|

市場調査レポート

商品コード

1910607

医薬品物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医薬品物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

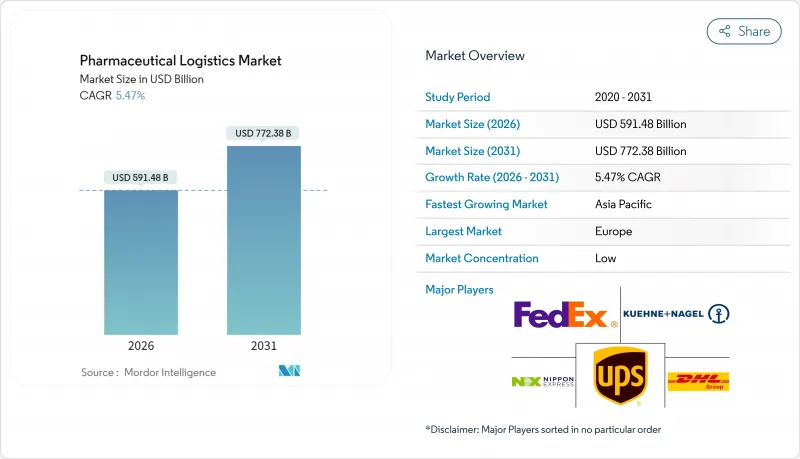

医薬品物流市場は、2025年に5,608億1,000万米ドルと評価され、2026年の5,914億8,000万米ドルから2031年までに7,723億8,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.47%と見込まれます。

堅調な成長は、生物学的製剤の普及、厳格なシリアル化義務、および精密な流通能力を必要とする患者直接配送モデルへの転換に起因しています。世界の統合事業者による強力な設備投資、持続的な電子薬局の導入、温度管理インフラの拡大は、競合を激化させ続ける一方で、エンドツーエンドでコンプライアンスに準拠したサプライチェーンソリューションに対する潜在的な需要を拡大しています。技術導入、特にIoTセンサー、ブロックチェーンによるトレーサビリティ、AI駆動のネットワーク最適化は、利害関係者が温度逸脱や偽造リスクを防止するため加速しています。同時に、排出量削減に向けた持続可能性への取り組みが、輸送手段を複合輸送や海上輸送へ転換させ、専門サービスプロバイダーにとって新たなニッチ市場を開拓しています。コールドチェーンのエネルギーコストや複数管轄区域にわたるコンプライアンスに関連する価格圧力は依然として逆風ではありますが、低炭素包装、地域別在庫管理、代替燃料への投資を促進し、最終的には医薬品物流市場の拡大につながっています。

世界の医薬品物流市場の動向と洞察

オンライン薬局の拡大

現在、消費者のほぼ半数が医薬品のオンライン注文を好んでおり、運送業者には温度管理が重要な製品向けに2℃~8℃の環境を保証する戸口配送ネットワークの構築が求められています。アジア太平洋地域のプロバイダーはデジタル決済と遠隔医療プラットフォームを活用し、常温・冷蔵小包サービスの拡大を図っています。一方、米国の統合事業者はIoT対応の梱包ソリューションによりラストマイルの可視性を高めています。規制当局はこれに対応し、シリアル化と追跡管理を単品レベルまで拡大。コンプライアンスのハードルは高まる一方、リアルタイムの温度・位置データを提供する事業者の差別化も進んでいます。電子薬局の取扱量が増加する中、マイクロフルフィルメントハブに向けたネットワーク再設計によりリードタイムが短縮され、服薬遵守率が向上。医薬品物流市場全体で需要の増加を後押ししています。

OTC医薬品需要の増加と慢性疾患の負担

OTC医薬品は処方薬に比べ取り扱い規則が緩やかであるため、統合型流通業者の保管コスト削減につながる混合輸送ルートが可能となります。しかしながら、糖尿病や心血管疾患の有病率上昇により継続的な補充サイクルが求められ、時間厳守在庫の処理能力要件が強化されています。物流パートナーはロボットによるピッキング・パッキングやスマートブリスター包装などの自動化技術を活用し、OTC医薬品と慢性疾患治療薬を統合フローで組み合わせることで滞留時間を削減しています。ハイブリッドモデルは、医薬品物流市場における資産活用率の向上と収益性の維持を実現すると同時に、薬局や診療所へのサービス品質を向上させます。

温度管理配送の高コスト

コールドチェーンの障害は、医薬品メーカーに年間推定350億米ドルの損失をもたらしています。これは廃棄処理、再包装、罰則付き配送などを反映した金額です。相変化材料を用いたパッシブ包装は保護時間を96時間まで延長可能ですが、小包あたりの費用を倍増させる場合が多く、資金が限られる新興市場向けプログラムに負担をかけています。冗長な監視装置や有資格スタッフの必要性は間接費を増大させ、医薬品物流市場における中小運送業者の利益率を制限しています。低炭素冷媒や再利用可能なトートバッグの革新は輸送コスト削減を目指していますが、初期投資額が障壁となり、広範な導入は依然として制約されています。

