液体廃棄物管理- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Liquid Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690702

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

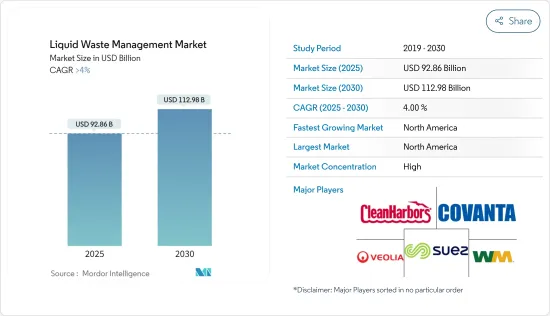

液体廃棄物管理市場規模は2025年に928億6,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは4%を超え、2030年には1,129億8,000万米ドルに達すると予測されます。

主要ハイライト

- COVID-19パンデミックは、石油精製装置が生産量を削減し、封鎖期間中に燃料需要が世界全体で約30%~40%減少したため、市場にマイナスの影響を与えました。しかし、パンデミック中は様々な医薬品の需要が増加したため、廃液の生産が促進されました。現在、市場はパンデミックから回復しています。市場は2022年にはパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

- 有毒化学品を発生させる製造活動の増加は、廃液管理活動を強化すると予想されます。また、製薬・医療産業の成長も市場の成長を促進すると予想されます。

- その反面、技術的課題の増加や厳しい廃棄物処理規制が市場成長の妨げになると予想されます。

- さらに、新たな汚染物質の処理への注目の高まりは、調査された市場に機会を提供すると考えられます。

- 北米地域は最大の市場を占めており、液体廃棄物の管理に関連する厳しい規範の制定や石油・ガス生産に関連する活動の存在により、予測期間中に最も急成長する市場になると予想されています。

液体廃棄物管理市場の動向

石油・ガスセグメントが市場を独占

- 石油・ガス産業は最も収益性の高い産業の一つです。石油・ガス産業は、様々な産業、家庭、輸送、その他の部門におけるあらゆるエネルギー需要を満たしています。石油・ガス産業は、主に廃水に関する環境問題に直面しています。

- 製油所では、原油をガソリン、ディーゼル、ジェット燃料、灯油などのさまざまな留分に蒸留するため、水の消費率が非常に高いです。製油所から排出される廃水には、上澄み前の原油を洗浄する際に発生する脱塩水、スチームストリッピングや原油と接触する分留から発生するサワー水、製品の洗浄、触媒の再生、脱水素反応から発生するプロセス水などがあります。

- さらに、石油・ガス産業は、パイプラインの安全性を確保し、漏れの可能性を発見するためのパイプラインの静水圧検査で消費される静水圧検査水など、様々な作業で大量の廃水を発生させるため、水の消費率が高いです。このプロセスには、化学添加物の使用も含まれます。したがって、水圧検査水は、海や地表水に廃棄される前に処理されなければならないです。

- さらに石油・ガス産業では、水圧破砕のような技術に水が使用されます。このプロセスでは、高圧の水を使用して岩石のタイトな地層に亀裂や割れ目を開け、石油ガスや未精製の石油を坑井に流して回収します。このプロセスで使用される水はしばしば汚染され、廃棄または再利用のために処理される必要があります。

- BP Statistical Review of World Energy 2022によると、2022年の世界の石油生産量は日量9,390万バレルで、前年比4%増です。

- さらに、中国は原油処理活動を増加させており、これは同国内で今後予定されているさまざまな製油所によって支えられています。例えば、2023年3月、Saudi Aramcoと中国のパートナーは、燃料と石油化学製品に対する同国の需要増加に対応するため、2026年に中国北東部で100億米ドルを投じて製油所と石油化学プロジェクトを開始する予定です。

- したがって、上記の要因は今後数年間、市場に大きな影響を与えると予想されます。

市場を独占する北米

- 北米は最大の市場であり、厳しい規制の制定や石油・ガス生産に関連する活動の存在により、期間中最も急成長する市場であると予想されます。

- 米国エネルギー情報局(EIA)によると、米国の原油生産量は2022年12月の年間1,211万5,000バレルに対し、2023年1月には1,246万2,000バレルに達しました。

