|

市場調査レポート

商品コード

1690725

北米の産業用電池:市場シェア分析、産業動向、成長予測(2025~2030年)North America Industrial Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の産業用電池:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

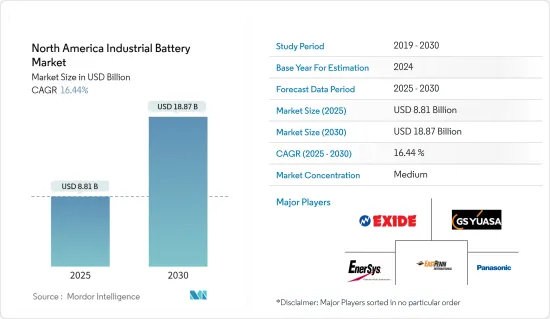

北米の産業用電池の市場規模は2025年に88億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは16.44%で、2030年には188億7,000万米ドルに達すると予測されます。

主なハイライト

- 長期的には、リチウムイオン電池価格の下落、データセンター、地域通信産業からの需要増加、再生可能エネルギー統合の高まりなどが市場を牽引する主な要因となっています。

- 一方、現地生産に必要な原材料の埋蔵量が不足していることなどが、予測期間中の市場成長率を抑制する要因となっています。

- とはいえ、技術的に先進的な電池への注目の高まりや、電池製造の研究開発段階における人工知能の利用の増加は、電池企業が画期的な電池技術を作るために投資し、資源を振り向ける大きな機会を生み出す可能性が高いです。

- 米国は、再生可能電力インフラと工業生産の拡大により、予測期間中に北米の産業用電池市場を独占すると予想されます。

北米の産業用電池市場動向

リチウムイオン電池(LIB)技術が最も急成長する市場セグメントと予測

- さまざまなタイプの産業用電池技術の中で、リチウムイオン電池(LIB)タイプは、主にその有利な容量対重量比により、予測期間中に北米の産業用電池市場で大きな成長が見込まれています。LIBの採用を後押しするその他の要因としては、性能の向上、エネルギー密度の向上、価格の低下といった特性が挙げられます。

- 世界のリチウムイオン電池メーカーは、リチウムイオン電池のコスト削減に注力しています。リチウムイオン電池の価格は過去10年間で急落しました。2023年には、平均的なリチウムイオン電池の価格は1kWhあたり約139米ドルと評価され、2013年と比較して82%以上低下しました。リチウムイオン電池価格の下落は、産業用電池メーカーが電子機器、小型・大型家電、UPS、電気エネルギー貯蔵システムの生産をより安価に動員することを促すと思われます。

- 米国政府は2023年11月、リチウムイオンなどの先進電池の国内生産を促進するため、インフラ法の範囲内で35億米ドルの資金提供を発表しました。アメリカへの投資アジェンダの一環として、政府の資金援助は今後数年間、リチウムイオン電池とパックの製造能力を助けると期待されています。

- さらに、米国ではここ数年、リチウムイオンギガファクトリーの開発が進んでいます。2024年2月、EnerSysはグリーンビルのオーガスタ・グローブ・ビジネス・パークでの平方フィートのリチウムイオン電池製造装置の開発に言及しました。EnerSysは2027年までに、米国の産業・防衛用途の需要に応えるため、リチウムイオン電池セルの製造を開始する予定です。

- さまざまな産業でリチウムイオン電池の利用が急増しているため、制御不能な自己発熱や爆発の可能性を排除する上で、その安全性は非常に重要です。しかし、高品質のリチウムイオン電池の場合、そのような事象はまれであるが、安全点検を行うことが決定的に重要になります。

- 2024年2月、カナダ国立研究会議(NRC)は、リチウムイオン電池モジュールまたはパックの単セル熱暴走故障を評価する試験技術の開発を発表しました。熱暴走開始メカニズム(またはTRIM)装置として知られる特許機構は、リチウムイオン電池の設計や部品の試験に使用できます。これは、関係規制当局が電池使用者のための安全ガイドラインを策定する際に大いに役立ちます。

