|

市場調査レポート

商品コード

1910890

北米の変圧器市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)North America Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の変圧器市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

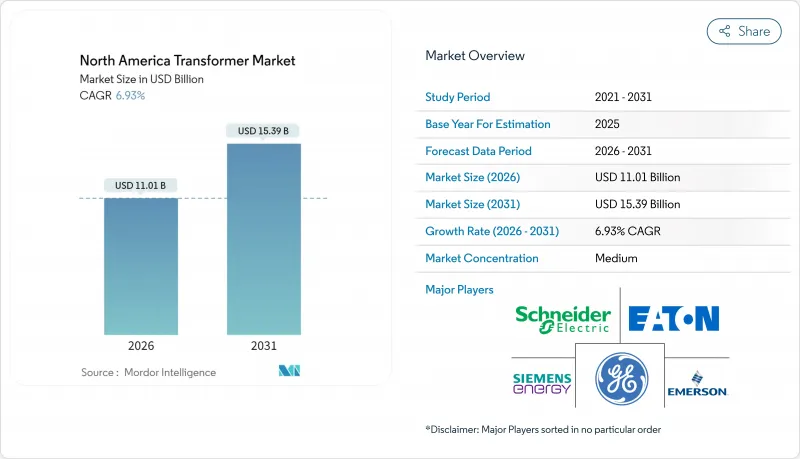

北米の変圧器市場は、2025年に102億9,000万米ドルと評価され、2026年の110億1,000万米ドルから2031年までに153億9,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは6.93%と見込まれています。

送電網近代化の義務化、再生可能エネルギー設備の拡充、老朽化した資産の更新の差し迫った必要性という三つの要因が、あらゆる電圧クラスにおいて受注を拡大する最も明確な原動力となっております。インフラ投資・雇用創出法による650億米ドルの送電網予算配分を中心とした連邦政府の支援は、大容量電力変圧器やデジタル対応監視オプションを重視する新たな電力会社の設備投資の波を生み出しました。バージニア州、テキサス州、オレゴン州におけるハイパースケールデータセンターの数が増加していることで、カスタム昇圧ユニットの需要が高まっております。一方、洋上風力発電の送電計画により、525kV高圧直流変換用変圧器の受注が増加しております。原材料コストの変動性は依然として主要な懸念事項ですが、シーメンス・エナジーや日立エナジーなどの既存メーカーによる現地生産拡大が、リードタイムの短縮、サプライチェーンの回復力向上、北米の変圧器市場の納期遵守に貢献しています。競争上の優位性はソフトウェア主導の資産健全性分析へと移行しており、強力なIoTポートフォリオを有するサプライヤーが調達プロセスで優位に立っています。

北米の変圧器市場の動向と洞察

米国・カナダにおける送電網近代化プログラム

電力会社は現在、中電圧および高電圧の入札案件において、双方向電力フロー機能、オンライン溶解ガス分析、サイバーセキュリティ対策通信を必須仕様として指定しています。米国エネルギー省の2024年度「グリッドレジリエンス・イノベーション・パートナーシップ」では35億米ドルが配分され、ICF社は変圧器健康状態センサーと耐嵐機能の使用を義務付ける2億5,000万米ドルの契約を獲得しました。カナダの電力会社も同様の動きを見せており、BCハイドロはNERC規格EOP-012-2に準拠した寒冷地対応アップグレードに2億米ドルを割り当て、メーカーに対し-40℃での性能検証を義務付けています。レジリエンス目標とスマートグリッド要件の相互作用により、北米の変圧器市場は汎用鉄心製品ではなく、モジュール式でソフトウェアを豊富に備えた設計へと移行しています。統合IoTスタックへの投資を行うメーカーは、新規受注において競合他社を凌駕しています。デジタル対応力は差別化要因ではなく必須条件となり、サプライヤー全体で研究開発予算が増加しています。

再生可能エネルギー拡大に伴う昇圧変圧器の需要

洋上風力発電大手は、3,000MWを超える定格容量の525kV高圧直流変換用変圧器を確定契約中です。2025年に日立エナジーが受注したSunZia連系プロジェクト契約が好例です。これらの特注ユニットは、高調波フィルタリング、故障耐過渡性能、厳格な系統コード同期化を処理しなければならず、これら全ての機能は標準的な配電用変圧器の能力を超えています。供給は世界的に限られた専門メーカーに集中しているため、プレミアム価格が維持されやすい状況です。契約当局は実績あるHVDC技術の実績を優先するため、低コスト参入者が北米の変圧器市場のこの層を混乱させる可能性は低くなっています。予測期間中、新規洋上風力発電プロジェクトの追加ごとに大型電力ユニットの需要が増大し、高電圧機器およびソフトウェア支援型状態監視への移行が加速する見込みです。

