軟体動物駆除剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Molluscicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 302 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687171

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

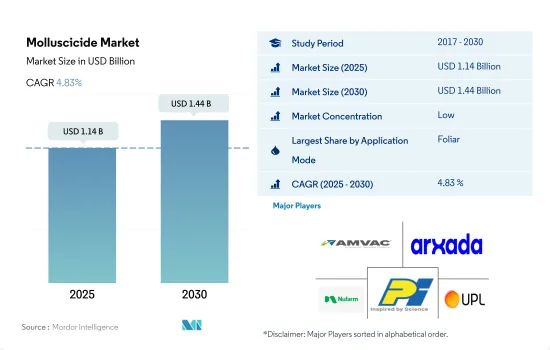

軟体動物駆除剤の市場規模は2025年に11億4,000万米ドルと推定・予測され、2030年には14億4,000万米ドルに達し、予測期間中(2025-2030年)にCAGR 4.83%で成長すると予測されます。

殺軟体動物剤の需要は、カタツムリの増加と農作物損失の増加が原動力となっています。

- 世界的に、軟体動物駆除剤の使用は様々なアプリケーションモードで拡大しています。葉面散布が2022年の軟体動物駆除剤市場全体の53.7%を占め、主要なシェア値を占めています。この分野における軟体動物駆除剤の需要は、特に冬期や雨期にカタツムリの蔓延が増加し、カタツムリやナメクジによる収量の向上と損失の削減が求められていることが背景にあります。

- 土壌処理法における軟体動物駆除剤の需要は、軟体動物駆除剤の土壌処理法の有効性により、予測期間中(2023~2029年)にCAGR 4.8%を記録すると予想されます。土壌処理に使用される軟体動物駆除剤の主な製品は、メタアルデヒド、リン酸鉄、メチオカルブ、エチレンジアミン四酢酸鉄ナトリウム(EDTA)、ニクロサミドです。

- 軟体動物駆除剤市場における化学灌漑分野は、2023年から2029年にかけてCAGR 4.6%で成長すると予測されます。このセグメントの成長は、点滴灌漑システムによる灌漑面積の増加や、これらの作物の水管理を利用したカタツムリやナメクジに対する化学薬品の使用傾向の高まりによるものと考えられます。

- 燻蒸法の市場価値は、予測期間中(2023~2029年)に180万米ドル増加すると予想されます。市場成長は、軟体動物の被害による経済的損失に対する農家や農業専門家の意識の高まりと、燻蒸の採用率の上昇によって刺激されると予想されます。

- したがって、カタツムリの蔓延の増加、灌漑面積の増加、作物損失の増加などの要因が軟体動物駆除剤の需要を促進しています。軟体動物駆除剤の世界市場は、2023年から2029年までの予測期間中にCAGR 4.4%で成長すると予想されています。

南米が軟体動物駆除剤の世界市場を独占

- ナメクジやカタツムリによる農作物被害は、農家への経済的悪影響だけでなく、農作物収量の大幅な損失につながる可能性があります。そのため、カタツムリを標的として作物を被害から守ることができる効果的な軟体動物駆除剤の需要が増加しています。

- 世界の軟体動物駆除剤市場は南米が支配的で、2022年の市場シェアは36.2%でした。南米諸国の農業に影響を与える主なカタツムリには、巨大アフリカカタツムリ(Achatina fulica)や黄金リンゴカタツムリ(Pomacea canaliculata)などがあります。これらの侵入種は旺盛な食欲と急速な繁殖能力で知られ、様々な作物に深刻な脅威を与えています。これらのカタツムリによって引き起こされる収量損失は相当なもので、特に米、トウモロコシ、野菜などの作物が被害を受けやすいです。カタツムリは幼苗や葉、さらには成熟した植物をも食害するため、作物の品質と量の低下につながります。

