|

市場調査レポート

商品コード

1910825

欧州の電気トラック市場- シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Electric Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の電気トラック市場- シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

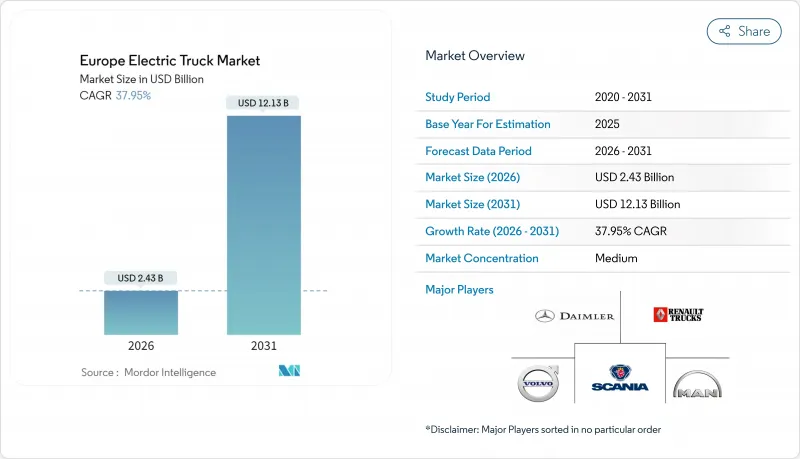

欧州の電気トラック市場は、2025年の17億6,000万米ドルから2026年には24億3,000万米ドルへ成長し、2026年から2031年にかけてCAGR37.95%で推移し、2031年までに121億3,000万米ドルに達すると予測されています。

この急成長の背景には、欧州連合(EU)の拘束力のあるCO2削減目標、バッテリーパック価格の下落、メガワット級充電回廊の急速な整備が進んでいることが挙げられます。これらの要因が相まって、電気トラックは特に利用頻度の高い物流ルートにおいて、試験的なプロジェクトから主流のフリート資産へと移行しつつあります。規制の期限がメーカーに生産拡大を迫る一方、企業の持続可能性への取り組みが確固たる購入注文へと結びつき、需要を安定化させ規模の経済を促進しています。同時に、電池エネルギー密度の向上、再生可能エネルギーの普及拡大、革新的な資金調達モデルにより、ディーゼル車との総所有コスト(TCO)の差が縮小し、地域間輸送や長距離輸送分野での導入がさらに加速しています。その結果、欧州の電気トラック市場は、早期導入者層から、大陸の主要貨物輸送ルートすべてに及ぶ広範な商業的展開へと移行しつつあります。

欧州電気トラック市場の動向と洞察

EUのCO2排出基準と2040年ゼロエミッション車販売義務

拘束力のあるCO2削減目標により、ゼロエミッショントラックは任意の持続可能性選択ではなく法的要件となりました。2030年および2035年の中間目標は明確な販売数量の指標となり、メーカーが数十億米ドル規模の電動化投資を正当化する根拠を提供します。フリート運営事業者は厳しい不適合罰則に直面するため、大規模なバッテリー式電気自動車および燃料電池モデルの調達を推進しています。ドイツの排出ガスゼロ都市圏政策などの国家政策はコンプライアンス網をさらに強化し、欧州の電気トラック市場が2040年の期限よりはるかに前に勢いを増すことを確実なものとしています。

急速なバッテリーパックコストの低下

2024年にはバッテリーパック価格が20%下落し、キロワット時(kWh)あたり115米ドルで安定しました。年間走行距離8万kmを超える高走行距離物流フリートにおいて、燃料費削減が資本コストのプレミアムを相殺するため、ディーゼル車とのコストパリティが最初に実現します。LFP化学の普及拡大により、原材料リスクが低減され、充放電サイクル寿命が4,000回以上に延長され、総所有コストがさらに低下します。欧州におけるギガファクトリーの建設はサプライチェーンを短縮し、地域調達比率を高め、急峻な学習曲線を支える規模の経済を強化します。

ディーゼル車との初期車両コスト比較

電気トラックは依然としてディーゼル車と比較して40~60%の価格プレミアムが存在し、中南欧の価格に敏感な事業者にとっては障壁となっています。このプレミアムはバッテリーコスト、低生産量、技術的複雑性を反映していますが、急速なコスト低下により、この制約は2027~2028年までに大幅に緩和される見込みです。低金利融資へのアクセス制限は、小規模フリート事業者にとってこの問題をさらに深刻化させます。しかしながら、トラック・アズ・ア・サービス(TaaS)モデルや政府のインセンティブにより、資本支出をキャッシュフローパターンに適合した運用経費構造へ転換することで、この不利な条件を相殺する動きが加速しています。

