの全国的なプレゼンスが拡大し、産業による専門性が強化されるとともに、RevelSecの顧客はデータプライズの幅広いサービスを利用できるようになりました。

- 市場レポートによると、先進的ネットワークインフラを必要とするIoT、AI、エッジコンピューティングなどの技術革新により、マネージドインフラは大きな市場シェアを占めています。マネージドサービスは、これらの技術の採用を促進する上で重要な役割を果たしています。

米国(米国)のマネージドサービス産業概要

米国のマネージドサービス市場概要はセグメント化されており、Fujitsu、Cisco Systems Inc.、IBM Corporation、AT&T Inc.、HP Inc.など、市場で強力な顧客基盤を持つ最大手企業によって支配されています。これらの企業は常に、より充実したサービスを提供しています。各社は市場で生き残り、顧客を維持するために強力な競争戦略を採用しているため、市場間の敵対関係が激化しています。

- 2024年2月-UbiquityはFujitsuと提携し、ラストワンマイルのデジタルインフラレジリエンスを強化します。UbiquityはFujitsuのネットワークオペレーションセンターを活用し、米国の4つの主要市場におけるラストマイル・ファイバー・ブロードバンドインフラをサポートします。Fujitsuは、テキサス州にあるキャリアクラスのNOCから24時間365日のマネージドネットワークサービスをUbiquityに記載しています。

- 2024年1月-Ciscoは、データストレージ、インフラ、ハイブリッドクラウド管理を専門とするHitachiの子会社、Hitachi Vantaraと共同で、次世代ハイブリッドクラウドマネージドサービスを発表。これらのサービスは、現代の企業が直面する持続的なデータ管理の課題に取り組むために特別に調整されたものです。Hitachi EverFlex with Cisco Powered Hybrid Cloudとして知られるこの共同ソリューションは、自動化ソリューションと予測分析を組み合わせたものです。Hitachi EverFlex with Cisco Powered Hybrid Cloudは、自動化ソリューションと予測分析を組み合わせたソリューションであり、合理的なインフラ管理、コスト最適化、運用効率向上のための将来を見据えたツールキットを企業に提供することを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- COVID-19の産業への影響評価

第5章 市場力学

- 市場の促進要因

- ハイブリッドITへのシフトの増加

- コストと業務効率の改善

- 市場課題

- 統合と規制の問題、信頼性への懸念

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- タイプ別

- マネージドデータセンター

- マネージドセキュリティ

- マネージドコミュニケーション

- マネージドネットワーク

- マネージドインフラ

- マネージドモビリティ

- 企業規模別

- 中小企業

- 大企業

- 産業別

- BFSI

- IT・通信

- 医療

- エンターテイメントメディア

- 小売

- 製造業

- 政府機関

- その他のエンドユーザー産業別

第7章 競合情勢

- 企業プロファイル

- Fujitsu Limited

- Cisco Systems Inc.

- IBM Corporation

- AT& T Inc.

- HP Inc.

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Rackspace Technology Inc.

- Tata Consultancy Services Limited

- Citrix Systems Inc.

- Wipro Limited

第8章 投資分析

第9章 市場の将来

目次

The United States Managed Services Industry is expected to grow from USD 69.55 billion in 2025 to USD 116.25 billion by 2030, at a CAGR of 10.82% during the forecast period (2025-2030).

Key Highlights

- Managed services comprise outsourcing specific IT functions or processes to third-party providers, aiming to streamline operations and reduce costs. This approach enhances service quality, operational efficiency, and customer satisfaction while lowering expenses.

- Market research indicates that the soaring number of Internet of Things (IoT) devices has heightened the demand for managed IoT services, emphasizing the need to secure, monitor, and optimize these connected devices. In response, IT infrastructure providers are collaborating on IoT solutions.

- Hybrid IT combines on-premise infrastructure with cloud-based solutions. The rise of the Internet of Things (IoT) has prompted organizations to rethink their customer engagement strategies. Managed service providers (MSPs) play a crucial role in bolstering security within the IoT ecosystem, ensuring robust protection.

- Relatively speaking, managed services are known to be cost-effective and efficient, as compared to in-house services in the US, as they enable organizations to focus on their core competencies while outsourcing the non-core areas.In the US managed services market outlook, the integration of diverse technologies and adherence to industry regulations often pose challenges. Companies must navigate a web of standards and legal requirements, impacting the implementation and operation of managed services.

