|

市場調査レポート

商品コード

1851536

中国紙包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)China Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国紙包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月03日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

概要

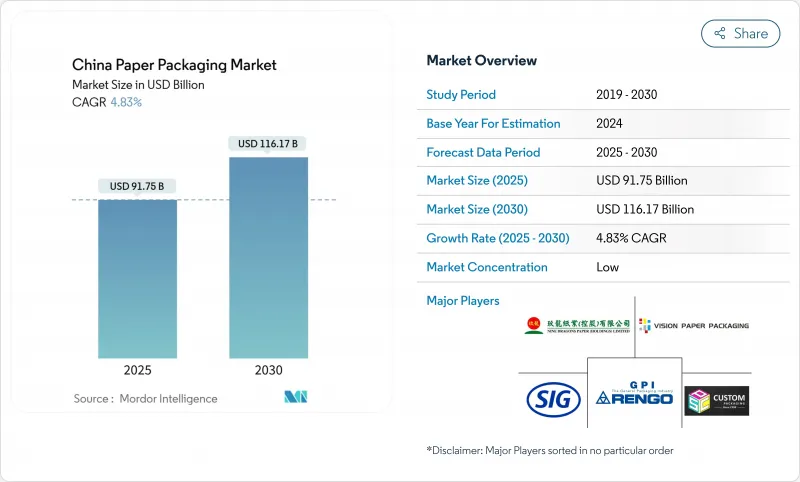

中国紙包装の市場規模は2025年に917億5,000万米ドル、2030年には1,161億7,000万米ドルに達すると予測され、この期間のCAGRは4.83%です。

パルプ価格のサイクルにもかかわらず拡大が続いているのは、eコマースの小包量、政府のプラスチック削減義務、外食産業の成長など、すべての新規需要が段ボールや折りたたみカートンのフォーマットに流れているからです。再生繊維の採用は、中国の国家的な炭素クレジット制度が回収率向上に貢献したメーカーに報いることで加速する一方、先進的なデジタル印刷によって、ブランドは在庫を無駄にすることなく、短期間でカスタマイズされたキャンペーンを実施することができます。ナインドラゴンズペーパーやサンペーパーグループなどの国内大手企業は、高速コルゲーターやボードマシンによって生産能力を拡大していますが、輸入木材繊維やダイナミックな電力価格の変動により、コスト圧力は高いままです。グリーン包装の施行が地方によって異なるため、企業は配合をローカライズし、GB 43352-2023の重金属と規制物質の制限を満たす品質管理システムに投資する必要があります。

中国紙包装市場動向と洞察

eコマース小包取扱量の伸び

エクスプレス便の2024年の取扱個数は1,745億個で、段ボール包装が箱材料の96.17%を占め、中国紙包装市場のベースライン消費の弾力性を確保します。北京と上海の地下鉄ベースの物流ハブは、ラストワンマイルのコストを削減し、配送時間を短縮しているが、複数のハンドリングサイクルに耐えなければならない二次箱の性能要件も強化しています。アリババが試験的に行っている、世界各地への1時間以内の配達を目標としたロケット配送の取り組みは、いかに極限のスピードが、耐衝撃性を維持しながら重量対強度比を最適化するよう包装設計者に迫っているかを例証しています。QRコードのシリアル化とRFIDの挿入は、在庫の可視化と返品の自動化を可能にし、出荷用カートンにますます現れています。これらの市場開拓は、eコマースを中国紙包装市場の構造的バックボーンとして確固たるものにしています。

フードサービスとデリバリーのエコシステムの拡大

持ち帰り注文は、中核的な商業グリッドで高密度の廃棄物を発生させ、上位10%のゾーンが包装廃棄物の64%を占めています。Sumkokaのような国内サプライヤーが開発した再利用可能なバガス成型トレーは、高級フランチャイズの間で人気を博しており、鮮度を追跡するバイオセンサーラベルは、安全性を損なうことなく、より長い配達半径をサポートしています。多国籍のクイックサービス・チェーンは、洗浄可能なダインイン容器を試験的に導入しており、各州の規制当局が使い捨てプラスチックに関する基準値を厳しくする中、将来のコンプライアンスの方向性を示しています。これらの要因が総合的に中国紙包装市場に勢いを与えています。

不安定な古紙輸入規制と原料供給

中国は2023年に市場パルプを2,800万トン輸入するが、これは24%の増加であり、工場は運賃の混乱と関税の変動にさらされます。消費後繊維の輸入禁止により、国内のリサイクル業者はフル稼働に近い状態で操業しているため、古紙価格が上昇し、時にはコンバーターがグラム数を下げざるを得ないこともあります。完成紙の関税引き下げはASEAN工場との競合を激化させ、価格の谷間に国内マージンを侵食します。このような力学により、中国紙包装市場の成長期待は縮小しています。