- したがって、上記の要因に基づいて、リチウムイオン電池技術は大きな需要を示し、予測期間中に北米の産業用電池市場で最も急成長しているセグメントになると予想されます。

米国が市場を独占すると予測

- 米国は、バッテリーを利用したエネルギー貯蔵プロジェクトの急増、再生可能電力インフラの拡大、強固な産業インフラにより、産業用バッテリーの世界の主要ホットスポットの1つです。さらに、米国におけるエネルギー貯蔵システム(ESS)の展開を支援する有利な政策が、今後数年間にわたって産業用電池市場を牽引する可能性が高いです。

- 米国のバッテリーエネルギー貯蔵システム(BESS)産業は、国内の再生可能エネルギーインフラへの投資増加に支えられ、ここ数年顕著な成長を遂げています。過去数年間、再生可能エネルギーの設備容量と発電量は世界的に着実に増加しており、米国は世界の再生可能エネルギーのホットスポットの1つです。

- エネルギー情報局(EIA)によると、2023年、米国は6.4ギガワットの蓄電池を大幅に増設し、電気容量を増強しました。この拡大は、再生可能エネルギー・インフラを強化し、化石燃料への依存を減らすという同国のコミットメントを強調するものでした。

- 国際再生可能エネルギー機関(IRENA)によると、2013年から23年の間に、再生可能エネルギーの設備容量は2倍以上に増加し、2023年の時点で、米国の再生可能エネルギーの設備容量は合計で約387.54GWに達しています。

- 米国エネルギー情報局によると、米国の公益事業規模の蓄電池容量はほぼ倍増すると予想され、開発業者は2023年に1550万kWに1430万kWを追加する計画です。2023年には、米国の送電網に新たに6.4GWの蓄電池容量が追加され、年間70%の増加を記録しました。テキサスは640万kW、カリフォルニアは520万kWで、新規容量の82%を占めると予想されます。

- さらに、2022年から2025年にかけて開発業者によって設置が計画されているユーティリティ規模のバッテリー容量2,080万kWの75%は、テキサス州(790万kW)とカリフォルニア州(760万kW)にあります。

- 米国では、カリフォルニア州独立系統運用機関(CAISO)とテキサス州電力信頼性評議会(ERCOT)が最も大規模な蓄電池容量を追加しています。過去12ヶ月の間に、CAISOにおける太陽光発電容量に占める蓄電池容量の割合は大幅に増加し、2023年1月の29%から2023年12月には41%まで上昇しました。

- さらに政府は、米国におけるBESS産業を強固なものにするため、国際的な連携も積極的に確保しています。例えば、2023年12月、欧州委員会は、オーストラリア、米国、カナダの各国政府とともに、低排出電力への世界的移行における蓄電池推進のための新たなイニシアティブを支援しました。

- COP28国連気候会議の中で発表されたこのイニシアティブは、「電池貯蔵の過充電イニシアチブ」と呼ばれ、多数の国のエネルギー省がメンバーとして参加するクリーンエネルギー閣僚会議に端を発するものです。このような二国間のクリーンエネルギー活動は、米国がバッテリーエネルギー貯蔵システムの強固な市場を開拓するのに役立つと期待されています。

- したがって、上記の要因から、予測期間中、米国が北米の産業用電池市場を独占すると予想されます。

北米の産業用電池産業の概要

北米の産業用電池市場は半分断されています。主なプレーヤー(順不同)には、Exide Industries Ltd、GS Yuasa Corporation、East Penn Manufacturing Company Inc.、Panasonic Holding Corporation、EnerSysなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 2029年までの主要技術タイプ別電池価格動向と予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- リチウムイオン電池のコスト低下

- 抑制要因

- 現地生産に必要な原材料の不足

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 技術分野

- リチウムイオン電池

- 鉛蓄電池

- その他の技術(ニッケルカドミウム電池、ニッケル水素電池、亜鉛カーボンなど)

- 用途

- フォークリフト

- テレコム

- UPS

- その他の用途

- 地域

- 米国

- カナダ

- その他北米地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- C&D Technologies Pvt. Ltd

- East Penn Manufacturing Company Inc.