- 2022年の市場シェアは、アジア太平洋地域が26.0%と第2位でした。アジアでカタツムリ養殖が失敗したのは、カタツムリが生育中の稲作を破壊したためであり、稲作は食料と農業収入の最も重要な供給源と考えられていたため、深刻な経済的影響を引き起こしました。黄金リンゴカタツムリ(Pomacea canaliculata)はアジアの数カ国に導入されたが、予想に反して稲作の害虫に発展しました。ほとんどの農家は、軟体動物駆除剤を含む化学的防除に頼ってきたが、カタツムリの総合的管理手法にも頼ってきました。

- 主要作物におけるカタツムリとナメクジの蔓延の増加は、世界の軟体動物駆除剤市場を牽引し、予測期間中(2023-2029年)のCAGRは4.9%を記録すると予想されます。

世界の軟体動物駆除剤市場の動向

軟体動物駆除剤による作物生産への脅威の増大が使用量を増加させている

- 1ヘクタール当たりの軟体動物駆除剤の世界平均消費量は、2017年の418.0グラム/ヘクタールから2022年には425.5グラム/ヘクタールに増加しました。アジア太平洋地域の1ヘクタール当たりの軟体動物駆除剤消費量は最も多く、2022年には1ヘクタール当たり152.69グラムとなります。国際稲研究所によると、黄金リンゴカタツムリは稲の茎を根元から切断し、株全体を破壊するため、アジア太平洋諸国の稲生産にとって大きな脅威であり、特に灌漑水田では年間収量が最大50%減少するといいます。

- 欧州はヘクタール当たりの消費量が第2位で、2022年には124.32グラム/ヘクタールの殺軟体動物を使用します。南米は、2022年に1ヘクタール当たり110.41グラムの軟体動物駆除剤を使用する、ヘクタール当たり第3位の消費国です。巨大アフリカカタツムリ(Achatina fulica)とゴールデンアップルカタツムリ(Pomacea canaliculata)は、旺盛な食欲と急速な繁殖能力で知られる外来種で、さまざまな作物に深刻な脅威を与えています。これらのカタツムリによる収穫量の損失は相当なもので、米、トウモロコシ、野菜などの作物は特に被害を受けやすいです。

- 北米では土地1ヘクタール当たり37.2グラムの軟体動物駆除剤を消費しており、これは他地域に比べてかなり少ないです。しかし、Deroceras reticulatumは米国でトウモロコシとダイズに最も侵入するナメクジの一種です。トウモロコシやダイズがナメクジによって落葉されると、生育後期にキャノピーの発達が遅れ、収量が低下します。このような攻撃は、軟体動物駆除剤の使用を含む効果的な管理の必要性を求めています。

畑作物や園芸作物など、さまざまな作物におけるカタツムリやナメクジの防除にメタアルデヒドが有効であることから、メタアルデヒドの価格が上昇する可能性があります。

- 軟体動物駆除剤は、農作物や観賞植物に大きな被害を与えるカタツムリやナメクジのような軟体動物を効果的に駆除するために、農業や園芸において不可欠です。これらの殺虫剤は、植物の健康を守り、収穫量の損失を防ぎ、庭園や景観の美観を保つ上で重要な役割を果たしています。

- メタアルデヒドはアルデヒド類に属する軟体動物駆除剤です。農作物や園芸作物の一般的害虫であるカタツムリやナメクジの駆除に広く使用されています。2022年の価格はトン当たり5万2,500米ドルでした。メタルアルデヒドは、一般的な園芸カタツムリ、灰色野ナメクジ、黒色野ナメクジなど、様々な種類のカタツムリやナメクジを効果的に駆除します。

- これらの軟体動物は、野菜、果実、観賞用植物、畑作物など、幅広い作物に大きな被害を与える可能性があります。軟体動物殺虫剤としてのメタアルデヒドの作用機序は、カタツムリやナメクジの活動亢進と協調性の喪失を誘発することです。摂取されると、メタアルデヒドは神経系を混乱させ、動きが活発になり、適切な摂食能力が失われます。その結果、最終的に害虫は脱水症状を起こし、メタルアルデヒドの影響に屈することになります。

- リン酸第二鉄は軟体動物駆除剤で、農業や園芸の現場でカタツムリやナメクジの駆除に使用されます。リン酸鉄としても知られ、天然に存在する化合物です。2022年の価格はトン当たり5万2,000米ドルでした。