セグメント分析

段ボール箱は、2024年の中国紙包装市場規模の36.24%を占める。Dongguan Huangshi Jinhuiの毎分352mのコルゲーターは、eコマース拠点へのジャストインタイム供給を確保する能力増強の例です。しかし、化粧品のプレミアム化に後押しされた紙器は、2030年までCAGR7.84%で段ボールの優位性を侵食していくと思われます。マルチパスデジタル印刷機は、ニス効果やスポット箔のアクセントを、長い準備時間を強いることなくサポートし、ブティック美容ラベルが高いマージンを得る限定版を印刷できるようにしています。液体包装用カートンは、SIGのアルミ層を使用しない技術を活用することで、ニッチな関連性を維持しています。改ざん防止スリーブなどの特殊サブラインは、都市部でのヘルスケア支出の増加に伴い、着実に成長しています。

2024年の中国紙包装市場シェアの41.32%は食品です。食事用弁当の密度はグリッドのホットスポットで急上昇し、自治体がリサイクル繊維工場に供給するクローズド・ループ回収を試行するよう促しています。パーソナルケアと化粧品は、規模は小さいもの、オンライン美容インフルエンサーと可処分所得の上昇を背景に、年間8.21%拡大します。Amcorのリサイクル対応パウチと詰め替えポッドは、第1級ショッピングモールのシャンプー詰め替えステーションで使用され、機能性と持続可能性の融合を示しています。エレクトロニクス・ブランドは、帯電防止と防湿ライナーを要求しており、段ボールサプライヤーはフルーティングにナノクレイコーティングをグラフト重ねることで、この有利なクロスオーバーに対応しています。ヘルスケア包装は、温度ロギング用のスマートラベルを統合し、地域のコールドチェーン全体で医薬品の完全性を確保しています。

中国紙包装市場レポートは、製品タイプ(折りたたみカートン、段ボール箱、紙袋と袋、液体包装カートン、その他)、エンドユーザー産業(食品、飲食品、ヘルスケア、パーソナルケア、家庭用品、エレクトロニクス、その他)、材料タイプ(バージン繊維ベース、再生繊維ベース)、包装レベル(一次、二次、三次)、地域(中国)で区分されています。市場予測は金額(米ドル)です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- eコマース小包量の伸び

- フードサービスとデリバリーのエコシステムの拡大

- 政府のプラスチック削減義務、紙を支持

- 先進デジタル印刷とスマートパッケージングの融合

- 国境を越えたeコマースの統合が段ボール需要を押し上げる

- 国の炭素クレジット制度が再生紙利用を加速

- 市場抑制要因

- 不安定な古紙輸入規制と原料供給

- リサイクル可能な単一素材プラスチックとの競合

- 脱炭素化目標の中で上昇するエネルギーコスト

- パルプ価格サイクルと国内木材パルプ不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 中国紙パルプ:海外投資家の投資機会

- ESGと持続可能性への取り組み

第5章 市場規模と成長予測

- 製品タイプ別

- 折りたたみカートン

- 段ボール箱

- 紙袋と袋

- 液体包装用カートン

- その他の製品タイプ

- エンドユーザー業界別

- 食品

- 飲料

- ヘルスケアと医薬品

- パーソナルケアと化粧品

- 家庭用品と洗剤

- 電子・電気製品

- その他のエンドユーザー産業

- 素材タイプ別

- バージン繊維ベース

- 再生繊維ベース

- 包装レベル別

- 一次包装

- 二次梱包

- 三次包装

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Nine Dragons Paper(Holdings)Ltd

- Lee & Man Paper Mfg Ltd

- Shanying International Holdings Co., Ltd

- Dongguan Vision Paper Products Co., Ltd

- Rengo Co., Ltd

- Oji Holdings Corp(China Packaging)

- SIG Combibloc Group

- Shanghai Custom Packaging Co., Ltd

- Xiamen Hexing Packaging & Printing Co., Ltd

- JML Packaging

- Suneco Box Co., Ltd

- Asia Pulp & Paper(APP)Sinar Mas

- Shanghai DE Printed Box

- Mondi Group

- Smurfit WestRock

- International Paper(China)

- Yutong Packaging Technology

- Zhejiang Jingxing Paper

- Guangdong Yizhou Packaging