|

市場調査レポート

商品コード

1850209

農薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月29日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

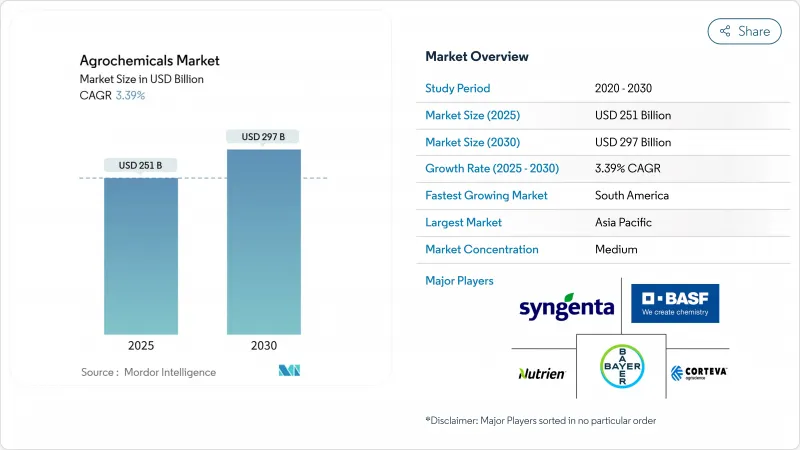

農薬市場は、2025年に2,510億米ドルに達し、2030年には2,970億米ドルに増加すると予測され、CAGRは3.39%と堅調です。

成長を支えているのは、大規模穀物経済圏における持続的な肥料需要、生物学的作物保護製品の急速な普及、投入資材の使用効率を高める精密農業ツールの普及です。同時に、2030年までに化学農薬の使用量を半減させるというEUのFarm to Fork指令、中国の定期的な肥料輸出抑制、主要輸入市場での残留規制の強化により、生産者は低毒性化学物質やデジタル・アドバイザリー・サービスへのポートフォリオ・シフトを加速せざるを得なくなっています。生物学的製剤は、現在30カ国で実施されている農薬税制や、ブラジルとインドの登録経路の合理化を背景に急速に規模を拡大しており、一方、新規作用モードを持つ高級除草剤は、コストのかかる耐性雑草の増加に対処しています。ジェネリック医薬品が成熟分子のマージンを侵食し、新たな「インプット・アズ・ア・サービス」モデルが製品量よりも成果ベースの価格設定に報いるにつれて競合の激しさは増しており、農薬市場において技術統合と持続可能性の証明によって定義される10年の舞台が整いつつあります。

世界の農薬市場の動向と洞察

除草剤耐性雑草の増加がプレミアム除草剤需要に拍車をかける

除草剤抵抗性の雑草は、現在世界中で2億7,000万エーカー以上に蔓延しており、生産者は新しい作用モードを持つプレミアム除草剤を求めています。FMCのドダイレックス・アクティブは、30年ぶりの新しい除草剤モードで、ペルーで初登録され、イネの抵抗性イネ科雑草を対象としており、2025年8月に商業販売が開始される予定です。米国環境保護庁の2024年抵抗性管理枠組みは、総合的な雑草管理プロトコルを強化し、革新的な製剤に規制上の支援を与えるものです。住友化学のアルゼンチンでのラピディシル登録は、不耕起システムに対応するための競争争を下支えし、保全耕起除草剤による年間売上高1,000億円(6億5,000万米ドル)を目指します。抵抗性雑草は世界全体で年間150億米ドルを超える収量損失をもたらすため、生産者の支払い意欲は依然として強いです。

AIを活用したインプット・アズ・ア・サービス・ビジネスモデルの融合

デジタル農業プラットフォームは、農学的アドバイス、可変レート処方、成果ベースの保証をバンドルすることで、従来の製品のみの流通に取って代わりつつあります。バイエルのCROPWISEプラットフォームは現在、圃場センサー、気象データ、衛星画像を統合し、散布と施肥のスケジュールを微調整しています。BASFとAgmatixは、機械学習による診断を応用して、大豆シスト線虫のストレスが目に見える症状が出る前に検出し、収量を守りながら薬剤負荷を削減します。シンジェンタとタラニスの提携は、小売業者にAIを活用したスカウティングを提供し、的確な投入資材の配置を促し、1回限りの売上を定期収入に変えます。これらのサービスにより、1エーカー当たりの化学物質使用量を最大20%削減し、農薬市場における持続可能性の要請と収益性を一致させることができます。

EU、ブラジル、中国における高毒性農薬の段階的廃止の加速

規制当局は、毒性が指摘された有効成分の猶予期間を短縮し、メーカーに在庫の償却と改良パイプラインの加速を迫っています。欧州連合(EU)の最新の提案は、影響を受けやすい生息地から特定の有機リン酸塩を排除するもので、ブラジルはEUと承認基準を合わせ、2026年までに約200のレガシー分子を排除します。BASFは2024年にグルホシネート工場を閉鎖し、規制強化の見通しに関連して減損損失を計上しました。中国の政策は低毒性殺菌剤と生物農薬を優先し、2025年までに9万トンの商業生産量を見込んでいます。

