アジア太平洋の軟体動物駆除剤市場:市場シェア分析、産業動向、成長予測(2025~2030年)

Asia Pacific Molluscicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 196 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683092

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

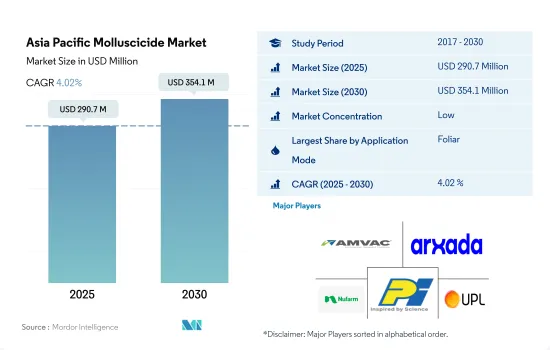

アジア太平洋の軟体動物駆除剤市場規模は、2025年には2億9,070万米ドルと推定され、2030年には3億5,410万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは4.02%で成長する見込みです。

葉面散布は即効性があるため、軟体動物駆除剤の用途で優位を占める

- ナメクジやカタツムリは、ほとんどの作物や多くの雑草を含む広葉植物や草を幅広く食べる。苗を枯らしたり、苗立ちを悪くしたり、若い植物の葉を傷つけたりして作物に害を与えます。したがって、ナメクジの管理は、影響を受けやすい作物の収量を向上させるために最も重要です。アジア太平洋の軟体動物駆除剤市場は、2022年に2億5,630万米ドルと評価され、予測期間終了時には3億4,360万米ドルに達すると予測されています。

- 茶色の庭カタツムリ、巨大アフリカカタツムリ、田んぼナメクジ、中国ナメクジ、キールバックナメクジは、アジア太平洋の作物生産に重大な課題をもたらす可能性のある主要なナメクジとカタツムリの種の一部です。メタアルデヒド、リン酸鉄、メチオカルブ、第二鉄EDTAナトリウムが一般的に使用される軟体動物駆除剤です。

- 軟体動物駆除剤はさまざまな方法で散布することができます。アジア太平洋では、葉面散布が軟体動物駆除剤の散布において優位を占めており、2022年には54.8%の最大市場シェアを占めます。葉面散布の軟体動物駆除剤は、軟体動物の個体数を迅速に制御することができます。軟体動物駆除剤を葉に散布すると、害虫が軟体動物駆除剤に接触することで容易に吸収されます。これにより、急速に死滅させることができます。

- 2022年のアジア太平洋の軟体動物駆除剤市場では、土壌処理が30.4%と第2位の市場シェアを占めています。カタツムリやナメクジに対する安定性、付着性、誘引性を向上させた湿潤性の高い粉末、顆粒、ベイト剤の開発における最近の動向が土壌処理を牽引します。市場は予測期間(2023~2029年)にCAGR 4.1%を記録すると予測されます。

稲などの主要作物における軟体動物駆除剤のニーズの増加が市場を牽引

- アジア太平洋の軟体動物駆除剤市場は、過去期間中に着実な成長を遂げ、2022年には世界の軟体動物駆除剤市場において金額ベースで26.0%と2番目に高いシェアを占めるに至りました。

- アジアでは、カタツムリが生育中の稲作を破壊し、稲作がこの地域の主要な食糧と収入源であることから深刻な経済的損失を引き起こしたため、カタツムリ養殖が失敗しました。ゴールデンAppleカタツムリ(Pomacea canaliculata)はアジア諸国に導入され、予想外に稲の害虫に発展しました。ほとんどの農業従事者は、軟体動物駆除剤の使用を含む化学的防除に頼っており、カタツムリの総合的な管理方法を採用しています。

- コメはアジア全域で圧倒的に重要な作物であり、世界の生産と消費の90%がこの地域で行われています。アジア太平洋は米のような主食用穀物の最大の輸出国・生産国であるため、軟体動物駆除剤はアジア太平洋の穀物・穀類に多く使用されています。このセグメントは2022年に金額ベースで55.5%のシェアを占めています。

