|

市場調査レポート

商品コード

1690694

欧州の医薬品ロジスティクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の医薬品ロジスティクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

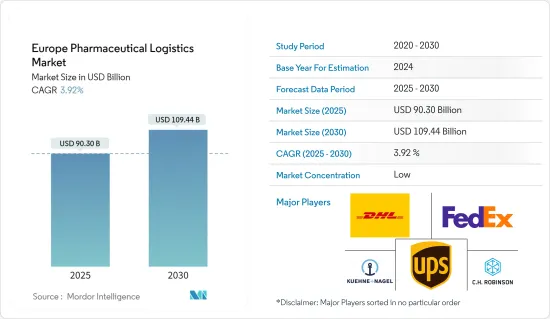

欧州の医薬品ロジスティクス市場規模は2025年に903億米ドルと推定され、予測期間(2025~2030年)のCAGRは3.92%で、2030年には1,094億4,000万米ドルに達すると予測されます。

欧州における医薬品ロジスティクスの需要は、COVID-19の大流行と大手製薬企業による投資の増加に煽られた医薬品とワクチンの需要増が主因となっています。欧州の経済成長を回復させ、競争が激化する世界経済において継続的な競合を確保するために、研究開発医薬品部門は重要な役割を果たしています。欧州は2022年に研究開発に445億ユーロ(484億3,400万米ドル)を投資しました。また、上流から下流まで、約86万5,000人を直接雇用し、間接的に現在の約3倍の雇用を生み出しています。

製薬産業における細胞療法、ワクチン、血液製剤の需要の増加が、この地域の医薬品ロジスティクス市場の成長を牽引しています。医薬品セグメントにおけるリバースロジスティクス需要の増加、温度に敏感な医薬品需要の増加、医薬品ロジスティクスにおけるRFID技術の利用の増加は、欧州の医薬品ロジスティクス市場における今後の動向です。

医薬品販売の増加は医療ロジスティクス市場の成長を促進すると予想されます。医薬品は薬局やドラッグストアなどに保管・輸送されるため、輸送や医療ロジスティクスの需要が高まります。

欧州の医薬品ロジスティクス市場動向

欧州におけるバイオ医薬品販売の増加

欧州は世界第2位のバイオ医薬品市場です。人口の増加と病気の蔓延が市場開拓を後押ししています。受容性と開放性、病気の治療と治療のためのバイオ医薬品へのアクセスのしやすさ、薬剤療法に関連する心遣いが、欧州市場を後押ししています。患者のために地域全体で安全で安価な医薬品を確保し、欧州製薬産業がイノベーターとして世界のリーダーであり続けられるよう支援するため、欧州委員会は欧州の医薬品戦略案に関する公開協議を開始しました。

医薬品メーカーは、製品の品質と感度をますます重視するようになっています。複雑な生物学的ベースの医薬品の開発、ホルモン治療、ワクチン、複雑なタンパク質の出荷などの要因は、特殊な輸送や倉庫を必要とする特定の結果を必要とします。医薬品や医療機器の温度管理物流は、医療物流産業の一部です。さらに、商品の品質を維持するための効果的なコールドチェーン物流サービスに対するニーズの高まりが、医薬品物流市場の成長を後押ししています。

医薬品産業向けのコールドチェーンサプライチェーンとロジスティクスは、より戦略的で信頼性の高いものへと進化しています。高価値の医薬品は主に、流通網全体にわたるコールドチェーンソリューションを通じて出荷されるため、市場の成長を後押ししています。

ドイツからの医薬品輸出が増加

ドイツ貿易投資庁(GTAI)によると、ドイツは欧州最大の医薬品市場であり、世界第4位の規模を誇る。同国は医薬品生産の世界の原動力の1つと考えられており、その豊富な熟練労働力により、製薬会社は良好な製造品質を維持しながら、バイオシミラーなど他の複雑で困難な製品に注力することができます。

2023年のドイツの人口は約8,450万人で、EUで最も人口の多い国となっています。ドイツ市場は、イタリア、フランス、英国市場を上回っています。ドイツの世界の医薬品総配分額は、世界の医薬品産業の5.9%を占めています。ドイツには510社以上の製薬会社と670社以上のバイオテクノロジー企業があります。製造された医薬品と製薬機器は、パンデミック初期には311億ユーロ(331億米ドル)でした。

