|

市場調査レポート

商品コード

1851942

アフリカの農薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Africa Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの農薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月13日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

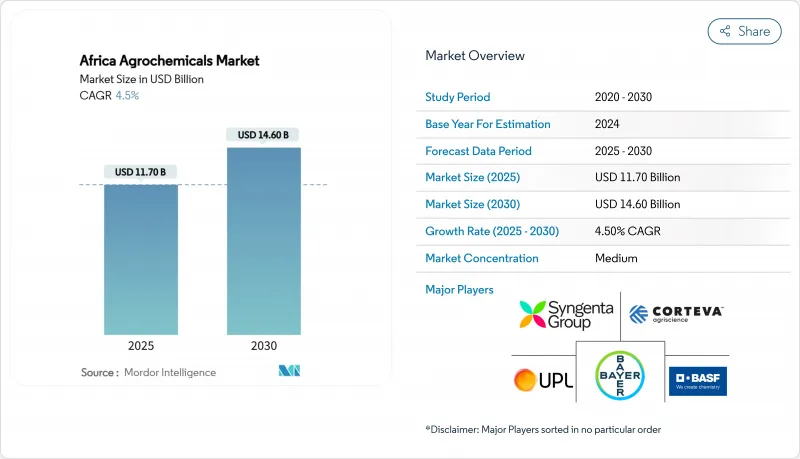

アフリカ農薬の市場規模は2025年に117億米ドルに達し、2030年にはCAGR 4.5%で成長して146億米ドルになると予測されています。

2024年には、アフリカ全域で土壌養分の枯渇が広がっていることを背景に、肥料が51%のシェアを占めて市場を独占しています。植物成長調整剤は、農家が精密な散布方法を採用していることから、CAGR 6.90%と最も高い成長率を示しました。市場の成長を支えているのは、害虫課題の増加、人口拡大による食糧需要の増大、零細農家へのアクセスを改善する政府の補助金制度です。高い投入コストと地域間の一貫性のない規制が、農業の収量格差是正への取り組みを制限しています。市場参入企業は、現地製造施設の設立、革新的な流通網の開発、精密化学ソリューションによる持続可能な製品ラインの構築を進めています。さらに、政府は倉庫受取型融資制度や機械化支援プログラムを拡充しており、これが農薬市場の需要拡大を後押ししています。

アフリカ農薬市場動向と洞察

気候に起因する病害虫の増加

不安定な天候パターンにより、アフリカの複数の国々で秋蚕のような侵入害虫の蔓延が拡大し、トウモロコシの収量に大きな影響を与えています。穀物栽培地域におけるストライガ雑草の蔓延は引き続き収穫に影響を及ぼしており、農家は総合的な化学的防除プログラムを実施するに至っています。ケニア、ガーナ、エチオピアは緊急対応プロトコルを確立し、地域組織は病害虫監視ネットワークを調整しています。農業関連企業は害虫の幼虫を標的にした精密殺虫剤の開発を加速させており、デジタル・モニタリング・プラットフォームは農家にリアルタイムの警報を提供しています。こうした要因がアフリカ農薬市場の持続的成長を後押ししています。この市場は、種子処理剤や農家教育プログラムへの投資を通じて、さらに勢いを増しています。官民パートナーシップは、新しい作物保護ソリューションへの農家のアクセスを改善しています。

加速する人口増加による食糧需要の格差

零細農家が農薬を推奨レベル以下で使用しているため、農業生産性は依然として限定的です。ナイジェリア、エチオピア、タンザニアでは、都市部への移住による大きな制約が発生し、農業労働力が減少しています。政府の取り組みとしては、国内での肥料生産と灌漑インフラへの投資による収量の向上が挙げられます。エチオピアの灌漑拡大プログラムは、低地の生産性向上と輸入依存度の低下に重点を置いています。食糧需要の増大は、肥料、農薬、植物成長調整剤製品のアフリカ農薬市場を引き続き牽引しています。農業ディーラー・ネットワークとモバイル・アドバイザリー・サービスの拡大は、農民の投入資材や知識へのアクセス向上に役立っています。農家は天候の変化に対応するため、気候変動に強い農薬ソリューションを採用するようになっています。