- リン酸第二鉄は、一般的な園芸用カタツムリ、灰色野ナメクジ、黒色野ナメクジなど、さまざまな種類のカタツムリやナメクジを効果的に駆除します。これらの軟体動物は一般的な害虫であり、農作物、野菜、果物、観賞用植物、その他様々な栽培植物に被害を与える可能性があります。

軟体動物駆除剤産業の概要

軟体動物駆除剤市場は細分化されており、上位5社で23.27%を占めています。この市場の主要企業は以下の通りです。 American Vanguard Corporation, Arxada, Nufarm Ltd, PI Industries and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- スペイン

- タイ

- ウクライナ

- 英国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- American Vanguard Corporation

- Arxada

- Liphatech Inc.

- Mitsui & Co. Ltd(Certis Belchim)

- Nufarm Ltd

- PI Industries

- UPL Limited

- W. Neudorff GmbH KG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 55939

The Molluscicide Market size is estimated at 1.14 billion USD in 2025, and is expected to reach 1.44 billion USD by 2030, growing at a CAGR of 4.83% during the forecast period (2025-2030).

The demand for molluscicide is driven by increasing snail infestation and rising crop losses

- Globally, the use of molluscicide is expanding in various application modes. Foliar holds the major share value, accounting for 53.7% of the total molluscicide market in 2022. Demand for molluscicides in this segment is driven by increased snail infestation, particularly during the winter and rainy periods, and a need to improve yields and reduce losses due to snails and slugs.

- The demand for molluscicide chemicals in soil treatment methods is expected to register a CAGR of 4.8% during the forecast period (2023-2029) due to the effectiveness of the soil treatment method for molluscicides. The main molluscicide products used for the treatment of soil are metaldehyde, iron phosphate, methiocarb, sodium ferric ethylenediaminetetraacetic acid (EDTA), and niclosamide.

- The chemigation segment in the molluscicide market is expected to grow at 4.6% CAGR from 2023 to 2029. The growth of this segment can be attributed to an increased area under drip irrigation systems, as well as a growing trend of the use of chemicals against snails or slugs using water management on these crops.

- The fumigation method's market value is expected to increase by USD 1.8 million during the forecast period (2023-2029). The market growth is expected to be stimulated by a growing awareness of the economic losses from mollusk damage in farmers and agricultural professionals, as well as the rising adoption of fumigation.

- Therefore, factors such as rising snail infestation, the growing area under irrigation, and increasing crop losses are driving the demand for molluscicide. The global molluscicide market is expected to grow at 4.4% CAGR during the forecast period from 2023 to 2029.

South America dominated the global molluscicide market

- Crop damage caused by slugs and snails can lead to a significant loss in crop yield as well as a negative economic impact on farmers. Consequently, the demand for effective molluscicides that are capable of targeting snails and protecting crops from damage is increasing.

- South America dominated the global molluscicide market, accounting for a market share of 36.2% in 2022. Some of the major snails that affect agriculture in South American countries include the giant African snail ( Achatina fulica) and the golden apple snail ( Pomacea canaliculata). These invasive species are known for their voracious appetite and ability to rapidly reproduce, posing a serious threat to various crops. The yield losses caused by these snails can be substantial, with crops like rice, corn, and vegetables being particularly vulnerable. The snails feed on young seedlings, foliage, and even mature plants, leading to reduced crop quality and quantity.

- Asia-Pacific accounted for the second-largest market share of 26.0% in 2022. Snail farming failed in Asia because snails were destroying the growing rice crops, which caused them severe economic consequences as rice farms were considered their most significant source of food and farm income. The golden apple snail, Pomacea canaliculata, had been introduced to several Asian countries, where it unexpectedly developed into a pest for rice crops. Most farmers have resorted to chemical control, which includes the use of molluscicides, and have also resorted to integrated snail management practices.

- The increasing snail and slug infestations in major crops will drive the molluscicides market globally, which is anticipated to register a CAGR of 4.9% during the forecast period (2023-2029).

