|

市場調査レポート

商品コード

1910579

米国の包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United States Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

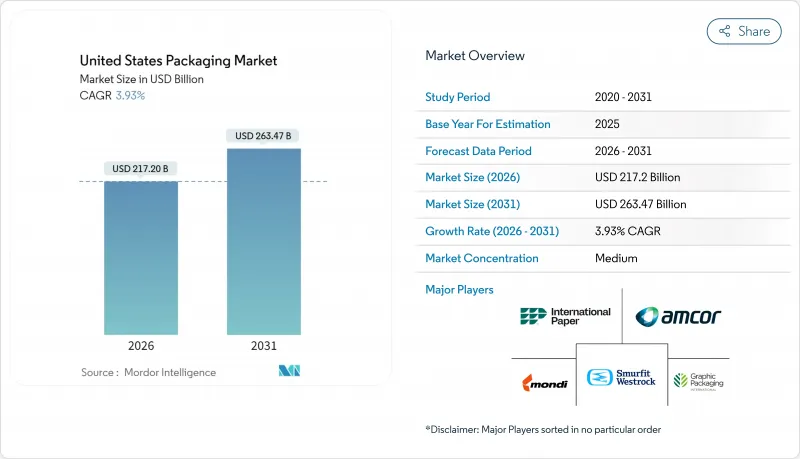

米国の包装市場は、2025年の2,089億8,000万米ドルから2026年には2,172億米ドルへ成長し、2026年から2031年にかけてCAGR 3.93%で推移し、2031年までに2,634億7,000万米ドルに達すると予測されています。

9,408億米ドル規模のトラック輸送業界との強固な連携が米国の包装市場の回復力を支えております。包装の設計や重量が直接的に貨物輸送コストに影響を与えるためです。電子商取引の拡大、州レベルの拡大生産者責任法(EPR)などの規制変化、医薬品生産能力の国内回帰加速が、自動化対応ラインや高バリア性素材への投資を促進しております。米国市場は食品・飲料分野におけるプレミアム化の恩恵を受け続けていますが、PFASフリー規制やポリマー生産能力増強によるコスト圧力により、コンバーター企業の利益率は圧迫されています。大規模な統合サプライヤーは、規模と研究開発の深みを活かして規制順守コストを吸収し、価格決定力を維持しています。一方、中小規模企業はニッチ市場での差別化を図っています。

米国の包装市場の動向と洞察

Eコマースの急成長が小口包装需要を牽引

自動化対応の二次ラインへの投資により、消費財メーカーは労働力不足とSKUの増加を効率的に管理できます。メアリーケイ社は200万米ドルの設備更新後、ライン労働力を85%削減しながら毎分50~60ユニットの生産を維持しました。主要運送会社の容積重量課金制度は小型軽量小包を優遇し、適切なサイズの段ボールインサートや緩衝材の需要を刺激しています。米国の包装市場がオムニチャネル対応へ移行する中、保護機能・ブランド化・データ豊富な統合ソリューションを提供するコンバーターは、ラストマイルコスト削減を目指す小売業者からの受注を獲得しています。自動化は流通業者のピッキング・パッキングミス削減と翌日配送の実現を支援し、信頼性の高い二次包装が競争上の必須要件となっています。サプライチェーンリスク軽減のため基材の複数調達が進み、多様な素材ポートフォリオを持つコンバーターが恩恵を受けています。

食品・飲料分野におけるプレミアム化が、高バリア性フレキシブル包装の需要を加速させております。

プレミアムブランドは、保存期間を延長しクリーンラベル処方に対応する多層高バリアフィルムへ移行しており、この動きが米国の包装市場における単価上昇を牽引しています。高度なコーティング技術は酸素・光・湿気を遮断し、添加物なしの天然風味を保護するとともに食品廃棄を削減します。消費者は再封可能な注ぎ口や透明窓付きパウチを好むため、コンバーターはバリア性能と店頭での訴求力のバランスが求められています。FDAの食品接触認可はコンプライアンスの複雑さを増し、低設備投資の競合他社の参入を制限しています。ブランドオーナーは、消費者が認識する品質に対して支払う意思があることを中心としたマージン拡大戦略により、高い包装コストを正当化しています。オーガニックスナックやレディ・トゥ・ドリンクコーヒーの売上増加に伴い、プレミアムフレキシブル包装への需要が高まり、フィルム押出メーカーの長期受注が強化されています。

カリフォルニア州SB-54法拡大生産者責任制度のコスト転嫁

ニューサム知事は事業負担を理由に初期規制の実施を延期しましたが、2032年までにプラスチックを25%削減する義務と50億米ドルの廃棄物基金は有効です。生産者はリサイクルインフラへの資金提供と包装の再設計、あるいは段階的料金の支払いが求められます。米国の包装市場の大手企業はコストを幅広い製品群に分散できる一方、中小コンバーターは利益率の低下と設備投資能力の縮小に直面しています。不確実性により新製品投入が停滞し、カリフォルニア州限定SKUと全国統一規格の選択を巡る議論が州間物流を複雑化させています。ブランドオーナーへのコスト転嫁は店頭価格に圧力をかけ、選択的消費財カテゴリーの販売数量成長を鈍化させる可能性があります。