- さらにEIAは、米国の原油生産量は2023年に平均1,240万バレル/日、2024年には1,280万バレル/日になると予測しています。米国は、非在来型原油埋蔵量の探査において世界有数の国であり、同国の調査市場にとって大きな機会であることを示しています。

- 自動車産業から排出される廃液には、使用済みモーターオイルや使用済みブレーキオイル液などがあります。OICAによると、2022年には米国で約1,006万339台の自動車が生産され、前年比約10%の成長率を示しています。

- さらに、液体廃棄物管理市場は、環境保護庁(EPA)や化学品の登録・評価・認可・制限(REACH)のような機関による規制が非常に厳しいです。1993年の環境保護法を含むいくつかの法律では、環境影響評価(EIA)の実施や環境影響評価書(EIS)の作成など、企業が実施すべきガイドラインについて言及しています。

- したがって、前述の要因は今後数年間、市場に大きな影響を与えると予想されます。

液体廃棄物管理産業概要

液体廃棄物管理市場は統合された性質を持っています。調査対象市場の主要企業(順不同)には、SUEZ、Veolia、CLEAN HARBORS, INC.、Covanta Holding Corporation、WM Intellectual Property Holdings, L.L.C.などが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 医薬品・医療産業の成長

- 有害化学品を含む製造活動の増加による廃液管理の拡大

- その他の促進要因

- 抑制要因

- 技術的課題の増加

- 厳しい廃棄物処理規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 発生源別

- 住宅

- 商業

- 産業

- サービス

- コレクション

- 輸送/運搬

- 廃棄/リサイクル

- エンドユーザー産業

- 自動車

- 鉄鋼

- 石油・ガス

- 製薬

- 繊維

- その他のエンドユーザー産業(紙パルプ、飲食品など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- CLEAN HARBORS, INC.

- Cleanaway

- Covanta Holding Corporation

- Enva

- GFL Environmental Inc.

- Hulsey(a Blue Flow Company)

- Ovivo

- REMONDIS SE & Co. KG

- SUEZ

- Veolia

- WM Intellectual Property Holdings, L.L.C.

第7章 市場機会と今後の動向

- 世界の水危機の高まりが、液体廃棄物管理に新たな機会を生み出す

- 新興汚染物質処理への注目の高まり

目次

Product Code: 71005

The Liquid Waste Management Market size is estimated at USD 92.86 billion in 2025, and is expected to reach USD 112.98 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic negatively impacted the market as petroleum refinery units cut their production throughput, and the demand for fuel decreased by about 30% to 40% globally during the lockdown. However, the demand for various pharmaceutical products increased during the pandemic, thereby enhancing the production of liquid wastes. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The increasing manufacturing activities that generate toxic chemicals are anticipated to enhance liquid effluent management activities. Also, the growth in the pharmaceutical and healthcare industry is expected to drive the market's growth.

- On the flip side, increasing technological challenges and stringent waste processing regulations are expected to hinder the market's growth.

- Further, the increasing focus on treating emerging contaminates is likely to provide opportunities to the market studied.

- The North American region represents the largest market, and it is also expected to be the fastest-growing market over the forecast period due to the enactment of stringent norms pertaining to the management of liquid waste and the presence of activities related to oil and gas production.

Liquid Waste Management Market Trends

Oil and Gas Segment to Dominate the Market

- The oil and gas industry is among the most profitable industries. It meets all the energy demands across various industries, households, transportation, and other sectors. The oil and gas industry is facing environmental concerns, mainly with wastewater.

- In refineries, the water consumption rate is very high for distilling crude into various fractions, such as gasoline, diesel, jet fuel, and kerosene. Several wastewater streams are coming out of refineries, which typically include desalter water generated from washing raw crude before topping, sour water from steam stripping, and fractionating that comes in contact with crude, process water generated from product washing, regenerating catalyst, and dehydrogenation reactions.