分散型エネルギー資源(DER)の浸透率上昇

カリフォルニア州のネット・エネルギー・メータリング制度により、双方向電力フローが従来の降圧変圧器に過負荷を発生させ、電力会社が屋根設置型太陽光発電の出力を抑制せざるを得ない事例が明らかになりました。テキサス州やハワイ州でも同様の傾向が見られ、電力会社の従来型ユニット更新意欲を抑制しています。DERは中規模配電変圧器の総需要を抑制する一方で、スマートな双方向デバイスの導入を促進しており、北米の変圧器市場は衰退ではなく進化を遂げていることを示しています。グリッドエッジ電圧調整機能とリモート更新ファームウェアを備えたベンダーは、販売数量の圧迫を平均販売価格の上昇で相殺する最適な立場にあります。

セグメント分析

100MVAを超える大型変圧器は、電力会社がHVDC連系や洋上風力発電接続プロジェクトを加速させるにつれ、北米の変圧器市場におけるシェア拡大が見込まれます。一方、10MVA以下の小型ユニットは、配電網における圧倒的な設置台数により、2025年の売上高の47.92%を占め続けています。超高圧設計のプレミアムは、世界でもごく少数の工場でしか生産できず、輸送制約が供給をさらに制限しているため、堅調に推移しています。2026年から2031年の期間において、大型ユニットクラスは7.74%のCAGRを記録すると予測されており、これは北米の変圧器市場全体の成長プロファイルを上回るものです。これは、連邦政府のマッチング資金により地域送電網アップグレードの承認期間が短縮されるためです。

電力会社はNERC(北米電力信頼性協議会)のライドスルー要件強化にも直面しており、部分的な出力増強から高定格機器への一括更新へと移行が進んでいます。中電力セグメント(10~100MVA)は産業の電化化により恩恵を受けておりますが、資金配分は注目を集める大規模電力プロジェクトに偏りがちです。大型コアや先進絶縁システムにおける規模の経済が成熟するにつれ、MVA当たりの納入コストは緩やかに低下し、対応可能な需要が拡大すると予想されます。その結果、北米の変圧器市場における大型定格ユニットのシェアは、この10年間を通じて着実な拡大を続ける見込みです。

油浸式設計は2025年時点で67.98%の市場支配率を維持しており、これは主に送電用途における優れた熱余裕度と過負荷耐性が要因です。しかしながら、環境責任への懸念や商業用不動産改修における保守性の高さから、空冷式代替品は7.52%のCAGRでシェアを拡大中です。データセンターでは消火システムの複雑化を最小限に抑えるため乾式変圧器が好まれており、この動向は北米の変圧器市場全体の需要を形成する産業ブームと相まっております。一方、電力会社は慎重な姿勢を維持しており、69kVを超える設備では実績ある誘電体安定性を理由に油浸式をデフォルト仕様とするケースが多く見られます。

規制当局は油漏れ防止と火災リスクに関する規則を強化しており、病院、空港、半導体工場などのセグメントを乾式変圧器の購入へと導いています。メーカーはこれに対応し、鋳造樹脂および強制空冷方式を採用した製品を開発しており、定格容量は25MVAに迫る水準に達し、従来のサイズ制限を解消しつつあります。絶縁システムの技術革新が継続すれば、北米の変圧器市場における乾式変圧器のシェアは2031年までに二桁に達する可能性がありますが、高電圧領域における油入変圧器技術の完全な置き換えは依然として困難と見られます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 米国およびカナダにおける送電網近代化プログラム

- 再生可能エネルギーの拡大に伴う昇圧変圧器の需要増加

- 老朽化した送電インフラの更新

- IIJA(インフラ投資・建設計画)を通じた連邦政府資金及びカナダのグリーンインフラ

- 洋上風力発電用高電圧直流変換器変圧器

- データセンターにおけるオンサイト変電所の電化

- 市場抑制要因

- 分散型エネルギー資源(DER)の普及率上昇

- 銅及び方向性鋼板の価格変動性

- ソリッドステート変圧器の台頭

- 長いリードタイムによる設備投資決定の遅延

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 定格出力別

- 大型(100 MVA以上)

- 中型(10~100 MVA)

- 小型(10MVA以下)

- 冷却方式別

- 空冷式

- 油冷式

- 相別

- 単相

- 三相

- 変圧器タイプ別

- 電力

- 配電

- エンドユーザー別

- 電力会社

- 産業用

- 商業用

- 住宅用

- 地域別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、提携、電力購入契約)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Hitachi Energy

- Siemens Energy

- GE Vernova(Prolec GE)

- Eaton Corp PLC

- Schneider Electric SE

- WEG SA

- Mitsubishi Electric Corp

- Toshiba Corp

- ABB Trafo US(ABB until 2020)

- SPX Transformer Solutions

- Northern Transformer Corp

- Howard Industries

- SGB-SMIT Group

- CG Power & Industrial Solutions

- Royal SMIT Transformers

- ERMCO Inc.

- Pennsylvania Transformer Tech

- Valard Construction(EPC)

- K-Factor Transformers(Hammond Power)

- Delta-Star Inc.