|

市場調査レポート

商品コード

1689813

世界の患者中心のヘルスケアアプリ- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Global Patient-centric Health Care App - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の患者中心のヘルスケアアプリ- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

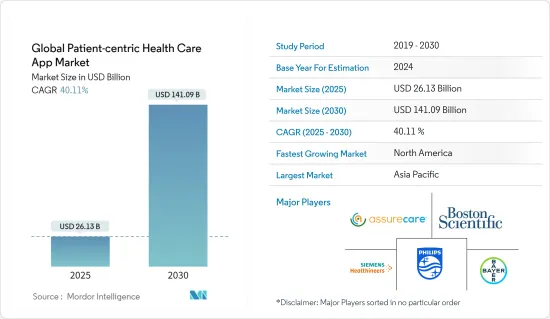

患者中心のヘルスケアアプリの世界市場規模は、2025年に261億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは40.11%で、2030年には1,410億9,000万米ドルに達すると予測されます。

COVID-19の大流行は医療産業に影響を与えました。COVID-19の流行は、あらゆる産業セグメントの混乱、課題、制限、変化につながりました。パンデミックは調査対象市場にも影響を与えました。COVID-19の大流行は市場に好影響を及ぼしたが、これはロックダウンによって臨床現場における医師の稼働率が低下したためです。

そのため、患者は糖尿病や高血圧などの慢性疾患を管理するためにアプリを利用する傾向が強まりました。さらに、COVID-19管理のために多くの患者ケアアプリが立ち上げられました。全国的なロックダウンの結果、病院やクリニックによる医療サービスが提供されなくなり、疾病管理を目的とした患者中心のヘルスケアアプリの利用が増加しました。

例えば、2020年12月にJournal of Medical Internet Researchに掲載されたHaridimos Kondylakisらの調査研究によると、モバイルアプリは、病院の負担軽減、個人の症状や精神状態の追跡、信頼できる情報へのアクセスの提供、新たな予測因子の発見など、パンデミックによって課せられた重大な課題に直面する医療専門家、市民、意思決定者にとって貴重なツールであると考えられ、医療提供者と消費者の両方から産業全体でモバイルヘルスアプリの高い採用につながりました。

市場成長を促進する主要因としては、特に高齢者層におけるがん、糖尿病、関節リウマチなどの慢性疾患の発生率の増加が挙げられます。慢性疾患の治療には、適切な診断と投薬のための生理学的変化の継続的なモニタリングと評価が必要です。

例えば、IDF Diabetes Atlas Tenth edition 2021によると、2021年には約5億3,700万人の成人が糖尿病を患っています。糖尿病患者の総数は、2030年には6億4,300万人、2045年には7億8,300万人に増加すると予測されています。糖尿病患者の増加により、モニタリングアプリの需要が高まり、市場を牽引する

2021年10月に発表された世界保健機関(WHO)のデータによると、2015~2050年にかけて、世界の60歳以上の人口の割合は12%から22%へとほぼ倍増し、高齢者の80%は低・中所得国に住むことになります。どの国も、医療社会システムがこの人口動態の変化を最大限に活用できるようにするための大きな課題に直面しています。そのため、ヘルスケアアプリはバイタルパラメーターをモニタリングする役割を担うようになります。これが市場を牽引すると予想されます。このように、高齢者の増加、電子カルテシステムを維持するための政府のイニシアチブの高まり、投薬ミスを回避するための技術ベースの治療に対する需要の増加は、予測期間にわたって患者中心のヘルスケアアプリ(PCHA)市場を牽引する可能性が高いです。

患者中心のヘルスケアアプリ市場動向

電話ベースのアプリサブセグメントが患者中心のヘルスケアアプリ市場で大きな市場シェアを占める見込み

予測期間中、患者中心のヘルスケアアプリ市場全体では、電話ベースのアプリが最大の収益シェアを占めると予測されます。

COVID-19パンデミック2020の間、医療、幸福、社会的つながりの維持は、高齢者にとって極めて重要でした。COVID-19パンデミックに対抗するために各国が遠隔医療規制を緩和した後、多くのモバイルヘルスアプリが発売されました。モバイルヘルスアプリは患者の健康状態を助け、医師はその場でサービスを記載しています。Dina M. El-Sherif & MohamedAbouzidが2022年6月に発表した調査研究によると、モバイルアプリケーションはCOVID-19パンデミックの間、COVID-19以外の管理や患者において重要な役割を果たしました。さらに2021年1月、インドではデル・ Technologiesが保健家族福祉省とタタ・トラストと共同で、全国の政府一次医療センター(PHC)で非感染性疾患を管理するためのモバイルアプリケーションを開発しました。

世界的にスマートフォンユーザーの普及が進み、遠隔医療やモバイルヘルスサービスに対する需要が高まる中、遠隔医療サービスを提供する企業があらゆる利点を備えたアプリケーションを発売するため、電話ベースの健康アプリケーションセグメントは予測期間中に成長すると予想されます。