- The initial days of the COVID-19 pandemic and subsequent lockdowns caused a temporary dip in demand as businesses focused on survival and delayed non-essential investments. This led to a delay in implementing managed services contracts. However, the surge in remote work highlighted the need for security, cloud migration, collaboration tools, and networking, creating opportunities for industry growth among Managed Service Providers (MSPs).

United States (US) Managed Services Industry Trends

Cloud to Witness Significant Market Growth

- Cloud-based managed services offer flexibility and scalability, empowering service providers to remotely access, monitor, and resolve issues within the cloud environment. Furthermore, market data shows that the adoption of technologies like AI/ML, big data analytics, threat intelligence, and advanced automation platforms is propelling this transition to cloud-based services. Market players are launching innovative and collaborative services in response to industry trends.

- For example, in November 2023, SonicWall, a global cybersecurity provider, acquired Solutions Granted Inc. (SGI), a Managed Security Service Provider (MSSP) catering to hundreds of Managed Service Providers (MSPs). This acquisition bolsters SonicWall's commitment to its partners. It expands its portfolio to include US-based Security Operations Center services (SOCaaS), Managed Detection and Response (MDR), and other tailored managed services for MSPs and MSSPs.

- The IT and Telecom sector holds a significant market share in the cloud-managed services industry. For the 2023 fiscal year, the US federal government allocated around USD 24.4 billion for major federal IT investments, where cloud-managed services are gaining traction in the United States due to their ability to streamline IT operations, bolster security, and offer scalable solutions, thereby reflecting a steady market growth rate.

- These services facilitate remote management and maintenance of cloud infrastructure, which enables businesses to focus on their core objectives while leveraging external expertise, thereby fostering industry growth. The demand for managed services is set to rise as cloud adoption continues to surge, fostering innovation and efficiency in the digital realm.

IT and Telecom to be the Largest End-user Vertical

- The telecom industry in the United States has a strong demand for managed security services and is identified as one of the major significant industry trends. This is primarily due to the telecom companies' handling of vast volumes of sensitive data, including customer information and network infrastructure details, making them prime targets for cyberattacks. Additionally, the complexity of telecom networks and the evolving nature of cyber threats necessitate specialized expertise for effective protection.

- With the advent of 5G networks, the focus has shifted to ensuring end users' security and quality experiences, a shift highlighted in the industry overview of telecom-managed services. According to VIAVISION, as of April 2023, 5G network access was available in 503 United States cities, the most of any country globally, and this requires a significant shift in managing and optimizing networks, moving away from the traditional technology-centric approach. As a result, there is a rising demand for telecom-managed services to aid in this transition, contributing to market growth.

- In July 2023, Dataprise, a leading provider of managed IT, cybersecurity, and cloud solutions, acquired RevelSec, a Texas-based security managed service provider. This acquisition expands Dataprise's national presence and enhances its vertical expertise while providing RevelSec clients access to a broader range of services from Dataprise.

- According to the market report, managed infrastructure holds a significant market share, driven by innovations like IoT, AI, and edge computing, which necessitate advanced network infrastructure. Managed services play an important role in facilitating the adoption of these technologies.

United States (US) Managed Services Industry Overview

The United States managed services market overview is fragmented and is dominated by largest companies, such as Fujitsu Limited, Cisco Systems Inc., IBM Corporation, AT&T Inc., and HP Inc., among other companies that have a strong client base in the market. These players are constantly providing increased and enhanced offerings. Companies are employing powerful competitive strategies in order to survive in the market and retain their clients, thereby intensifying competitive rivalry in the market.

- February 2024 - Ubiquity partnered with Fujitsu to augment Last-Mile Digital Infrastructure Resilience. Ubiquity would utilize the Fujitsu Network Operations Center to support last-mile fiber broadband infrastructure in four major US markets. Fujitsu delivers Ubiquity with 24x7 managed network services from their carrier-class NOC in Texas.

- January 2024 - Cisco, in collaboration with Hitachi Vantara, the subsidiary of Hitachi Ltd specializing in data storage, infrastructure, and hybrid cloud management, unveiled Next-Gen hybrid cloud managed services. These services are specifically tailored to tackle the persistent data management hurdles faced by contemporary businesses. The joint solution, known as Hitachi EverFlex with Cisco Powered Hybrid Cloud, combines automation solutions and predictive analytics. It aims to equip organizations with a forward-looking toolkit for streamlined infrastructure management, cost optimization, and enhanced operational efficiency.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Limited

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Inc.

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Rackspace Technology Inc.

- 7.1.10 Tata Consultancy Services Limited

- 7.1.11 Citrix Systems Inc.

- 7.1.12 Wipro Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日