|

市場調査レポート

商品コード

1687223

食品サービス用包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Food Service Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 食品サービス用包装:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 137 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

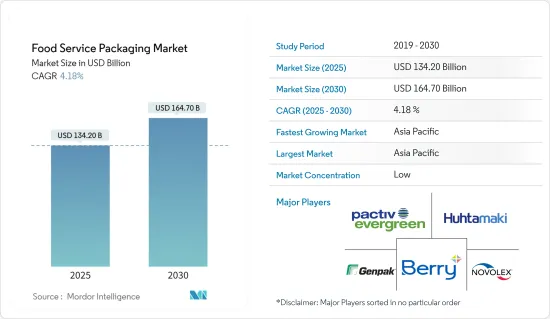

食品サービス用包装市場規模は2025年に1,342億米ドルと推定され、予測期間(2025~2030年)のCAGRは4.18%で、2030年には1,647億米ドルに達すると予測されます。

主要ハイライト

- オンラインデリバリープラットフォームとモバイルアプリが食品サービス用包装製品の成長に拍車をかけています。技術が食の展望を再形成し、より多くの投資を呼び込むにつれて、この急増はさらに強まるものと考えられます。サードパーティのオンライン食品注文サービスは急増すると予想され、多数の小規模な独立系飲食店がより広範な顧客基盤を獲得できるようになります。さらに、オンラインデリバリー食品トラックを含むクイックサービスレストラン(QSR)の成長は、食品サービス用包装、特に使い捨て包装の需要を強化します。

- ここ数年で、オンライン注文とレストランデリバリーは20%以上の成長を遂げました。オンライン食品デリバリーシステムの採用が増えるにつれ、サステイナブル包装の需要と使用が高まり、メーカーはサステイナブル包装ソリューションを選ぶようになっています。

- カフェやレストランは世界中で増加傾向にあり、食品サービス用包装市場を後押ししています。CBN-Dataが報告したように、中国だけでもカフェの数は2022年の11万5,820から2023年には13万2,830に急増しました。このカフェ数の増加は、食品サービス用包装の需要を直接促進します。多くのカフェがテイクアウトのオプションを優先することを考えると、紙袋やプラスチック容器などの包装の必要性が最も重要になります。その結果、カフェやレストランが拡大するにつれ、小売用袋の需要も増加の一途をたどっています。

- Hinojosaのようないくつかの包装会社は、飲食品産業においてよりエコフレンドリー消費習慣を促進するために企業を支援し、戦略的に競争上の優位性として持続可能性を含めることを容易にしています。外食産業はプラスチック包装の需要が最も大きい産業の1つで、2021年にはプラスチック使用量が33%以上増加します。

主要ハイライト

- 2023年3月、Hinojosa Packaging Groupは、食品に触れても安全な印刷方法を用いて様々なソリューションを提供する、食品サービス向け包装製品の新シリーズを発売しました。この容器はすべてリサイクル可能な紙で構成され、生分解性であるため、他の包装とは一線を画しています。

- しかし、サステイナブル包装は開発コストが高く、課題も多いです。多くの企業はより多くの資源を必要としており、より良い包装のためには研究開発への投資が必要となります。包装の合理化によるコスト削減の可能性も考慮しなければならないです。サステイナブル包装を使用するコストは、従来の包装よりも高いです。これは、関係する材料とその調達(バージンと中古の両方)、確立されていないサプライチェーン、製造プロセス、規模の経済性が低いためです。

- 強化された包装材料とカスタマイズは、食品サービス用包装市場の成長の極めて重要な促進要因です。これらは進化する消費者の嗜好に対応するだけでなく、ブランドID確認を強化し、持続可能性への懸念に取り組むものでもあります。2024年4月、食品包装の大手イノベーターであるSabert Corporationは最新の製品群を発表した:パルプ・プロテイン・トレイと青果物トレイです。商業的に堆肥化可能であることが証明されたこれらのトレイは、外食事業者に従来の発泡トレイに代わるサステイナブル選択肢を提供し、しかもトップクラスの品質と性能を維持しています。