- 同様に、果物作物に対する軟体動物の攻撃もこの地域で増加しており、農業従事者が作物を保護するために化学的防除方法を採用するに至っています。果物・野菜は2022年に金額ベースで17.5%のシェアを占めました。

- 同地域では防除戦略が急務であるが、研究者は、農業従事者が軟体動物駆除剤の適切な散布戦略を採用するにはカタツムリの生態に関する正しい知識を持つ必要があると指摘しています。同時に、各国政府による取り組みやメーカーによる技術革新により、同地域の軟体動物駆除剤市場は予測期間中(2023~2029年)にCAGR 4.2%で成長すると見込まれています。

アジア太平洋の軟体動物駆除剤市場動向

軟体動物の個体数の増加がヘクタール当たりの散布量の増加につながる

- 軟体動物駆除剤のヘクタール当たり消費量は日本が最大で、2022年には100.0グラムとなります。カタツムリは日本では幅広い作物を食害する一般的な害虫です。しかし、外来種であるリンゴカタツムリは、日本、特に九州の稲作に大きな脅威をもたらしています。リンゴカタツムリは、稲作における直播栽培の導入の大きな障害となっていると考えられています。この問題に対処するため、農業従事者による軟体動物駆除剤や忌避剤の使用が増加しており、リンゴカタツムリの侵入による影響を軽減する効果的な戦略であることが証明されています。

- オーストラリアは、アジア太平洋で1ヘクタール当たりの軟体動物駆除剤の使用量が圧倒的に多く、2022年には1ヘクタール当たり13.2グラムを使用しています。アフリカオオカタツムリ(Lissachatina fulica)は、急速に繁殖し、農作物、観賞用植物、自生植物を含むさまざまな植物を食べることから、オーストラリアでは主要害虫とみなされています。食欲旺盛で、庭園や農作物、自然生息地に大きな被害を与え、深刻な経済的損失につながります。

- 2022年に軟体動物駆除剤を使用している国は、フィリピン、ベトナム、中国がそれぞれ1ヘクタールあたり9.9グラム、8.4グラム、7.1グラムと突出しています。国際稲ラボによると、ゴールデンAppleカタツムリは稲の茎を根元から切断し、株全体を破壊するため、これらの国々では稲生産にとって大きな脅威となっており、特に灌漑水田では年間収量が最大50%減少するといいます。

- イヌリンゴカタツムリのようなカタツムリの仲間は成長が早く、繁殖も早いため、防除が非常に難しく、アジア太平洋諸国では軟体動物駆除剤の使用量が増加しています。

この市場の主要促進要因としては、農薬の採用が増加していること、アジアの水田でイヌリンゴカタツムリが蔓延していることなどが挙げられます。

- ナメクジは通常、土壌表面の上下で食害し、種子、新芽、根にダメージを与えます。作物によっては、植え付け時に主要問題が発生するものもあれば、生育期や収穫時に問題が発生するものもあります。これらの軟体動物タイプは、農業に莫大な損失をもたらす大きな脅威のひとつとなっています。これらの種は主に小麦、大麦、オート麦などの穀類や園芸作物で見られます。Deroceras、Milax、Tandonia、Limax、Arionは、農作物に経済的損失をもたらす重要な軟体動物として認識されています。

- メタルアルデヒドは軟体動物駆除剤として、畑、庭、温室で様々な野菜や作物に使用されています。ナメクジやカタツムリを殺すために、液体、顆粒、散布、粉塵、ペレット状/粒状の餌の形で散布されます。メタルアルデヒドは2022年に1トン当たり5万2,500米ドルと評価されました。