電話ベースのヘルスケアアプリケーションの他の利点には、インタラクティブでユーザーフレンドリーなインターフェース、診察から決済までの統合ソリューション、ユーザーの最新情報を維持するための定期的な通知、プロバイダや機能によっては、電話ベースのヘルスケアアプリケーションをインターネットなしで使用することもできます。これらすべての要因が、予測期間中、調査対象セグメントの成長を後押しすると予想されます。

北米が市場を独占、予測期間中も同様と予測

北米は、予測期間を通じて患者中心のヘルスケアアプリ(PCHA)市場全体を支配すると予想されます。この優位性は、冠動脈性心疾患、心房細動、脳卒中、高血圧、糖尿病などの慢性疾患を持つ膨大な対象人口による。

米国心臓病学会(American College of Cardiology Foundation)2021によると、米国では2020年のCOVID-19パンデミック時に高血圧性疾患と虚血性心疾患による死亡が増加し、米国でのパンデミック時に患者中心のヘルスケアアプリが疾患管理に使用されるようになりました。

高齢者の増加と慢性疾患の負担が大きい同国は、市場成長を後押しすると予想されます。例えば、米国疾病予防管理センター(CDC)の2020年9月によると、心臓病は米国における主要死因です。毎年約80万5,000人の米国人が心臓発作を経験しています。心臓疾患による死亡者数が増加しているため、心臓疾患の適切なモニタリングに対する継続的なニーズがあり、患者中心のヘルスケアアプリはアンメットニーズを満たすため、予測期間中に成長を示すと予想されます。さらに、米国糖尿病連盟の2019年版レポートによると、世界中で推定4億6,300万人の成人が糖尿病を患っており、2045年には7億人に達すると推定されています。

さらに、医療支出の増加、健康意識、臨床中心の治療から患者中心の治療へのシフトが、この地域の市場を押し上げています。同地域の主要医療プロバイダによる技術採用の拡大は、予測期間を通じて世界市場シェアの大幅な拡大に貢献すると予想されます。

患者中心のヘルスケアアプリ産業概要

患者中心のヘルスケアアプリ市場の競争は中程度です。市場ポジションを拡大している企業もあれば、市場ポジションを維持するためにM&A、新製品の導入、技術のアップグレードなど、さまざまな戦略を採用している企業もあります。市場参入企業には、Koninklijke Philips N V、Merck & Co.Inc.、Hill-Rom Holdings Inc.、Bayer AG、Siemens Healthineers AGなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 慢性疾患の有病率の増加と高齢者の増加

- 新規技術によるアクセスの向上と柔軟性

- 市場抑制要因

- 開発コストの高さ

- 通常の医療プロバイダによる消極的姿勢

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 運営形態別

- 電話ベース

- ウェブベース

- ハイブリッド患者中心アプリ

- 用途別

- ウェルネス管理

- 疾病・治療管理

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Boston Scientific Corporation

- Assurecare LLC(IPatient Care)

- Merck & Co. Inc.

- MobileSmith Inc.

- Koninklijke Philips NV

- Pfizer Inc.

- Siemens Healthineers AG

- Novartis AG

- Bayer AG

- Baxter International Inc.(hillrom Services, Inc.)

- athenahealth Inc.

- Allscripts Healthcare Solutions Inc.

- International Business Machines Corporation(IBM)

- Mfine Pvt. Ltd

- Oracle(cerner Corporation)

第7章 市場機会と今後の動向

The Global Patient-centric Health Care App Market size is estimated at USD 26.13 billion in 2025, and is expected to reach USD 141.09 billion by 2030, at a CAGR of 40.11% during the forecast period (2025-2030).

The COVID-19 pandemic had an impact on the healthcare industry. The outbreak of COVID-19 led to disruption, challenges, limitations, and changes in every industry sector. The pandemic also impacted the studied market. The outbreak of COVID-19 showed a positive impact on the market, as lockdowns led to the lower availability of doctors in clinical settings.

Thus, patients were more inclined to use apps to manage their chronic conditions, such as diabetes, hypertension, and other chronic diseases. Moreover, there have been a large number of patient care apps launched for COVID-19 management. Nationwide lockdowns resulted in providing healthcare services by the hospitals and clinics, which led to the rise in the use of patient-centric healthcare app that aims toward the management of diseases.

For instance, according to a research study by Haridimos Kondylakis et al., published in the Journal of Medical Internet Research in December 2020, mobile apps were considered to be a valuable tool for health professionals, citizens, and decision-makers in facing critical challenges imposed by the pandemic such as reducing the burden on hospitals, tracking the symptoms and mental health of individuals, providing access to credible information, and discovering new predictors, leading to the high adoption of mobile health apps across the industry both from providers and consumers.

The major factors driving the market growth include the increased incidence of chronic disorders, such as cancers, diabetes, and rheumatoid arthritis, especially in the geriatric population. Treating chronic diseases requires continuous monitoring and evaluation of physiological changes for proper diagnosis and medication.