- EnerSys

- Exide Industries Ltd

- GS Yuasa Corporation

- Leoch International Technology Limited Inc.

- Panasonic Holding Corporation

- Saft Groupe SA

- List of Other Prominent Companies(Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 市場ランキング分析

第7章 市場機会と今後の動向

目次

Product Code: 71172

The North America Industrial Battery Market size is estimated at USD 8.81 billion in 2025, and is expected to reach USD 18.87 billion by 2030, at a CAGR of 16.44% during the forecast period (2025-2030).

Key Highlights

- Over the long term, declining lithium-ion battery prices, increasing demand from data centers, regional telecom industries, and rising renewable energy integration are some major factors driving the market.

- On the other hand, factors such as the lack of prominent raw material reserves required for local production are likely to curtail the market's growth rate during the forecast period.

- Nevertheless, the rising focus on technologically advanced batteries and the growing use of artificial intelligence in the R&D phase of battery manufacturing are likely to create massive opportunities for battery companies to invest and redirect their resources to make breakthrough battery technologies.

- The United States is expected to dominate the North American industrial batteries market during the forecast period, owing to the country's expansion in renewable power infrastructure and industrial production.

North America Industrial Battery Market Trends

Lithium-ion Battery (LIB) Technology Projected to be the Fastest-growing Market Segment

- Among the different types of industrial battery technologies, the lithium-ion battery (LIB) type is expected to witness significant growth in the North American industrial batteries market over the forecast period, majorly due to its favorable capacity-to-weight ratio. Other factors boosting LIB adoption include properties like better performance, higher energy density, and decreasing price.

- Global lithium-ion battery manufacturers are focusing on reducing the cost of lithium-ion batteries. The price of lithium-ion batteries declined steeply over the past ten years. In 2023, the price of an average lithium-ion battery was valued at around USD 139 per kWh, having witnessed a decrease of more than 82% in the price compared to 2013. The decline in lithium-ion battery prices will encourage industrial battery manufacturers to mobilize the production of electronics, small and large appliances, UPS, and electrical energy storage systems at cheaper rates.

- In November 2023, the US government announced a funding of USD 3.5 billion under the ambit of its Infrastructure Law to expedite indigenous production of advanced batteries such as lithium-ion in the country. As a part of the Invest in America Agenda, government funding is expected to help lithium-ion cell and pack manufacturing capabilities over the coming years.

- Further, the United States has been witnessing the development of lithium-ion gigafactories in recent years. In February 2024, EnerSys noted the development of a square-foot lithium-ion battery manufacturing unit at the Augusta Grove Business Park in Greenville. By 2027, EnerSys plans to start manufacturing lithium-ion battery cells to cater to the demand for industrial and defense applications in the United States.

- Owing to the surge in the utilization of lithium-ion batteries across various industries, their safety is of immense importance in eliminating the possibility of uncontrolled self-heating instances and explosions. Such events are, however, rare for high-quality lithium-ion batteries, but it becomes critically important to hold safety checks.

- In February 2024, the National Research Council of Canada (NRC) announced the development of a testing technique to assess the single-cell thermal runaway failure of lithium-ion battery modules or packs. The patented mechanism known as the Thermal Runaway Initiation Mechanism (or TRIM) device can be used to test the design and components of lithium-ion batteries. This can significantly help the concerned regulators devise safety guidelines for battery users.

- Therefore, based on the abovementioned factors, lithium-ion battery technology is expected to witness significant demand and be the fastest-growing segment of the North American industrial batteries market during the forecast period.