セグメント分析

農薬市場の2024年の売上高の46.0%を肥料が占めたが、これは穀物や油糧種子への大栄養素の供給において不可欠な役割を担っていることを反映しています。しかし、不安定な天然ガス価格はアンモニアコストを高騰させ、窒素生産者のマージンを圧迫し、ウレアーゼ阻害剤や、収量を落とすことなく散布量を15~25%削減する放出制御型コーティング剤などの効率化技術に軸足を移す兆しを見せています。肥料の農薬市場規模は、新興経済諸国における施用率の頭打ちにより、市場全体よりも鈍いCAGR 2.3%で拡大すると予測されます。そのため生産者は、プレミアムポリマーコーティング製品や、炭素クレジットに連動した製品など、数量以上の価値を獲得できる製品を重視しています。

微生物、植物、フェロモン、生化学を含む生物学的セグメントは、2024年に14.7%成長し、2030年には250億米ドルに達すると予測されます。その中で、バイオ殺虫剤の農薬市場規模は、欧州の残留規制強化やブラジルのファスト・トラック登録に後押しされ、CAGR 15.2%で拡大する見通しです。その結果、総合的な害虫管理プログラムでは、化学的手法と生物学的手法が1シーズンごとにローテーションされるようになり、サプライヤーは独自の系統やアジュバントを相互販売できるようになりました。シンジェンタ・バイオロジカルズやFMCといった大手企業は、この分野に積極的に軸足を置き、ポートフォリオのギャップを埋めるためにM&Aを加速させています。除草剤、殺菌剤、アジュバント、植物成長調整剤は依然として重要であり、これらを合わせた農薬市場のシェアは、生物学的製剤がより高いマージンを得ながら販売量をカニバリゼーションするため、わずかに低下すると予測されます。

地域分析

アジア太平洋地域は2024年に最も高い収益を維持し、農薬市場の48.5%を占めました。中国は世界の活性成分生産量の50%を製造しているが、国内の環境規制は現在低毒性ラインを優先しており、生物農薬生産能力への投資を刺激しています。インドの開発・製造受託企業は、欧米のパイプラインのギャップを埋める複数年契約を獲得し、二桁の売上成長を牽引します。日本は排出量目標を達成するために放出制御肥料の採用を加速し、オーストラリアは肥料需要と気候による干ばつ調整のバランスをとる。デジタル土壌検査とバランスの取れた栄養摂取を推進する政府の補助金プログラムは、基本的な消費パターンを強化します。

南米は最も急成長している地域で、2030年までCAGR 4.4%で拡大します。ブラジルのバイオ市場は2024年に50億BRL(10億米ドル)に達し、大豆と綿花に集中します。物流のボトルネックは依然として残っており、ブラジルの農道の62%は最適品質未満であるため、コストが上昇し、製剤工場の地域化が進んでいます。アルゼンチンの不耕起作付面積は90%を超え、Rapidicilのような残渣対応除草剤の需要を下支えしています。気候変動、特に干ばつは、微量栄養素と水効率製品の売上を押し上げ、農薬市場において適応技術のための弾力的なビジネスケースを形成しています。

北米と欧州は成熟しているもの、依然としてイノベーションの中心地です。米国は、農家のコストを1トン当たり100米ドル上昇させる可能性のあるカナダ産カリの関税提案と戦っており、生物学的窒素置換とカリウム可溶化微生物への関心を促しています。カナダは4R栄養管理認証を推進し、貸し手のインセンティブを肥料のベストプラクティスに結びつけています。欧州のFarm to Fork戦略では、2030年までに農薬を50%削減することが義務付けられており、生物学的認証の加速化とデジタル・トレーサビリティ・システムが推進されています。中東とアフリカはそれぞれ3.4%と4.1%の成長を遂げたが、これは小規模な基盤からではあるもの、ソブリンによる食糧安全保障への投資、水耕栽培の採用、砂漠の再生農法に後押しされたものです。これらの力学を総合すると、農薬市場は、より高価値の製品代替によって補完された緩やかな数量成長の軌道を維持していることになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 除草剤耐性雑草の増加が高級除草剤の需要を刺激

- AIを活用したInput-as-a-Serviceビジネスモデルの融合

- 農薬税制度による生物製剤の急増

- 窒素効率製品の炭素クレジット収益化

- 緩効性肥料の主流化

- 垂直農場と屋内農場における作物の多様化

- 市場抑制要因

- EU、ブラジル、中国における高毒性活性物質の段階的廃止の加速

- 不安定なグリホサート価格が製造業者の利益を圧迫

- 規制データパッケージコストの上昇

- 北米における慢性的なアクティビスト訴訟リスク

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 肥料

- 窒素

- リン酸

- カリウム

- 農薬

- 除草剤

- 殺虫剤

- 殺菌剤

- 生物農薬

- アジュバント

- 植物成長調整剤

- 肥料

- 用途別

- 作物ベース

- 穀物

- 豆類と油糧種子

- 果物と野菜

- 非作物ベース

- 芝生と観賞用芝

- その他非作物ベース

- 作物ベース

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Syngenta Group

- Bayer Crop Science AG

- BASF Agricultural Solutions

- Corteva Agriscience

- Nutrien Ltd

- Yara International ASA

- Mosaic Company

- CF Industries Holdings

- UPL Ltd

- FMC Corporation

- Sumitomo Chemical AgroSolutions

- Nufarm Ltd

- K+S AG

- ICL Group

- OCP Group

- Albaugh LLC

- OCI Global

- RovensaNext

- Bharat Rasayan Ltd

- Helm AG