For instance, as per the IDF Diabetes Atlas Tenth edition 2021, in 2021, about 537 million adults were living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The increasing number of diabetes patients drives them to demand more monitoring apps and drives the market

According to World Health Organization (WHO) data published in October 2021, between 2015 and 2050, the proportion of the global population over 60 years will nearly double from 12% to 22% in 2050, and 80% of older people will be living in low- and middle-income countries. All countries face major challenges in ensuring their health and social systems are ready to make the most of this demographic shift. Thus, healthcare apps come in the role of monitoring vital parameters. This is expected to drive the market. Thus, the growing elderly population, rise in government initiatives to maintain electronic health record systems, and increased demand for technology-based treatment to avoid medication errors are likely to drive the patient-centric healthcare app (PCHA) market over the forecast period.

Patient Centric Healthcare App Market Trends

The Phone-based Apps Sub-segment is Expected to Hold Significant Market Share in the Patient-centric Healthcare App Market

The phone-based apps are expected to account for the largest revenue share in the overall patient-centric healthcare app market over the forecast period.

During the COVID-19 pandemic 2020, the maintenance of healthcare, well-being, and the social connection was crucial for the elderly population. Many mobile health apps were launched after countries relaxed their telehealth regulations to combat the COVID-19 pandemic. Mobile health apps help patients with their health conditions, and physicians deliver the services on their premises. According to the research study published in June 2022 by Dina M. El-Sherif& Mohamed Abouzid, mobile applications played a crucial role during the COVID-19 pandemic in management and patients other than COVID-19. Additionally, in January 2021, in India, Dell Technologies, in collaboration with the Ministry of Health and Family Welfare and Tata Trusts, developed a mobile application to manage non-communicable diseases at the government primary health centers (PHCs) across the country.

With the growing penetration of smartphone users globally and increasing demand for telehealth and mobile health services, the phone-based health application segment is expected to grow over the forecast period as companies offering telehealth services launch their applications with all the benefits.

Other advantages of phone-based health applications include an interactive and user-friendly interface, integrated solutions from consultation to payment, regular notification to keep the user updated, and depending upon the provider and function, phone-based healthcare applications can also be used without the internet. All these factors are collectively expected to boost growth in the studied segment over the forecast period.

North America Dominates the Market and Expected to do the Same in the Forecast Period.

North America is expected to dominate the overall patient-centric healthcare app (PCHA) market throughout the forecast period. The dominance is due to the region's huge target population base with chronic diseases, such as coronary heart diseases, atrial fibrillation, stroke, hypertension, and diabetes.

As per the American College of Cardiology Foundation 2021, deaths from hypertensive diseases and ischemic heart disease in the United States increased during the COVID-19 pandemic in 2020, leading to the increasing use of patient-centric health care apps during the pandemic in the United States in the management of the disease.

The rising geriatric population and the country's high burden of chronic diseases are expected to boost market growth. For instance, Heart disease is the main cause of death in the United States, according to the Centers for Disease Control and Prevention (CDC) September 2020. Around 805,000 Americans experience a heart attack each year. As the number of deaths due to heart diseases is increasing, there is a continuous need for the proper monitoring of cardiac diseases, and patient-centric healthcare apps fulfill the unmet needs; hence it is expected to show growth over the forecast period. Additionally, According to the American Diabetes Federation 2019 report, an estimated 463 million adults live with diabetes worldwide, which is estimated to reach 700 million by 2045.

Furthermore, a rise in healthcare expenditure, health awareness, and a shift from clinical-centric treatment to patient-centric care boost the market in the region. The growing adoption of technology by key healthcare providers in the region is expected to contribute to a significant global market share throughout the forecast period.

Patient Centric Healthcare App Industry Overview

The patient-centric healthcare app market is moderately competitive. Some companies are expanding their market position while others are adopting various strategies, such as mergers and acquisitions, introducing new products, and upgrading technologies, to maintain their market position. Some market players are Koninklijke Philips N V, Merck & Co. Inc., Hill-Rom Holdings Inc., Bayer AG, and Siemens Healthineers AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases and Rising Geriatric Population

- 4.2.2 Enhanced Access and Flexibility with Novel Technologies

- 4.3 Market Restraints

- 4.3.1 The High Cost of Development

- 4.3.2 Reluctance by Regular Healthcare Providers

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Mode of Operation

- 5.1.1 Phone-based

- 5.1.2 Web-based

- 5.1.3 Hybrid Patient-centric Apps

- 5.2 By Application

- 5.2.1 Wellness Management

- 5.2.2 Disease And Treatment Management

- 5.2.3 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boston Scientific Corporation

- 6.1.2 Assurecare LLC (IPatient Care)

- 6.1.3 Merck & Co. Inc.

- 6.1.4 MobileSmith Inc.

- 6.1.5 Koninklijke Philips NV

- 6.1.6 Pfizer Inc.

- 6.1.7 Siemens Healthineers AG

- 6.1.8 Novartis AG

- 6.1.9 Bayer AG

- 6.1.10 Baxter International Inc. (hillrom Services, Inc.)

- 6.1.11 athenahealth Inc.

- 6.1.12 Allscripts Healthcare Solutions Inc.

- 6.1.13 International Business Machines Corporation (IBM)

- 6.1.14 Mfine Pvt. Ltd

- 6.1.15 Oracle (cerner Corporation)