|

市場調査レポート

商品コード

1907334

欧州のペットフード:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のペットフード:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

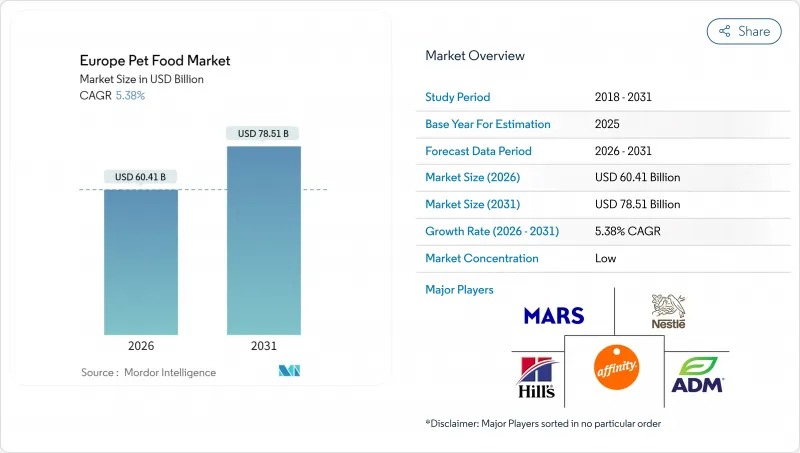

欧州のペットフード市場規模は、2026年に604億1,000万米ドルと推定されております。

これは2025年の573億3,000万米ドルから成長した数値であり、2031年には785億1,000万米ドルに達すると予測されております。2026年から2031年にかけては、CAGR5.38%で成長が見込まれております。

この成長の勢いは、プレミアム化、ペットの人間化、そして単身世帯への人口動態の変化によって支えられており、これらの世帯はコンパニオンアニマルの栄養管理に安定した自由裁量予算を割いています。プロバイオティクス、オメガ脂肪酸、関節サポート複合体などの機能性成分が主流SKU(在庫管理単位)に採用され、高価格帯を重視した価値構成を支えています。欧州の消費者がパーソナライズされた食事を提供する定期購入モデルを採用する中、オンラインおよび消費者直販チャネルが急速に拡大しています。主要メーカーは欧州グリーンディールへの適合と将来を見据えた原材料サプライチェーン構築のため、代替タンパク質への投資を進めています。

欧州のペットフード市場の動向と洞察

プレミアム化とペットのヒューマナイズ化

欧州のペットオーナーは、動物を家族の一員として捉える傾向が強まっており、科学的に裏付けられたプレミアム栄養製品への購買行動が根本的に変化しています。この人間化動向は、パンデミック後のリモートワーク普及により人と動物の絆が深まったことで加速しました。2024年現在、欧州のペットオーナーの73%が、ペットの栄養ニーズを人間の家族と同等と認識しています。この変化は、オーガニック、グレインフリー、獣医師推奨の製品への需要増加に顕著に表れており、プレミアム製品は従来品に比べて40~60%の価格プレミアムを形成しています。欧州消費者が自身の支出を削減してもペットの栄養品質を妥協しない姿勢が、この動向の持続可能性を裏付けています。

増加するペット飼育世帯と単身世帯

欧州では単身世帯が人口構成の変化に伴い増加しており、2024年には全世帯の41.4%を占めました(2010年は32.8%)。この傾向はペットおよび関連栄養製品の持続的な需要を生み出しています。特に都市部では高齢化と家族形成の遅れが相まって、感情的な伴侶としてのペット飼育が顕著です。単身世帯は、他の支出項目が少ないため、ペットケアへの一人当たりの支出額が一般的に高く、ペットフードへの年間平均支出額は複数人世帯よりも35%高くなっています。この動向は、賃貸物件におけるペット飼育の受け入れを促進する欧州の住宅政策によってさらに強化され、従来のペット飼育障壁が取り除かれています。

肉類・穀物原料価格の変動性

2024年以降、肉粉、穀物、特殊原料などの商品価格変動が激化しております。小麦価格は25~30%の変動幅を示し、アフリカ豚熱の発生や気候変動に伴う供給障害により肉粉コストは35~40%急騰しました。こうした原材料コスト上昇圧力は、垂直統合や商品ヘッジ能力を持たない中堅メーカーに特に深刻な影響を与え、利益率圧縮と小売価格引き上げという消費者離れリスクを伴う困難な選択を迫っております。一方、消費者の強い支持を得ているプレミアムブランドは価格決定力が高く、プライベートブランドメーカーは小売業者の支援によりコスト変動の管理が可能となります。しかし、経済不安の中での欧州消費者の価格感応度の高さが課題となり、メーカーがコスト上昇分を完全に転嫁する能力を制限しています。