外食包装市場の動向

クイックサービスレストラン(QSR)が最大のシェアを占める見込み

- KFC、Domino's、Starbucksといった世界の大手企業や地域密着型企業が提供するメニューが急増し、世界の消費者のファースト食品への関心が高まっています。この動向に拍車をかけているのは、外食志向の高まり、異文化の食嗜好の融合、めまぐるしい生活の中でのファスト食品の利便性です。QSRセグメントの成長は、国際的ブランドが提供する多様な料理の選択肢によって後押しされています。人口構成の変化と、ミレニアル世代とベビーブーム世代の健康志向の高まりは、健康を優先した食品への需要を増幅しています。

- QSRは手頃な価格のファースト食品に特化し、サービスの効率を優先しています。QSRは、テーブルサービスを最小限にとどめ、セルフサービスを重視することで、従来の飲食店とは一線を画しています。一般的にQSRは、硬質ポリスチレン(PS)、発泡ポリスチレン(EPS)、ポリプロピレン(PP)、ポリエチレンテレフタレート(PET)、ポリ乳酸(PLA)などの使い捨てプラスチック製品を利用しています。

- ロックダウンの間、多くのカフェやレストランは、カーブサイド・ピックアップやキャリーアウトに重点を置くようになりました。また、店舗内のキャパシティを削減し、食品デリバリーの需要に応えるために革新的なデリバリーサービスを導入する店もありました。その結果、飲食品産業は外食産業向け包装の需要拡大を生み出す態勢を整えました。この背景には、衛生と持続可能性が重視されるようになり、包装材料として紙が最前線に押し上げられたことが大きく影響しています。

- 発泡スチロールのカップ、プラスチックの蓋、無機質な肉が普及する中、産業はますますエコフレンドリー方向に舵を切っています。サステイナブルプラクティスに対する顧客の嗜好の高まりに後押しされ、多くの企業がよりエコフレンドリー代替品を取り入れています。マクドナルドの独立系フランチャイジーであるArcos Dorados Holdingsは、2024年6月にJ&J Green Paperの「オール天然」バリア・コーティングを採用しました。この動きは、プラスチックとPFAS化学品を排除し、消費者の廃棄物を削減することを目的としたもので、ファースト食品産業の持続可能性への取り組みにおける重要な一歩となりました。

- オン・ザ・ゴー・ダイニングの傾向の高まりと食費の増加は、QSRセグメントを強化し、その結果、食品サービス用包装の需要を押し上げています。Yum! Brandsの2024年2月の報告書によると、KFCの世界店舗数は2020年の約2万5,000店から2023年には驚異的な2万9,900店に急増しました。このようなQSR店舗の世界の増加は、今後数年間で食品サービス用包装のニーズをさらにエスカレートさせる構えです。

アジア太平洋が最大の市場シェアを占める

- アジア太平洋は人口密度の高い国々と中国やインドのような新興経済国で構成されています。食品サービスの需要は急速に伸びており、サステイナブル包装の採用が勢いを増しています。

- プラスチックは、消費者の利便性文化の基盤を形成する包装産業に不可欠な要素です。コストパフォーマンスの高さから、外食産業では段ボール、ガラス、金属といった従来の包装材料がプラスチックに取って代わられてきました。

- 堆肥化可能な食品サービスブランドのCHUKは、クイック・コマース企業のBlinkitをサステナビリティ・パートナーとして迎えました。BlinkitはCHUKの製品を10分以内に消費者に届け、消費者とCHUKの橋渡しをします。このパートナーシップにより、CHUKは2022~23年には、このプラットフォームで消費者に1兆個の商品を提供することになります。

- 日本は一人当たりの包装材消費量が多く、食品産業と包装産業は密接な関係にあります。日本の食品メーカーは、ハイテク包装技術を使用し、包装デザインに創意工夫を凝らす傾向があることで知られています。このような包装技術革新への注力は、日本における魅力的で効率的な包装ソリューションの開発につながりました。

- インドでは過去数年間、中国料理、インド料理、日本料理、汎アジア料理など、さまざまな種類のアジア料理の消費が増加したため、FSRが力強い成長を遂げてきました。インド料理は東アジア文化の影響を大きく受けており、特に若い世代に人気があります。