小農には手の届かない高い農薬価格

内陸国では輸送コストが最終小売価格の最大50%を占め、エチオピアでは近年、肥料価格が大幅に上昇しています。ケニアでは、2025年財政法案を通じて農薬に16%の付加価値税を課すことが提案されており、生産コストが大幅に上昇する可能性があります。ナイジェリアでは、2024年半ばに記録的な高水準の食料インフレが発生し、家計は収入の大半を食料に費やさざるを得なくなり、農業投資に使える資金が減少しました。農家はしばしば高金利を請求する非正規金融業者に手を出し、アフリカの農薬市場の成長を制限する負債サイクルを生み出しています。その結果、価格的な問題により、効果的な作物保護製品の導入が減少し、収量が最適化されず、食糧安全保障の課題が続くことになります。

セグメント分析

肥料は2024年のアフリカ農薬市場シェアの51%を占め、広範な土壌養分不足に対処し、さまざまな農業生態学的地帯で農業生産性を支えています。窒素ベースの製剤は穀物生産に不可欠であることに変わりはないが、リン酸肥料とカリ肥料はバランスの取れた栄養プログラムを通じて普及が進んでいます。デジタル補助金電子バウチャーと倉庫受取型クレジット・システムは、経済的障壁を軽減し、タイムリーな施肥を可能にします。

植物成長調整剤はCAGR 6.9%を示し、これはストレス耐性、根の発達、収量の可能性を向上させる栄養素の採用増加によるものです。農薬はアフリカ全域でかなりの量を維持しており、労働力不足と雑草の耐性個体数のために除草剤が優勢です。殺虫剤の需要は気候に関連した害虫の発生に対応して増加し、殺菌剤の使用は園芸地域で拡大します。アジュバントは、精密散布装置が葉の被覆率の向上とタンク混合の簡略化のために高度な製剤を必要とすることから、小さい分野ではあるが重要性を増しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 気候に起因する病害虫圧力の上昇

- 人口増加が加速する食糧需要格差

- 肥料と農薬の導入に対する政府の補助金制度

- 機械化と精密農業技術の導入が投入効率を押し上げる

- 倉庫受入金融の拡大が投入資材の運転資金を解放する

- ラストワンマイル流通を改善するプライベートブランド農産物小売チェーンの出現

- 市場抑制要因

- 小農民には手の届かない高い投入資材価格

- 細分化された厳しい薬事承認スケジュール

- 農家の信頼を損なう偽造農薬の蔓延

- 有機・無残渣輸出作物プログラムによる合成農薬使用の抑制

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 肥料

- 窒素

- リン酸肥料

- カリウム

- 農薬

- 除草剤

- 殺虫剤

- 殺菌剤

- アジュバント

- 植物成長調節剤

- 肥料

- 用途別

- 穀物および穀類

- 豆類と油糧種子

- 果物および野菜

- 商業作物(サトウキビ、綿花、その他)

- 地域別

- エジプト

- モロッコ

- アルジェリア

- ケニア

- タンザニア

- エチオピア

- 南アフリカ

- ザンビア

- ジンバブエ

- ナイジェリア

- ガーナ

- コンゴ民主共和国

- その他アフリカ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Bayer AG

- Syngenta Group

- Corteva Agriscience

- BASF SE

- FMC Corporation

- UPL Limited

- Yara International ASA

- Sumitomo Chemical Co., Ltd.

- Gowan Company(Isagro S.r.l.)

- Rovensa S.A(Partners Group)

- Sasol Limited

- Twiga Chemical Industries Ltd.(AJ Group)

- OCP Group

- Indorama Corporation

- Albaugh LLC