セグメント分析

2025年時点でフード市場が66.65%のシェアを占め、欧州における総合的な栄養ソリューションへの嗜好が、補助的なおやつやアクセサリーよりも優先されていることを反映しています。この大きなシェアは、ペットフード製品が日々の栄養要求を満たす上で不可欠であるという特性に主に起因しています。このセグメント内では、ドライフードがペットオーナーの好まれる選択肢として浮上しています。その理由は、ウェットフード製品と比較した際の利便性、長期保存性、栄養バランス、コスト効率性にあります。特に利便性と栄養最適化が優先される都市部において、手作り食から市販ペットフード製品への移行が増加していることも、このセグメントの成長をさらに後押ししています。

ペット用栄養補助食品/サプリメントは、ペットの健康意識の高まりと予防栄養戦略に関する獣医師の推奨により、2031年までCAGR7.95%で最も急速に成長する製品セグメントです。このセグメントの拡大は、ペットの総合的な健康と幸福を高めるために、ビタミン、ミネラル、オメガ3脂肪酸、プロバイオティクスを含むサプリメントへの投資が増加しているプレミアム市場で特に顕著です。この成長は、特にペットの健康意識が特に高い英国、ドイツ、フランスなどの国々において、獣医師の推奨やペットケアへのホリスティックなアプローチの普及拡大によってさらに支えられています。

欧州のペットフード市場レポートは、ペットフード製品(フード、ペット用栄養補助食品/サプリメント、ペット用おやつなど)、ペットの種類(猫、犬、その他のペット)、流通チャネル(コンビニエンスストア、オンラインチャネルなど)、地域(フランス、ドイツ、イタリア、オランダなど)ごとにセグメント化されています。市場予測は、金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリーおよび主要な調査結果

第4章 主要業界動向

- ペットの飼育数

- 猫

- 犬

- その他のペット

- ペット関連支出

- 消費者の動向

第5章 供給と生産の動向

- 貿易分析

- 原材料の動向

- バリューチェーン及び流通チャネル分析

- 規制の枠組み

- 市場促進要因

- プレミアム化とペットのヒューマナイズ化

- ペット飼育世帯数および単身世帯の増加

- 電子商取引(Eコマース)およびDTC(消費者直接販売)サブスクリプションの急速な成長

- プライベートブランドの統合による価格競争力の拡大

- 欧州連合(EU)グリーンディールの圧力による代替タンパク質イノベーションの促進

- 獣医療費のインフレが飼い主の予防栄養への意識を高める

- 市場抑制要因

- 肉類・穀物原料価格の変動性

- 欧州連合(EU)の添加物および表示に関する厳格な規制

- カテゴリー3動物性脂肪のバイオ燃料への転用による供給逼迫

- 獣医療費の高騰がペットフードの任意支出を圧迫

第6章 市場規模と成長予測(金額ベース/数量ベース)

- ペットフード製品

- 食品

- サブ製品別

- ドライペットフード

- サブドライペットフード別

- キブル

- その他のドライペットフード

- サブドライペットフード別

- ウェットペットフード

- ドライペットフード

- サブ製品別

- ペット用ニュートラシューティカル/サプリメント

- サブ製品別

- 乳由来バイオアクティブ成分

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質およびペプチド

- ビタミン・ミネラル

- その他のニュートラシューティカルズ

- サブ製品別

- ペット用おやつ

- サブ製品別

- カリカリおやつ

- デンタルおやつ

- フリーズドライおよびジャーキーおやつ

- ソフト&チューイーおやつ

- その他のおやつ

- サブ製品別

- ペット用獣医規定食

- サブ製品別

- 糖尿病

- 消化器系サポート

- 口腔ケア用規定食

- 腎臓

- 尿路疾患

- 肥満用規定食

- 皮膚用規定食

- その他の獣医規定食

- サブ製品別

- 食品

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他の流通チャネル

- 地域

- ドイツ

- フランス

- スペイン

- イタリア

- 英国

- ポーランド

- ロシア

- オランダ

- その他欧州地域

第7章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- ブランドポジショニングマトリックス

- 市場要求分析

- 企業概況

- 企業プロファイル

- Mars, Incorporated

- Nestle(Purina)

- Colgate-Palmolive Company(Hill's Pet Nutrition, Inc.)

- General Mills Inc.

- Affinity Petcare S.A

- Archer Daniels Midland(ADM)

- Clearlake Capital Group, L.P.(Wellness Pet Company, Inc.)

- Schell & Kampeter, Inc.(Diamond Pet Foods)

- Heristo aktiengesellschaft

- Virbac

- Deuerer GmbH

- Partner in Pet Food

- Monge & C. S.p.A.

- Farmina Pet Foods

- Vafo Group