- Speciality Restaurantsの報告書によると、2023年度には、インドのSpeciality Restaurants Limitedの店舗数は約127店となり、2年前の117店から増加しました。この増加傾向は今後数年間も続くと予想され、それによって外食包装製品の需要が強化されます。

- 産業関係者によると、外食包装メーカーは見た目が良く、費用対効果が高く、長持ちする軟質包装に惹かれています。India Brand Equity Foundation(IBEF)によると、インドの食品・食料品市場は世界第6位で、小売が売上の70%を占めています。インドの食品加工産業は同国の食品市場全体の32%を占め、生産、消費、輸出、期待される成長において第6位にランクされています。

食品サービス用包装産業概要

食品サービス用包装市場はセグメント化されており、多くの参入企業がその提供品によって強い存在感を示しています。イノベーションと需要により、市場は新規参入企業にとって魅力的です。

- 2023年9月、Berryは、消費者使用後の再生プラスチックを少なくとも30%(PCR)含む食品グレードの低密度ポリエチレン(LLDPE)フィルムで、軟質プラスチック包装に食品グレードの再生材料を導入しました。強固なフィルムポートフォリオへのこの追加を通じて、Berryは、食品包装にPCRを含めるというブランドの持続可能性へのコミットメントに対するソリューションを提供しました。

- 2023年2月、Pactiv EvergreenはAmStyと協力し、循環型ポリスチレン食品包装製品を発売。Pactiv Evergreenの包装にはAmStyのISCC PLUS認定再生ポリスチレンが使用され、Evergreenはマスバランス配分を利用した先進リサイクル技術から生まれたISCC PLUS認定消費者使用後再生ポリスチレンにリンクした包装を購入できる機能を顧客に提供し始める。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業エコシステム分析

第5章 市場力学

- 市場促進要因

- 主要市場で高まるコンビニエンス食品需要

- 持続可能性重視による再生プラスチックへのベンダー注目の高まり

- 市場課題

- 環境圧力とポリマー価格の不安定さによる軟包装の着実な成長

第6章 市場セグメンテーション

- 製品タイプ別

- 段ボール箱とカートン

- プラスチックボトル

- トレイ、皿、食品容器、ボウル

- カップと蓋

- クラムシェル

- その他

- エンドユーザー産業別

- クイックサービスレストラン(QSR)

- フルサービスレストラン(FSR)

- 施設

- ホスピタリティ(ダイニングイン、コーヒー&スナックなど)

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Pactiv Evergreen Inc.

- Dart Container Corporation

- Amhil North America

- Genpak LLC

- Huhtamaki Oyj

- Berry Global Inc.

- Novolex Holdings LLC

- Sabert Corporation

- Silgan Plastic Food Container

- B& R Plastics Inc.

- Graphic Packaging International Inc.

- Amcor PLC

- Sonoco Products Company

第8章 投資分析

第9章 市場の将来

目次

Product Code: 56762

The Food Service Packaging Market size is estimated at USD 134.20 billion in 2025, and is expected to reach USD 164.70 billion by 2030, at a CAGR of 4.18% during the forecast period (2025-2030).

Key Highlights

- Online delivery platforms and mobile apps fuel the growth of foodservice packaging products. This surge is poised to intensify as technology reshapes the food landscape, drawing in more investments. Third-party online food ordering services are expected to surge, empowering numerous small, independent eateries to tap into a wider customer base. Additionally, the growth of quick service restaurants (QSRs), including online delivery food trucks, bolsters the demand for foodservice packaging, especially disposables.

- Over the last few years, online food ordering and restaurant delivery have grown more than 20%. With the increasing adoption of the online food delivery system, the demand and use of sustainable packaging are rising, causing manufacturers to opt for sustainable packaging solutions.

- Cafes and restaurants worldwide are on the rise, propelling the foodservice packaging market. In China alone, the cafe count surged from 115.82 thousand in 2022 to 132.83 thousand in 2023, as reported by CBN-Data. This uptick in cafe numbers directly fuels the demand for foodservice packaging. Given that many cafes prioritize takeout options, the need for packaging, such as paper bags and plastic containers, becomes paramount. Consequently, with the expanding cafe and restaurant landscape, the demand for retail bags is poised to climb.