輸出は2002年の500億ユーロ(535億米ドル)から2022年には2,870億ユーロ(307億米ドル)に増加しました。2021年(2,350億ユーロ)と比較すると、2022年の総額は22%の増加となります。輸入は2002~2022年の間に320億ユーロ(340億米ドル)から1,120億ユーロ(119億米ドル)に増加し、2021年(1,000億ユーロ)から2022年には約12%増加しました。

欧州の医薬品ロジスティクス産業概要

欧州の医薬品ロジスティクス市場は競争が激しくセグメント化されており、地域的・国際的な市場参入企業で構成されています。同市場には、DHL Supply Chain、FedEx、Kuehne+Nagel International AG、United Parcel Service、CH Robinsonなど、既存の大手企業がいくつか存在します。国内の主要企業には、Eurotranspharma、Centre Specialties Pharmaceutiques、PostNL Pharma & Care、Trans-o-Flex Schnell-Lieferdienst GmbHなどがあります。これらの企業は、自動化、人工知能、機械学習(AIやML)、ブロックチェーン、輸送管理システムなどの次世代物流ソリューションをサービスに導入し、サプライチェーンの生産性を高め、コストを削減し、エラーを回避しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 政府の規制と取り組み

- 産業の技術動向

- COVID-19の市場への影響

- バリューチェーン/サプライチェーン分析

第5章 市場力学

- 市場の促進要因

- 欧州における大衆薬の需要拡大

- 製薬会社による製造活動の拡大

- 市場抑制要因

- 注文輸送に伴う高コスト

- 市場機会

- 医療セグメントにおける在宅医療機器と迅速な支援に対する需要の増加

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 製品別

- ジェネリック医薬品

- ブランド医薬品

- オペレーション別

- コールドチェーン輸送

- 非コールドチェーン輸送

- 用途別

- バイオ医薬品

- 化学医薬品

- 輸送別

- 航空

- 鉄道

- 道路

- 海路

- 地域別

- ドイツ

- 英国

- オランダ

- フランス

- イタリア

- スペイン

- ポーランド

- ベルギー

- スウェーデン

- その他の欧州

第7章 競合情勢

- 市場集中度概要

- 企業プロファイル

- DHL

- FedEx

- Kuehne+Nagel International AG

- United Parcel Service

- C.H. Robinson

- CEVA Logistics

- DB Schenker

- Agility Logistics

- Eurotranspharma

- CSP*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

The Europe Pharmaceutical Logistics Market size is estimated at USD 90.30 billion in 2025, and is expected to reach USD 109.44 billion by 2030, at a CAGR of 3.92% during the forecast period (2025-2030).

The demand for pharmaceutical logistics in Europe is mainly driven by the increasing demand for drugs and vaccines, fueled by the COVID-19 pandemic and increasing investments by leading pharmaceutical firms. In order to restore economic growth in Europe and ensure the continued competitiveness of an increasingly competitive world economy, the R&D pharmaceutical sector plays a vital role. Europe invested EUR 44,500 million (USD 48,434 million) in research and development in 2022. It also directly employs about 865,000 people and indirectly generates about three times as many jobs as it now does, upstream and downstream.

Increasing demand for cellular therapies, vaccines, and blood products in the pharmaceutical industry is driving the growth of the region's pharmaceutical logistics market. The increase in demand for reverse logistics in the pharmaceutical sector, the rise in demand for temperature-sensitive pharmaceutical drugs, and the increase in the use of RFID technologies for pharmaceutical logistics are upcoming trends in the European pharmaceutical logistics market.

The growing pharmaceutical sales are expected to propel the growth of the healthcare logistics market. Increasing sales of pharmaceuticals are expected to boost the demand for logistics as the pharmaceutical products or drugs should be stored and transported to pharmacies, drug stores, and others, thus increasing the demand for transportation or healthcare logistics.

Europe Pharmaceutical Logistics Market Trends

Biopharma Sales in Europe is Increasing

Europe is the second-biggest biopharmaceuticals market in the world. The increasing populace and persistent sicknesses are boosting market development. The reception and openness, accessibility of biopharmaceuticals for treating and concluding illnesses, and mindfulness connected with medication have boosted the European market. To ensure the availability of secure and affordable medicines throughout the region for patients and to support the European pharmaceutical industry's ability to remain an innovator and a world leader, the European Commission established a public consultation on its proposed European drug strategy.