- リン酸鉄は、穀物、ナタネ、ジャガイモ、幅広い園芸作物に使用される軟体動物駆除剤であり、2022年には1トン当たり5万2,000米ドルと評価されました。リン酸鉄はナメクジ内のカルシウム代謝を阻害し、最終的にナメクジの作物と肝膵臓に細胞病理学的変化を引き起こします。この摂食から死滅までのプロセスは、通常約3~6日かかります。

- この市場の主要促進要因としては、農薬採用の増加、高付加価値園芸作物に対する需要の高まり、アジアの水田におけるゴールデンAppleカタツムリの蔓延などが挙げられます。さらに、農業従事者の軟体動物駆除に対する意識の高まりや、革新的な軟体動物駆除剤の導入は、予測期間中にこの市場に成長機会をもたらすと期待されています。

アジア太平洋の軟体動物駆除剤産業概要

アジア太平洋の軟体動物駆除剤市場は細分化されており、上位5社で14.89%を占めています。この市場の主要企業は、American Vanguard Corporation、Arxada、Nufarm Ltd、PI Industries、UPL Limitedです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- アプリケーションモード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- American Vanguard Corporation

- Arxada

- Nufarm Ltd

- PI Industries

- UPL Limited

- Zagro

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 47094

The Asia Pacific Molluscicide Market size is estimated at 290.7 million USD in 2025, and is expected to reach 354.1 million USD by 2030, growing at a CAGR of 4.02% during the forecast period (2025-2030).

Foliar application dominates molluscicide applications owing to its quick action

- Slugs and snails eat a wide array of broadleaf plants and grasses, including most crops and many weeds. They harm crops by killing seedlings, causing poor stands, and damaging leaves on young plants. Hence, the management of slugs is of utmost importance to get better yields in the susceptible crops. The Asia-Pacific molluscicide market was valued at USD 256.3 million in 2022 and is anticipated to reach USD 343.6 million by the end of the forecast period.

- Brown garden snails, giant African snails, rice field slugs, Chinese slugs, and keelback slugs are some of the major slug and snail species that can pose significant challenges to crop production in Asia-Pacific. Metaldehyde, iron phosphate, methiocarb, and sodium ferric EDTA are commonly used molluscicides.

- Molluscicides can be applied through different methods. In Asia-Pacific, foliar application dominated in molluscicide application, accounting for the largest market share of 54.8% in 2022. Foliar-applied molluscicides can provide quick control of mollusk populations. When sprayed onto the foliage, the molluscicides can be readily absorbed by the pests as they come into contact with it. This can lead to rapid mortality.

- Soil treatment accounted for the second largest market share of 30.4% of the Asia-Pacific molluscicide market in 2022. Recent advances in the development of enhanced wettable powders, granules, and bait formulations with improved stability, adherence, and attractiveness to snails and slugs will drive the soil treatment. The market is anticipated to register a CAGR of 4.1% during the forecast period (2023-2029).

Increased need for molluscicides in major crops like rice is driving the market

- The molluscicides market in Asia-Pacific witnessed steady growth during the historical period, with the region occupying the second-highest share of 26.0% by value of the global molluscicide market in 2022.

- Snail farming failed in Asia as snails destroyed the growing rice crops, causing severe economic losses as rice farms are the region's major source of food and income. The golden apple snail, Pomacea canaliculata, has been introduced to several Asian countries, where it has unexpectedly developed into a rice pest. Most farmers have resorted to chemical control, including the use of molluscicides, and have adopted integrated snail management practices.

- Rice is by far the most important crop throughout Asia, where 90% of the world's production and consumption occurs in this region. Molluscicides are mostly used in grains and cereals in Asia-Pacific as the region is the largest exporter and producer of staple grains such as rice. The segment occupied a share of 55.5% by value in 2022.

- Similarly, mollusk attacks on fruit crops have also been on the rise in the region, leading to farmers adopting chemical control methods to protect their crops. Fruits and vegetables occupied a share of 17.5% by value in 2022.