- Several packaging companies, such as Hinojosa, assist firms in promoting more environmentally friendly consumption habits in the food and beverage industry, strategically making it easier to include sustainability as a competitive advantage. Foodservice was one of the industries with the most significant demand for plastic packaging, which witnessed plastic usage climb by more than 33% in 2021.

- In March 2023, Hinojosa Packaging Group launched a new line of foodservice packaging products that offers a range of solutions using printing methods safe for contact with food. This container is constructed entirely of recyclable paper and is biodegradable, which makes it stand out from other packaging.

- However, sustainable packaging can be expensive and challenging to develop. Many businesses need more resources, and investing in R&D would be required for better packaging. The potential cost savings from streamlined packaging must be considered. The cost of using sustainable packaging is higher than conventional packaging. This is due to the materials involved and their sourcing (both virgin and used), the less-established supply chains, manufacturing processes, and lower economies of scale.

- Enhanced packaging materials and customization are pivotal drivers of growth in the foodservice packaging market. They not only meet evolving consumer preferences but also bolster brand identity and tackle sustainability concerns. In April 2024, Sabert Corporation, a leading innovator in food packaging, unveiled its latest range: Pulp Protein and Produce Trays. These Trays, certified as commercially compostable, offer foodservice operators a sustainable choice over conventional foam trays, all while maintaining top-tier quality and performance.

Key Highlights

Food Service Packaging Market Trends

Quick Service Restaurants (QSR) Are Expected to Hold the Largest Share

- Global consumers are increasingly turning to fast food, with a surge in offerings from global giants like KFC, Domino's, and Starbucks, as well as regional players. This trend is fueled by the growing penchant for dining out, a melding of cross-cultural dietary tastes, and fast food's convenience in fast-paced lives. The QSR segment's growth is bolstered by the diverse culinary options offered by international brands. Shifting population demographics and a growing health consciousness among millennials and baby boomers are amplifying the demand for food products that prioritize wellness.

- QSRs specialize in affordable, fast food and prioritize service efficiency. They stand out from traditional dining establishments by offering minimal table service and a strong focus on self-service. Commonly, QSRs utilize single-use plastic products such as rigid polystyrene (PS), expanded polystyrene (EPS), polypropylene (PP), polyethylene terephthalate (PET), and polylactic acid (PLA).

- During the lockdowns, many cafes and restaurants pivoted to emphasize curbside pickup and carryout exclusively. Others slashed their in-store capacities, introducing innovative delivery services to meet the demand for food delivery. As a result, the food and beverage industry is poised to generate increased demand for foodservice packaging. This can be largely attributed to the heightened emphasis on hygiene and sustainability, propelling paper to the forefront as a preferred packaging material.

- Amidst the prevalence of styrofoam cups, plastic lids, and inorganic meat, the industry is increasingly pivoting toward eco-friendliness. Driven by a rising customer preference for sustainable practices, numerous companies are embracing greener alternatives. Arcos Dorados Holdings, an independent McDonald's franchisee, adopted J&J Green Paper's 'all-natural' barrier coating in June 2024. This move aimed to eliminate plastics and PFAS chemicals and reduce consumer waste, marking a significant step in the fast food industry's sustainability efforts.

- The rising trend of on-the-go dining and heightened food expenditures have bolstered the QSR segment, consequently driving up the demand for foodservice packaging. As per Yum! Brands' February 2024 report, the global count of KFC outlets surged from approximately 25,000 in 2020 to a staggering 29,900 by 2023. This global uptick in QSR establishments is poised to further escalate the need for foodservice packaging in the coming years.

Asia-Pacific Accounts for the Largest Market Share

- Asia-Pacific comprises densely populated countries and emerging economies like China and India. The demand for foodservice is growing rapidly, and the adoption of sustainable packaging is gaining momentum; it is expected to increase further during the forecast period.

- Plastic is an essential part of the packaging industry that forms the foundation of the consumer convenience culture. Owing to their cost-to-performance ratio, traditional packaging materials, such as corrugated paper boards, glass, and metals, have been substituted by plastics in foodservice.