セグメント分析

2025年時点で欧州電気トラック市場規模の76.12%をバッテリー式電気トラックが占めておりますが、燃料電池モデルは2031年までに42.75%という最も高いCAGRで推移すると予測されます。初期段階での優位性は、充電ステーション網の密度、小口配送や地域貨物輸送における実証済みの信頼性、そして長距離走行を日常的に行うフリートにおける低い運用コストに起因しております。予測期間中、水素燃料補給ネットワークはスカンジナビアとドイツに拡大し、高い稼働率と迅速なターンアラウンドを必要とする重量貨物輸送や温度管理が必要な商品分野における燃料電池の普及を促進します。プラグインハイブリッドは、ゼロエミッション区域規制により内燃機関バックアップモードが完全に排除され始めるにつれ、縮小する過渡的なニッチ市場を占めることになります。

フリート使用事例の整合性から、夜間デポ充電が最も簡便なインフラモデルである都市部および短距離地域路線では、今後もバッテリー電気自動車形式が優位を維持します。燃料電池駆動は、1日600kmを超える路線で特に強化されます。これは、大型バッテリーパックによる積載量ペナルティが、そうでなければ1回あたりの収益を損なう可能性があるためです。バッテリーのエネルギー密度が向上し充電曲線が急峻化するにつれ、現在の燃料電池導入候補路線の測定可能な割合が純粋なバッテリーソリューションに転換する可能性があり、欧州電気トラック市場における競合の動的な性質を浮き彫りにしています。

2025年時点で、12トン超の大型リジッドトラックは欧州電気トラック市場規模の47.05%を占めます。予測可能なハブ・アンド・スポーク型物流サイクルはバッテリー利用率を最大化し、デポ充電設備への投資を正当化します。2026年以降は、メガワット級充電器が欧州全域の貨物ネットワークに展開され、高度な熱管理技術が長距離運行サイクル下での電池パック寿命を維持するにつれ、トラクタートレーラーセグメントが39.05%のCAGRで最も急速な拡大を示します。3.5トンまでの小型トラックは、排出ガス規制が適用される密集した都市部において、着実な普及を続けています。ごみ圧縮車やクレーン装備シャーシなどの中型特殊車両は自治体からの関心が高まっていますが、年間販売台数は低水準です。

競争の舞台は大型トラクター分野で激化しており、中国の新興企業や欧州のスタートアップ企業が、総コスト削減を約束する統合型ハードウェア・ソフトウェア・スタックを提案しています。既存OEMメーカーは、地域内および国境を越えた用途の両方に最適化されたモジュラープラットフォームで対応し、サービスネットワークの優位性維持を目指しています。その結果、欧州の電気トラック市場ではトラクターセグメントで価格形成が急速に進み、ポートフォリオ全体の基準点が設定される見込みです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EU二酸化炭素排出基準および2040年ゼロエミッション車販売義務

- 急速なバッテリーパックコストの低下

- 企業向けフリートの脱炭素化への取り組み

- 購入奨励策および道路通行料免除

- メガワット充電回廊による長距離輸送ルートの開拓

- トラック・アズ・ア・サービス(TaaS)ファイナンスモデル

- 市場抑制要因

- ディーゼル車と比較した車両の初期費用の高さ

- 公共の大型電気自動車対応充電インフラの不足

- デポレベルにおける電力容量の制約

- 電気トラックの整備技術と部品の不足

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額(米ドル)および数量(台数))

- 推進タイプ別

- バッテリー式電気自動車

- 燃料電池電気自動車

- プラグインハイブリッド

- トラックタイプ別

- 小型トラック(3.5トン以下)

- 中型トラック(3.6~12トン)

- 大型トラック(12トン以上)

- トラクター・トレーラー

- バッテリータイプ別

- リチウム・ニッケル・マンガン・コバルト酸化物(NMC)

- リン酸鉄リチウム(LFP)

- その他(NCA、LTO、固体プロトタイプ)

- バッテリー容量別

- 50kWh未満

- 50~250キロワット時

- 250kWh以上

- 範囲別

- 200kmまで(都市部)

- 201~400km(地域配送)

- 400km以上(長距離)

- 用途別

- 物流・小口配送

- 自治体サービス(廃棄物処理、道路清掃)

- 建設・鉱業

- 小売業および消費財配送

- 公益事業およびその他産業

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- オランダ

- スペイン

- スウェーデン

- ノルウェー

- デンマーク

- ベルギー

- ポーランド

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- AB Volvo

- Daimler Truck AG(Mercedes-Benz Trucks)

- Scania AB

- MAN Truck and Bus(SE)

- DAF Trucks N.V.

- Renault Trucks

- IVECO Group N.V.

- BYD Co. Ltd.

- Tesla Inc.

- Einride AB

- Tevva Motors Ltd.

- E-Force One AG

- Quantron AG

- Ford Motor Company

- Nikola Motor Europe

- Hyundai Motor Company

- E-Trucks Europe BV

- Lion Electric(EU operations)