Global Molluscicide Market Trends

Increasing threat to crop production due to molluscicides is increasing the usage

- The global average consumption of molluscicides per hectare increased from 418.0 grams per hectare in 2017 to 425.5 grams per hectare in 2022. Asia-Pacific recorded the highest per-hectare consumption of molluscicides, with 152.69 grams per hectare in 2022. Golden apple snails are the major threat to rice production in Asia-Pacific countries as they cut the rice stem at the base, destroying the whole plant and leading to annual yield losses of up to 50%, especially in irrigated rice fields, according to the International Rice Research Institute.

- Europe is the second-largest per-hectare consumer, with 124.32 grams per hectare of molluscicides in 2022. South America is the third-largest per-hectare consumer of molluscicides, with 110.41 grams per hectare of land in 2022. The giant African snail ( Achatina fulica) and the golden apple snail ( Pomacea canaliculata) are invasive species known for their voracious appetite and ability to reproduce rapidly, posing a serious threat to various crops. The yield losses caused by these snails can be substantial, with crops like rice, corn, and vegetables being particularly vulnerable.

- North America consumed 37.2 grams of molluscicides per hectare of land, which is significantly less compared to other regions. However, Deroceras reticulatum is one of the most invasive slug species of maize and soybean in the United States. At later growth stages, corn and soybean defoliation by slugs can lead to delayed canopy development and subsequent lower yields. Such attacks call for the need for effective management, which includes the use of molluscicides.

Effectiveness of the metaldehyde in controlling snails and slugs in various crops like field crops and horticultural crops may increase the price of it

- Molluscicides are essential in agriculture and horticulture for effectively controlling mollusks like snails and slugs, which can cause significant damage to crop and ornamental plants. These pesticides play a vital role in protecting plant health, preventing yield losses, and maintaining the aesthetic appeal of gardens and landscapes.

- Metaldehyde is a molluscicide belonging to the chemical class of aldehydes. It is widely used to control snails and slugs, which are common pests in agricultural and horticultural crops. It was priced at USD 52.5 thousand per metric ton in 2022. Metaldehyde effectively controls a variety of snail and slug species, including common garden snails, grey field slugs, and black field slugs.

- These mollusks can cause significant damage to a wide range of crops, including vegetables, fruits, ornamental plants, and field crops. The mode of action of metaldehyde as a molluscicide involves inducing hyperactivity and loss of coordination in snails and slugs. When ingested, metaldehyde disrupts their nervous systems, leading to increased movement and a loss of their ability to feed properly. This eventually results in the pests becoming dehydrated and succumbing to the effects of metaldehyde.

- Ferric phosphate is a molluscicide used to control snails and slugs in agricultural and horticultural settings. It is also known as iron phosphate and is a naturally occurring compound. It was priced at USD 52.0 thousand per metric ton in 2022.

- Ferric phosphate effectively controls a variety of snail and slug species, including common garden snails, grey field slugs, and black field slugs. These mollusks are common pests that can cause damage to crops, vegetables, fruits, ornamental plants, and various other cultivated plants.

Molluscicide Industry Overview

The Molluscicide Market is fragmented, with the top five companies occupying 23.27%. The major players in this market are American Vanguard Corporation, Arxada, Nufarm Ltd, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 France

- 4.3.4 Germany

- 4.3.5 India

- 4.3.6 Indonesia

- 4.3.7 Italy

- 4.3.8 Japan

- 4.3.9 Myanmar

- 4.3.10 Netherlands

- 4.3.11 Pakistan

- 4.3.12 Philippines

- 4.3.13 Russia

- 4.3.14 Spain

- 4.3.15 Thailand

- 4.3.16 Ukraine

- 4.3.17 United Kingdom

- 4.3.18 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 American Vanguard Corporation

- 6.4.2 Arxada

- 6.4.3 Liphatech Inc.

- 6.4.4 Mitsui & Co. Ltd (Certis Belchim)

- 6.4.5 Nufarm Ltd

- 6.4.6 PI Industries

- 6.4.7 UPL Limited

- 6.4.8 W. Neudorff GmbH KG

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

軟体動物駆除剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 302 Pages

- 納期

- 2~3営業日