Pharmaceutical manufacturers increasingly focus on product quality and sensitivity. Factors such as the development of complex biological-based medicines and shipments of hormone treatments, vaccines, and complex proteins require specific results that require specialized transportation and warehousing. Temperature-controlled logistics of pharmaceutical products and medical devices is a part of the healthcare logistics industry. Moreover, the increase in the need for effective cold-chain logistics services to maintain the quality of goods fuels the growth of the pharmaceutical logistics market.

Cold chain supply chains and logistics for the pharmaceutical industry are evolving to be more strategic and reliable. High-value pharmaceutical products are mainly shipped via cold chain solutions across the entire distribution network, thus driving the market's growth.

Pharmaceutical Exports From Germany Are Increasing

Germany is the largest pharmaceutical market in Europe and the fourth-biggest in the world, as per Germany Trade and Invest (GTAI). The country is considered one of the global driving points for pharmaceutical production, and its large skilled labor force allows pharmaceutical companies to focus on other complex and challenging products, such as biosimilars, while keeping up with good manufacturing quality.

The population of Germany in 2023 was almost 84.5 million inhabitants, making it the most populated country in the European Union. The German market is ahead of the Italian, French, and Great Britain markets. Germany's total global pharmaceutical value allocation accounted for 5.9% of the global pharmaceutical industry. Germany has more than 510 pharmaceutical companies and more than 670 biotech companies. The manufactured medicines and pharma equipment were valued at EUR 31.1 billion (USD 33.1 billion) at the beginning of the pandemic.

Exports increased from EUR 50 billion (USD 53.5 billion) in 2002 to EUR 287 billion (USD 30.7 billion) in 2022. Compared to 2021 (EUR 235 billion), the 2022 total represented an increase of 22%. Imports rose from EUR 32 billion (USD 34 billion) to EUR 112 billion (USD 11.9 billion) between 2002 and 2022, rising by almost 12% from 2021 (EUR 100 billion) to 2022.

Europe Pharmaceutical Logistics Industry Overview

The European pharmaceutical logistics market is highly competitive and fragmented and consists of regional and international market players. A few existing significant players in the market include DHL Supply Chain, FedEx, Kuehne + Nagel International AG, United Parcel Service, and CH Robinson. Some major domestic players include Eurotranspharma, Centre Specialties Pharmaceutiques, PostNL Pharma & Care, and Trans-o-Flex Schnell-Lieferdienst GmbH. These companies are implementing next-generation logistics solutions in their services, such as automation, artificial intelligence, machine learning (AI and ML), blockchain, transportation management systems, and others, to increase supply chain productivity, reduce costs, and avoid errors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends in the Industry

- 4.4 Impact of COVID-19 on the Market

- 4.5 Value Chain / Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Over the Counter Drugs Across the European Region

- 5.1.2 Growing Manufacture Activity from Pharmaceutical Companies

- 5.2 Market Restraints

- 5.2.1 High Cost Associated with the Transportation Ordered

- 5.3 Market Opportunities

- 5.3.1 Increasing Demand for Home Healthcare Devices and Fast Track Assistance in the Healthcare Sector

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Generic Drugs

- 6.1.2 Branded Drugs

- 6.2 By Operation

- 6.2.1 Cold Chain Transport

- 6.2.2 Non-cold Chain Transport

- 6.3 By Application

- 6.3.1 Biopharma

- 6.3.2 Chemical Pharma

- 6.4 By Transportation

- 6.4.1 Airways

- 6.4.2 Railways

- 6.4.3 Roadways

- 6.4.4 Seaways

- 6.5 By Geography

- 6.5.1 Germany

- 6.5.2 United Kingdom

- 6.5.3 The Netherlands

- 6.5.4 France

- 6.5.5 Italy

- 6.5.6 Spain

- 6.5.7 Poland

- 6.5.8 Belgium

- 6.5.9 Sweden

- 6.5.10 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 DHL

- 7.2.2 FedEx

- 7.2.3 Kuehne+Nagel International AG

- 7.2.4 United Parcel Service

- 7.2.5 C.H. Robinson

- 7.2.6 CEVA Logistics

- 7.2.7 DB Schenker

- 7.2.8 Agility Logistics

- 7.2.9 Eurotranspharma

- 7.2.10 CSP*

- 7.3 Other Companies