- Although control strategies are urgently needed in the region, researchers have suggested that farmers must have a sound knowledge of the ecology of snails to adopt the right application strategy for molluscicides. At the same time, initiatives by governments of various countries and innovations by manufacturers are expected to drive the molluscicide market in the region at a CAGR of 4.2% during the forecast period (2023-2029).

Asia Pacific Molluscicide Market Trends

The increasing mollusk population is leading to higher application per hectare

- Japan is the largest per hectare consumer of molluscicides, with 100.0 grams in 2022. Snails are common pests that feed on a wide range of crops in Japan. However, the apple snail, an invasive species, poses a significant threat to rice cultivation in Japan, particularly in Kyushu. It is considered a major hindrance to the adoption of direct-sowing practices in rice farming. To address this problem, the use of molluscicides and repellents by farmers has increased and proven to be an effective strategy in mitigating the impact caused by the apple snail invasion.

- Australia is by far the second-highest per hectare consumer of molluscicides in Asia-Pacific, with 13.2 grams per hectare in 2022. African giant snail (Lissachatina fulica) is considered a major pest in Australia due to its ability to reproduce rapidly and feed on a wide range of plants, including crops, ornamental plants, and native vegetation. It has a voracious appetite and can cause significant damage to gardens, crops, and natural habitats, leading to severe economic losses.

- The Philippines, Vietnam, and China were other prominent countries using molluscicides at the rate of 9.9 grams, 8.4 grams, and 7.1 grams per hectare, respectively, in 2022. Golden apple snails are the major threat to rice production in these countries as they cut the rice stem at the base, destroying the whole plant and leading to annual yield losses of up to 50%, especially in irrigated rice fields, according to the International Rice Research Institute.

- Few of the snail species like golden apple snails can grow and reproduce quickly, making it very difficult to control, leading to higher usage of molluscicides in the countries of Asia-Pacific.

The major drivers for this market include the increasing adoption of agrochemicals and the infestation of golden apple snails in the rice fields of Asia

- Slugs usually feed above and below the soil surface, damaging seeds, shoots, and roots. In some crops, the main problem time is at planting, while in others, problems occur during the growing season or harvest. These mollusk species have become one of the major threats causing huge agricultural losses. These species are majorly seen in cereal crops such as wheat, barley, oats, and horticultural crops. Deroceras, Milax, Tandonia, Limax, and Arion are recognized as important mollusks causing economic losses in the crops.

- Metaldehyde is a molluscicide used in a variety of vegetables and crops in fields, gardens, and greenhouses. It is applied in the form of liquid, granules, sprays, dust, or pelleted/grain bait to kill slugs and snails. Metaldehyde was valued at USD 52.5 thousand per metric ton in 2022.

- Ferric phosphate is a molluscicide for use in cereals, oilseed rape, potatoes, and a wide range of horticultural crops and was valued at USD 52.0 thousand per metric ton in 2022. Iron phosphate interferes with the calcium metabolism within the slug and eventually causes cellular pathological changes in the slug's crop and hepatopancreas. This process from feeding to dying normally takes about three to six days.

- The major drivers for this market include increasing adoption of agrochemicals, rising demand for high-value horticulture crops, and infestation of golden apple snails in the rice fields of Asia. Further, increasing awareness of mollusk control among farmers and the introduction of innovative molluscicide products are expected to create growth opportunities for this market during the forecast period.

Asia Pacific Molluscicide Industry Overview

The Asia Pacific Molluscicide Market is fragmented, with the top five companies occupying 14.89%. The major players in this market are American Vanguard Corporation, Arxada, Nufarm Ltd, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 American Vanguard Corporation

- 6.4.2 Arxada

- 6.4.3 Nufarm Ltd

- 6.4.4 PI Industries

- 6.4.5 UPL Limited

- 6.4.6 Zagro

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋の軟体動物駆除剤市場:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 196 Pages

- 納期

- 2~3営業日