- Further, the oil and gas industry has a high water consumption rate, as it generates a large amount of wastewater in various operations, such as in hydrostatic testing water, which is consumed in the hydrostatic testing of pipelines to ensure pipeline safety and find any possible leaks. The process also includes the usage of chemical additives. Hence, hydro-test water should be treated before disposal into the sea or surface water.

- Furthermore, in the oil and gas industry, water is employed in technologies like hydraulic fracturing. In this process, high-pressure water is used to open up the cracks or fractures into the tight formations of rocks, permitting petroleum gas and unrefined petroleum to stream to a well for recovery. The water used in the process often gets contaminated, and it needs to be treated for either disposing of or reuse.

- According to the BP Statistical Review of World Energy 2022, global oil production amounted to 93.9 million barrels per day in 2022, representing an increase of 4% compared to the previous year.

- Further, China is increasing crude oil processing activities, which will be supported by following various upcoming refineries in the country. For instance, in March 2023, Saudi Aramco and its Chinese partners plan to start a full 10 USD billion refinery and petrochemical project in northeast China in 2026 to meet the country's growing demand for fuel and petrochemicals.

- Therefore, the factors above are expected to show a significant impact on the market in the coming years.

North America to Dominate the Market

- North America represents the largest market, and it is also expected to be the fastest-growing market over the period due to the enactment of stringent norms and the presence of activities related to oil and gas production.

- According to the US Energy Information Administration (EIA), crude oil production in the United States reached 12,462 thousand barrels in January 2023, compared to 12,115 thousand barrels annually in December 2022.

- Further, EIA forecasted that crude oil production in the United States will average 12.4 million barrels per day (b/d) in 2023 and 12.8 million b/d in 2024. The United States is one of the leading countries globally in terms of exploration of unconventional crude oil reserves, indicating a huge opportunity for the studied market in the country.

- Some of the liquid waste produced by the automotive industry includes used motor oil and used brake oil fluid. According to OICA, in 2022, around 10,060,339 vehicles were produced in the United States, witnessing an increasing growth rate of about 10% compared to the previous year.

- Moreover, the liquid waste management market is very well regulated by agencies like the Environmental Protection Agency (EPA) and the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH). Several laws, including the Environmental Protection Act of 1993, mentioned guidelines to be carried out by companies, including undertaking Environmental Impact Assessment (EIA) and preparing Environmental Impact Statement (EIS).

- Therefore, the aforementioned factors are expected to impact the market in the coming years significantly.

Liquid Waste Management Industry Overview

The liquid waste management market is consolidated in nature. The major players in the studied market (not in any particular order) include SUEZ, Veolia, CLEAN HARBORS, INC., Covanta Holding Corporation, and WM Intellectual Property Holdings, L.L.C., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in the Pharmaceutical and Healthcare Industry

- 4.1.2 Increased Manufacturing Activities Containing Toxic Chemicals Leading to Growing Liquid Effluent Management

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Technological Challenges

- 4.2.2 Stringent Waste Processing Regulations

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Source

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial

- 5.2 Service

- 5.2.1 Collection

- 5.2.2 Transportation/Hauling

- 5.2.3 Disposal/Recycling

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Iron and Steel

- 5.3.3 Oil and Gas

- 5.3.4 Pharmaceutical

- 5.3.5 Textile

- 5.3.6 Other End-user Industries (Pulp and Paper, Food and Beverages, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 CLEAN HARBORS, INC.

- 6.4.2 Cleanaway

- 6.4.3 Covanta Holding Corporation

- 6.4.4 Enva

- 6.4.5 GFL Environmental Inc.

- 6.4.6 Hulsey (a Blue Flow Company)

- 6.4.7 Ovivo

- 6.4.8 REMONDIS SE & Co. KG

- 6.4.9 SUEZ

- 6.4.10 Veolia

- 6.4.11 WM Intellectual Property Holdings, L.L.C.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Rising Water Crisis Globally is Creating New Opportunities for Liquid Waste Management

- 7.2 Increasing Focus on Treating Emerging Contaminates

液体廃棄物管理- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日