- CHUK, a compostable foodservice brand, joined quick commerce firm Blinkit as its sustainability partner. Blinkit delivers CHUK's products to consumers within 10 minutes, bridging the gap between the consumers and CHUK. The partnership helped CHUK to serve one crore pieces to consumers on the platform FY 2022-23.

- Japan has a high per capita consumption of packaging materials, and there is a close relationship between the food and packaging industries in the country. Japanese food manufacturers are known for using high-tech packaging techniques and their tendency toward ingenuity in packaging designs. This focus on packaging innovation has led to the development of attractive and efficient packaging solutions in Japan.

- There has been strong growth of FSRs in India during the past years due to the rise in the consumption of different varieties of Asian cuisine, including Chinese, Indian, Japanese, and Pan-Asian. Indian cuisine is significantly influenced by East Asian culture and is particularly popular among the younger generation.

- As per the Speciality Restaurants report, in FY 2023, there were about 127 outlets of Speciality Restaurants Limited in India, up from 117 stores two years prior. This uptrend is also expected to be witnessed in the upcoming years, thereby bolstering the demand for foodservice packaging products.

- According to industry insiders, foodservice packaging manufacturers are gravitating toward flexible packaging as it is visually appealing, cost-effective, and long-lasting. According to the India Brand Equity Foundation (IBEF), the Indian food and grocery market is the sixth-largest globally, with retail accounting for 70% of sales. The Indian food processing industry accounted for 32% of the country's overall food market, ranking sixth in production, consumption, export, and expected growth.

Food Service Packaging Industry Overview

The foodservice packaging market is fragmented, as many players have a strong presence due to their offerings. With innovations and demand, the market is attractive for new players.

- September 2023: Berry introduced food-grade recycled content in flexible plastic packaging with food-grade low-density polyethylene (LLDPE) films containing at least 30% (PCR) post-consumer recycled plastic. Through this addition to its robust film portfolio, Berry offered brands a solution to their sustainability commitments to include PCR in food packaging.

- February 2023: Pactiv Evergreen collaborated with AmSty to launch Circular Polystyrene Food Packaging Products, where Pactiv Evergreen packaging will use ISCC PLUS-certified recycled polystyrene from AmSty, and Evergreen will begin offering customers the ability to purchase packaging linked to ISCC PLUS-certified post-consumer recycled polystyrene derived from advanced recycling technologies using mass balance allocation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand For Convenience Food Continues In Major Markets

- 5.1.2 Increasing Vendor Focus On Recycled Plastic Due To Emphasis On Sustainability

- 5.2 Market Challenges

- 5.2.1 Steady Growth Of Flexible Packaging Due To Environmental Pressure And Uncertainty In Polymer Prices

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Corrugated Boxes And Cartons

- 6.1.2 Plastic Bottles

- 6.1.3 Trays, Plates, Food Containers, And Bowls

- 6.1.4 Cups And Lids

- 6.1.5 Clamshells

- 6.1.6 Other Product Types

- 6.2 By End-user Industries

- 6.2.1 Quick Service Restaurants (QSR)

- 6.2.2 Full-service Restaurants (FSR)

- 6.2.3 Institutional

- 6.2.4 Hospitality (Dine-ins, Coffee & Snack, Etc.)

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Australia and New Zealand

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.5 Middle East and Africa

- 6.3.5.1 Saudi Arabia

- 6.3.5.2 United Arab Emirates

- 6.3.5.3 South Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Pactiv Evergreen Inc.

- 7.1.2 Dart Container Corporation

- 7.1.3 Amhil North America

- 7.1.4 Genpak LLC

- 7.1.5 Huhtamaki Oyj

- 7.1.6 Berry Global Inc.

- 7.1.7 Novolex Holdings LLC

- 7.1.8 Sabert Corporation

- 7.1.9 Silgan Plastic Food Container

- 7.1.10 B&R Plastics Inc.

- 7.1.11 Graphic Packaging International Inc.

- 7.1.12 Amcor PLC

- 7.1.13 Sonoco Products Company