セグメント分析

プラスチックは汎用性とコスト効率の高さから、2025年時点で米国の包装市場シェアの35.88%を維持しました。しかしながら紙・板紙はCAGR5.33%で拡大しており、小売業者が繊維系代替品の導入を約束する中、2031年までにプラスチックのシェアを一部侵食すると予測されます。エネルギー省がセルロース系フィルムに5,200万米ドルを拠出する動きは、次世代基材に対する公共部門の支援を示しています。天然HDPEの不足により、2025年3月には再生樹脂価格が1ポンドあたり96セントに達し、ボトルからボトルへのリサイクルプロジェクトに課題が生じています。

米国の包装市場のプラスチック加工業者は、カーボンアカウンティングの要求と樹脂供給過剰リスクという二重の圧力に直面しています。投資はリサイクル性を考慮した単一素材PEフィルムへ移行する一方、多層ナイロン構造は高バリア紙へ移行しています。飲料メーカーが無限リサイクルを謳う合金缶を採用する中、金属包装の需要は維持されています。全体として、素材選定では基本性能以上に、コスト、循環性指標、規制リスクのバランスが重視されるようになりました。

2025年、紙・板紙製品は段ボールの大量消費により米国の包装市場シェアの28.70%を占めました。金属製品は炭酸飲料やハードセルツァーが軽量化とリサイクル利点を求めてアルミ缶を選択したため、CAGR6.64%で成長すると予測されています。クラウン・ホールディングスの飲料缶収入は2024年に17%増加し、持続的な需要を裏付けています。シルガン社が金属製食品缶市場で50%のシェアを維持している事実は、常温保存可能製品の強靭性を示しています。

デジタル印刷の導入により、加工業者は季節的なSKU急増に対応可能となり、一方、HDPEジャグなどの硬質プラスチックは、バリューパックにおける食料品業界の支持を維持しています。しかしながら、金属の無限リサイクルという特性は、気候変動を気にかける消費者に共感を呼び、プロモーション予算が缶中心のフォーマットへシフトしています。LMEアルミニウム価格の変動が数量増加を抑制する可能性がありますが、ブランドオーナーは複数年のテイク・オア・ペイ契約でヘッジし、缶メーカーへの発注を安定させています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の急成長が小口包装需要を牽引

- 食品・飲料分野におけるプレミアム化の進展が、高バリア性フレキシブル包装材の需要を加速させております

- 医薬品充填・包装設備の国内回帰が滅菌包装需要を促進

- 消費財メーカーにおける自動化対応型二次包装ライン

- 小売メディアネットワークは棚出し可能なフォーマットを好みます

- バイオポリマーパイロットプラント向け米国農務省(USDA)およびエネルギー省(DOE)の助成金(注目度低)

- 市場抑制要因

- カリフォルニア州SB-54「拡大生産者責任」制度によるコスト転嫁

- PFASフリー規制による配合コストの上昇

- 2028-2029年におけるPE・PPクラッカー設備の過剰供給がコンバーターマージンを圧迫(過小報告)

- シャーシ不足による段ボール輸送の運賃上昇(過小報告)

- 業界サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 素材タイプ別

- 紙および板紙

- プラスチック

- ポリエチレンポリプロピレン(PP)

- 高密度ポリエチレン(HDPE)および低密度ポリエチレン(LDPE)

- ポリエチレンテレフタレート(PET)

- ポリ塩化ビニル(PVC)

- ポリスチレン(PS)

- その他のプラスチック製品

- 金属

- 容器ガラス

- 製品タイプ別

- 紙および板紙製品タイプ

- 折り畳み式カートンおよび硬質ボックス

- 段ボール箱およびコンテナ

- 使い捨て紙製品

- その他の紙・板紙製品タイプ

- プラスチック製品タイプ

- 硬質プラスチック

- 瓶・ジャー

- キャップおよびクロージャー

- バルクグレード製品

- その他の硬質プラスチック製品タイプ

- フレキシブルプラスチック

- パウチ

- 袋

- フィルムおよびラップ

- その他のフレキシブルプラスチック製品タイプ

- 硬質プラスチック

- 金属製品タイプ

- 缶

- キャップおよびクロージャー

- エアゾール容器

- その他の金属製品タイプ

- 容器ガラス製品タイプ

- 瓶

- 瓶

- 紙および板紙製品タイプ

- 包装形態別

- 硬質包装形態

- フレキシブル包装形態

- エンドユーザー別

- 食品

- 飲料

- 医薬品・医療

- パーソナルケアおよび化粧品

- 工業・化学

- 農業

- 自動車

- その他のエンドユーザー

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Sealed Air Corporation

- Ball Corporation

- Crown Holdings, Inc.

- Sonoco Products Company

- American Packaging Corporation

- International Paper Company

- Graphic Packaging Holding Company

- Novolex Holdings, LLC

- ProAmpac Holdings Inc.

- Silgan Holdings Inc.

- AptarGroup, Inc.

- Huhtamaki Oyj

- Printpack, Inc.

- Packaging Corporation of America

- CCL Industries Inc.

- Ardagh Group S.A.

- Smurfit WestRock plc

- Mondi plc