セグメント分析

輸送部門は2025年収益の51.40%を占め、物理的移動が医薬品物流市場の基幹であることが示されています。道路貨物輸送は地域間流通、特に欧州と北米を結ぶ流れを担い、航空貨物輸送は翌日配達保証による長距離バイオ医薬品補充を支えています。海運ルートは、排出量削減のためGDP準拠の冷蔵コンテナを活用する荷主が持続可能な選択肢を追求する中で重要性を増しています。

付加価値サービスはCAGR4.42%で拡大しており、ラベル貼付、二次包装、注文キット化、シリアル化コンサルティングなどが含まれ、メーカーの非中核業務負担を軽減します。需要が最も急速に伸びているのはアジア太平洋地域であり、契約製造メーカーは複数言語での規制印刷を処理できる単一ソースのパートナーを求めています。データ完全性に関する規制が強化される中、認証済み再ラベル貼付や改ざん防止包装は、オプションの追加サービスから調達の前提条件へと変化し、医薬品物流市場全体で利益率の向上を促進しています。

地域別分析

欧州は2025年においても31.70%の収益シェアを維持しました。これは、調和されたGDP施行、密な道路網、そしてドイツ、スイス、アイルランドにおける大規模製造クラスターに支えられたものです。国境を越えた鉄道・航空回廊への投資は、リードタイムを損なうことなく排出量を削減するモーダルシフトを支援しています。欧州の医薬品物流市場規模は、コールドチェーン・テクノロジーズ社のオランダ新ハブなど継続的な容量増強の恩恵を受けており、これにより地域のPCM生産が強化され輸送リスクが低減されます。

北米は、DSCSA(医薬品安全供給法)に基づくシリアル化システムの成熟度と、パンデミック対策への持続的な公的資金投入により、引き続き主要市場としての地位を維持しています。DHLは20億ユーロ(20億8,000万米ドル)計画の50%を米国・カナダ施設に配分し、サービス水準を維持しつつ排出量を抑制する太陽光発電倉庫やLNGトラックを導入しました。フェデックスの4億4,000万米ドル規模の医療流通センター拡張と相まって、同地域はデータ可視性と持続可能性に関するベストプラクティスの再定義を続けています。

アジア太平洋地域は、中国とインドの生産増加、保険適用範囲の拡大、電子薬局の普及に支えられ、2026年から2031年にかけて5.02%のCAGRで最速の成長が見込まれています。インドが2025年にGDP準拠の倉庫設備に対して税還付を行うなど、各国政府はコールドチェーンのアップグレードを奨励しています。地域の運送業者は、中国と欧州を結ぶ回廊に沿って、鉄道・トラック・海上・航空の複合輸送ソリューションを導入し、コスト削減と輸送中の排出ガス削減を図っています。中東およびアフリカはインフラ整備が遅れていますが、湾岸協力会議(GCC)の現地化プログラムが倉庫投資を刺激し、将来の医薬品物流市場の拡大を確保しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3か月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- オンライン薬局の拡大

- OTC医薬品の需要増加と慢性疾患の負担増

- 生物製剤・ワクチン向けコールドチェーン需要の加速

- 3PL/4PL専門業者へのアウトソーシング急増

- 必須のエンドツーエンドIoT/ブロックチェーン追跡システム

- ネットゼロ物流投資によるインフラ更新の推進

- 市場抑制要因

- 温度管理配送の高コスト

- 複雑かつ多様化する世界のコンプライアンス基準

- 高度な相変化包装材料の不足

- 新興市場におけるラストマイル生物製剤配送のボトルネック

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19および地政学的イベントの影響

第5章 市場規模と成長予測

- サービスタイプ別

- 交通機関

- 道路貨物輸送

- 航空貨物

- 海上輸送

- 鉄道貨物輸送

- 倉庫保管・貯蔵

- 付加価値サービスおよびその他

- 交通機関

- 運用モード別

- コールドチェーン物流

- 非コールドチェーン物流

- 製品タイプ別

- 処方薬

- 一般用医薬品

- バイオ医薬品およびバイオシミラー

- ワクチン及び血液製剤

- 臨床試験資料

- 細胞・遺伝子治療

- 医療機器・診断機器

- 獣医学

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- ペルー

- チリ

- アルゼンチン

- その他南米

- アジア太平洋地域

- インド

- 中国

- 日本

- オーストラリア

- 韓国

- 東南アジア(シンガポール、マレーシア、タイ、インドネシア、ベトナム、フィリピン)

- その他アジア太平洋地域

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ベネルクス(ベルギー、オランダ、ルクセンブルク)

- 北欧諸国(デンマーク、フィンランド、アイスランド、ノルウェー、スウェーデン)

- その他欧州地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Deutsche Post DHL

- Kuehne+Nagel

- UPS

- FedEx

- Nippon Express

- World Courier

- SF Express

- CEVA Logistics

- DSV

- Kerry Logistics

- C.H. Robinson

- Lineage Logistics

- United States Cold Storage

- Americold Logistics

- Nichirei Logistics Group

- Kloosterboer

- NewCold Advanced Cold Logistics

- VersaCold Logistics Services

- Rhenus Logistics

- Cencora