United States Projected to Dominate the Market

- The United States is one of the major hotspots for industrial batteries worldwide on account of the surging deployment of battery-based energy storage projects, expansion in renewable power infrastructure, and a robust industrial infrastructure. Moreover, favorable policies backing the deployment of energy storage systems (ESS) in the United States are likely to drive the industrial batteries market over the coming years.

- The US battery energy storage systems (BESS) industry has been experiencing notable growth over the past few years, supported by rising investments in renewable energy infrastructure in the country. Over the past few years, the installed renewable energy capacity and generation have been rising steadily globally, and the United States is one of the global renewable energy hotspots.

- In 2023, according to the Energy Information Administration (EIA), the United States augmented its electric capacity with a significant addition of 6.4 gigawatts in battery storage, marking a notable 2.2 gigawatt increase over the previous year. This expansion underscored the country's commitment to enhancing its renewable energy infrastructure and reducing reliance on fossil fuels.

- According to the International Renewable Energy Agency (IRENA), during 2013-23, installed renewable energy capacity grew by more than two times, and as of 2023, the total installed renewable capacity stood at around 387.54 GW in the United States.

- According to the US Energy Information Administration, the US utility-scale battery storage capacity was expected to nearly double, with developers planning to add 14.3 GW to the 15.5 GW in 2023. In 2023, 6.4 GW of new battery storage capacity was added to the US grid, marking a 70% annual increase. Texas and California were expected to contribute 82% of the new capacity, with 6.4 GW and 5.2 GW, respectively.

- Moreover, 75% of the 20.8 GW of utility-scale battery capacity planned by developers to be installed from 2022 to 2025 is in Texas (7.9 GW) and California (7.6 GW).

- In the United States, the California Independent System Operator (CAISO) and Electric Reliability Council of Texas (ERCOT) have the most large-scale battery storage capacity additions. Over the past twelve months, battery capacity as a percentage of solar generation capacity in CAISO has significantly increased, climbing from 29% in January 2023 to 41% by December 2023.

- In addition, the government is also proactively assuring international ties to make a robust BESS industry in the United States. For instance, in December 2023, the European Commission, together with the national governments of Australia, the United States, and Canada, supported a new initiative to promote battery storage in the global transition to low-emission electricity.

- This initiative, announced during the COP28 UN Climate Conference, called the 'Supercharging Battery Storage Initiative,' originates from the Clean Energy Ministerial, which includes energy departments from numerous countries as members and participants. Such bilateral clean energy activities are expected to help the United States develop a robust market for battery energy storage systems.

- Therefore, based on the abovementioned factors, the United States is expected to dominate the North American industrial batteries market during the forecast period.

North America Industrial Battery Industry Overview

The North American industrial batteries market is semi-fragmented. Some of the major players (not in any particular order) include Exide Industries Ltd, GS Yuasa Corporation, East Penn Manufacturing Company Inc., Panasonic Holding Corporation, and EnerSys.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, Till 2029

- 4.3 Battery Price Trends and Forecasts, By Major Technology Type, Till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Costs of Lithium-ion Batteries

- 4.6.2 Restraints

- 4.6.2.1 Lack of Prominent Raw Material Reserves Required for Local Production

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-acid Battery

- 5.1.3 Other Technologies (Nickel Cadmium Battery, Nickel Metal Hydride, Zinc Carbon, etc.)

- 5.2 Application

- 5.2.1 Forklift

- 5.2.2 Telecom

- 5.2.3 UPS

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 C&D Technologies Pvt. Ltd

- 6.3.2 East Penn Manufacturing Company Inc.

- 6.3.3 EnerSys

- 6.3.4 Exide Industries Ltd

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Leoch International Technology Limited Inc.

- 6.3.7 Panasonic Holding Corporation

- 6.3.8 Saft Groupe SA

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis