|

市場調査レポート

商品コード

1690106

フランスのデータセンター市場:市場シェア分析、産業動向、成長予測(2025年~2030年)France Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスのデータセンター市場:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

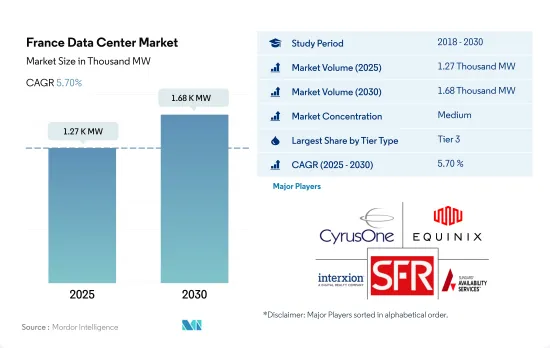

フランスのデータセンター市場規模は2025年に1,270kWと推定され、2030年には1,680kWに達し、CAGR 5.70%で成長すると予測されます。

また、2025年には17億9,930万米ドルのコロケーション収益が見込まれ、2030年には31億5,780万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは11.91%です。

ティア3データセンターは、2023年には容量ベースで大半のシェアを占め、予測期間を通じて優位を占めると予測されます。

- ティア3データセンターの容量は2023年に782.67MWに達し、さらにCAGR 4.46%を記録し、2029年には1016.98MWを超えると予測されます。一方、ティア4データセンターは成長し、CAGR6.72%を記録し、2029年までに283.98MWの容量に達すると予測されます。

- ティア1とティア2の施設は徐々に需要を失い、今後数年間で成長率が低下します。ティア1とティア2の施設は、2029年までにほぼ2%の市場シェアを維持し、成長は最小限にとどまると予想されます。これは、停電が長期化し、安定しないことが原因です。大半のユーザーは、データの保存、処理、分析に対する需要の増加により、最終的にティア3と4の施設に移行し、それぞれ市場シェアの76.5%と21.4%を占めることになります。

- 経済のBFSI部門は拡大しています。近年、フランスではオンライン・バンキングやモバイル・バンキングの利用が増加しています。欧州市場において、フランスのオンライン・バンキング普及率はトップ15に入る。2021年現在、フランスの消費者の72%がオンライン・バンキングを利用しており、2017年の62%から増加しています。このため、ティア3および4の要件を備えたホールセールおよびハイパースケール施設の建設が必要であり、eバンキングとオンライン取引の需要の高まりが原動力となっています。

- さらに、ティア4データセンターは今後数年で大幅に拡大すると予想されます。これは、クラウドベースのサービスを提供する企業が増えているためで、コロケーションスペースを最高の技術で提供する施設を建設する企業が増えています。

フランスのデータセンター市場動向

スマートフォンユーザーの増加とキャッシュレス取引が市場成長を後押し

- 2022年の同国のスマートフォンユーザー総数は5,420万人で、予測期間中にCAGR 1.25%を記録し、2029年には5,915万人に達すると予測されます。

- フランスではデジタル利用が急速に拡大しています。様々なビジネスにおけるインターネットやスマートフォンの迅速な技術導入が消費者行動に影響を与えています。例えば、2018年から2021年にかけて、フランスの1人当たりの購買力は0.9%から2%に増加しました。その結果、より多くの人がスマートフォンを購入できるようになり、スマートフォンユーザーの増加につながりました。

- 同国のインターネット普及率は2017年の80.05%から2020年には84.8%に増加し、スマートフォンユーザー数は2017年の3,970万人から2020年には4,980万人に増加しました。このような広範な利用により、デジタル決済サービスが促進され、COVID-19の流行によりその適用が増加しました。さらに、同国はウイルスが蔓延する可能性を減らすため、支払い基準額を30ユーロから50ユーロに引き上げました。人々はキャッシュレス取引を好む傾向にあり、これは市場に長期的な影響を与えると予測されます。その結果、フランスではスマートフォンの利用者が増えています。

- フランス市場におけるスマートフォンの普及は、データの絶え間ない増加をもたらし、リアルタイムの処理と分析が必要とされるこの制御不能なデータの流れに対応するため、ストレージスペースの増大が必要となります。データセンターは膨大な量のデータを管理しなければならないです。そのため、フランスのデータセンターでは、スマートフォンユーザーの増加に伴い、ラック増設の必要性が高まる可能性があります。

eコマース、5Gインフラ、ネオバンクのようなデジタルバンキングの採用が増加し、市場需要が高まる

- 2022年、フランスの平均データ速度は59.66Mbpsでした。フランスでは2000年代半ばに4Gが導入されました。フランスは2020年に5Gサービスを開始しました。両サービスの開始以来、4Gは2022年に86.72Mbpsに達し、5Gは2022年に201.3Mbpsに達しました。フランスのモバイル・サービス・プロバイダー4社(Orange、SFR、Bouygues Telecom、Free Mobile)は2013年、パリ、マルセイユ、リヨン、リール、ナントで4Gサービスのテストを行いました。4Gのカバー率は2018年初頭の45%から2020年半ばには76%に拡大しました。

- 5Gネットワーク・サービスに関しては、フランスでは2020年にノキア、オレンジ・ビジネス・サービス、フリー・モバイル、エリクソン、SNCFが商業・産業サービス向けにこれらのネットワークを展開します。フランス政府の計画によると、5Gは2030年までにフランス全土で利用可能になるはずです。大手通信事業者4社はいずれも、2022年までに3,000カ所、2024年までに8,000カ所、2025年までに10,500カ所に5Gを設置する計画を立てており、近い将来、生データの指数関数的な生成がさらに進むことを示唆しています。2Gサービスは2026年までに、3Gサービスは2029年までに廃止されます。

- 平均通信速度の向上は、eコマースやデジタル・バンキングなどのエンドユーザーが、顧客向けのオンライン・サービスを拡大する道を開きます。ネオバンク(デジタル専用銀行)は、フランスの銀行業界の今後の機能を変えつつあります。ネオバンクで開設された当座預金口座数は2018年から2.5%増加し、フランスでは350万以上の有効口座があります。とはいえ、ネオバンクユーザーの31%は、今後より頻繁に銀行のサービスを利用したいと考えています。このように、モバイルデータの高速化は、エンドユーザー業界の間でよりサービス指向のアプリケーションにつながると予想され、今後数年間はデータ処理施設の成長につながると期待されています。

フランスのデータセンター産業概要

フランスのデータセンター市場は、上位5社で60.47%を占め、緩やかに統合されています。同市場の主要企業は以下の通り。 CyrusOne Inc., Equinix Inc., Interxion(Digital Reality Trust Inc.), SOCIETE FRANCAISE DU RADIOTELEPHONE-SFR and Sungard Availability Services LP(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 市場展望

- 耐荷重

- 床面積

- コロケーション収入

- 設置ラック数

- ラックスペース利用率

- 海底ケーブル

第5章 主要業界動向

- スマートフォンユーザー数

- スマートフォン1台当たりのデータトラフィック

- モバイルデータ速度

- ブロードバンドデータ速度

- 光ファイバー接続ネットワーク

- 規制の枠組み

- フランス

- バリューチェーンと流通チャネル分析

第6章 市場セグメンテーション

- ホットスポット

- パリ(イル・ド・フランス)

- フランスのその他の地域

- データセンターの規模

- 大規模

- 超大規模

- 中規模

- メガ

- 小規模

- ティアタイプ

- ティア1と2

- ティア3

- ティア4

- 吸収量

- 非利用

- 利用

- コロケーションタイプ別

- ハイパースケール

- リテール

- ホールセール

- エンドユーザー別

- BFSI

- クラウド

- eコマース

- 政府機関

- 製造業

- メディア&エンターテイメント

- テレコム

- その他エンドユーザー

第7章 競合情勢

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Cogent Communications

- CyrusOne Inc.

- Equinix Inc.

- Euclyde Data Centers

- Global Switch Holdings Limited

- Interxion(Digital Reality Trust Inc.)

- Scaleway SAS(Illiad Group)

- SOCIETE FRANCAISE DU RADIOTELEPHONE-SFR

- Sungard Availability Services LP

- Telehouse(KDDI Corporation)

- Thesee DataCenter

- Zenlayer Inc.

- LIST OF COMPANIES STUDIED

第8章 CEOへの主な戦略的質問

第9章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The France Data Center Market size is estimated at 1.27 thousand MW in 2025, and is expected to reach 1.68 thousand MW by 2030, growing at a CAGR of 5.70%. Further, the market is expected to generate colocation revenue of USD 1,799.3 Million in 2025 and is projected to reach USD 3,157.8 Million by 2030, growing at a CAGR of 11.91% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, and is expected to dominate through out the forecasted period

- The tier 3 data center capacity is expected to reach 782.67 MW in 2023 and is further projected to register a CAGR of 4.46%, surpassing 1016.98 MW by 2029. On the other hand, the tier 4 data center is predicted to grow and register a CAGR of 6.72% to reach a capacity of 283.98 MW by 2029.

- Facilities in tier 1 and tier 2 gradually lose their demand and display a decrease in growth in the upcoming years. Tier 1 and 2 facilities are expected to hold a market share of nearly 2% by 2029 with minimal growth. This is a result of the prolonged and inconsistent outages. Most users will eventually switch to tier 3 and 4 facilities, holding 76.5% and 21.4% of the market share, respectively, owing to the increased demand for storing, processing, and analyzing data.

- The BFSI sector of the economy is expanding. In recent years, France has seen a rise in the use of online and mobile banking. In the European market, France has one of the top 15 best rates of online banking penetration. As of 2021, 72% of French consumers were using online banking, which increased from 62% in 2017. This necessitates the construction of wholesale and hyperscale facilities, which have tier 3 and 4 requirements and is driven by the rising demand for e-banking and online transactions.

- Additionally, tier 4 data centers are expected to expand significantly in the years to come. This is because more businesses are providing cloud-based services, which has caused more businesses to construct facilities to provide colocation space with the best technology.

France Data Center Market Trends

Rising smartphone users and cashless transactions boost the market growth

- The total number of smartphone users in the country was 54.20 million in 2022, which is expected to register a CAGR of 1.25% during the forecast period to reach a value of 59.15 million by 2029.

- Digital usage is expanding rapidly in France. The quick internet and smartphone technology adoption in various businesses has impacted consumer behavior. For instance, from 2018 to 2021, the per capita purchasing power per person in France increased from 0.9% to 2%. As a result, more people can purchase smartphones, leading to a growing number of smartphone users.

- The internet penetration of the country increased from 80.05% in 2017 to 84.8% in 2020, while the number of smartphone users increased from 39.7 million in 2017 to 49.8 million in 2020. Owing to such extensive use, digital payment services were promoted, and their application increased due to the COVID-19 pandemic. Additionally, the nation raised the payment threshold from EUR 30 to EUR 50 to lessen the chance of the virus spreading. People are now more inclined to prefer cashless transactions, which is predicted to have a long-term impact on the market. Consequently, there are more smartphone users in France.

- The rising use of smartphones in the French market results in a constant increase in data, necessitating a growing amount of storage space to accommodate this uncontrollable flow of data with the need for real-time processing and analysis. The data centers must manage the sheer amount of data. Thus, the requirement for extra racks in French data centers may increase as the number of smartphone users rises.

Rising adoption of e-commerce, 5G infrastructure and digital banking such as Neobank increases the adoption of market demand

- In 2022, the nation's average data speed was 59.66 Mbps. The mid-2000s saw the introduction of 4G in France. France launched its 5G services in 2020. Since the launch of both services, 4G reached 86.72 Mbps in 2022 and 5G reached 201.3 Mbps by 2022. Four French mobile service providers, Orange, SFR, Bouygues Telecom, and Free Mobile, tested their 4G offerings in 2013 in Paris, Marseille, Lyon, Lille, and Nantes, which are significant 4G hotspots. The 4G coverage has grown from 45% at the beginning of 2018 to 76% by the middle of 2020.

- In terms of 5G network services, France saw the deployments of these networks in 2020 for commercial and industrial services from Nokia, Orange Business Services, Free Mobile, Ericsson, and SNCF. According to French government plans, 5G should be available across the country by 2030. All four major operators had planned to install 5G in 3,000 locations by 2022, 8,000 by 2024, and 10,500 by 2025, which will further suggest the exponential generation of raw data in the near future. The 2G and 3G services will be decommissioned by 2026 and 2029, respectively.

- The increased average speed is paving the way for end users, such as e-commerce, and digital banking, to expand their online services for customers. Neobanks, or digital-only banks, are changing how France's banking industry functions in the future. The number of current accounts opened in neobanks has increased by 2.5% from 2018, and France has over 3.5 million active accounts. Nevertheless, 31% of Neobank users want to use banks' services more frequently in the future. Thus, the rise in mobile data speed is expected to lead to more service-oriented applications among end-user industries and is expected to lead to the growth of data processing facilities in the coming years.

France Data Center Industry Overview

The France Data Center Market is moderately consolidated, with the top five companies occupying 60.47%. The major players in this market are CyrusOne Inc., Equinix Inc., Interxion (Digital Reality Trust Inc.), SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR and Sungard Availability Services LP (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 France

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 Paris (Ile-De-France)

- 6.1.2 Rest of France

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Cogent Communications

- 7.3.2 CyrusOne Inc.

- 7.3.3 Equinix Inc.

- 7.3.4 Euclyde Data Centers

- 7.3.5 Global Switch Holdings Limited

- 7.3.6 Interxion (Digital Reality Trust Inc.)

- 7.3.7 Scaleway SAS (Illiad Group)

- 7.3.8 SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR

- 7.3.9 Sungard Availability Services LP

- 7.3.10 Telehouse (KDDI Corporation)

- 7.3.11 Thesee DataCenter

- 7.3.12 Zenlayer Inc.

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms