|

市場調査レポート

商品コード

1907289

板紙包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 板紙包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

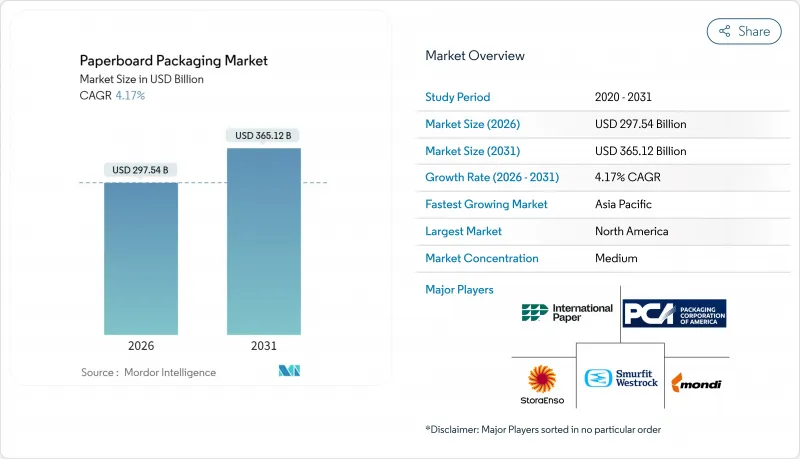

板紙包装市場は、2025年の2,856億3,000万米ドルから2026年には2,975億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR 4.17%で推移し、2031年には3,651億2,000万米ドルに達すると予測されています。

電子商取引量の増加、プラスチックよりも繊維を優先する規制の勢い、軽量化およびデジタル加工技術の継続的な改善が相まって、市場の拡大を推進しています。再生繊維の優れたコストパフォーマンス特性は、循環型サプライチェーンへの小売業者の取り組みを補完し、原材料コストの変動にもかかわらず需要を持続させています。段ボール包装は物流ネットワークの基幹を成し続ける一方、高級消費財分野では折り畳み式カートンの採用が拡大しています。市場参入企業は、エネルギーコスト上昇や古紙価格の変動性に対処するため、垂直統合や低コスト林業地域におけるパルプ生産能力への投資を進めています。

世界の板紙包装市場の動向と洞察

電子商取引の急拡大が段ボール輸送需要を牽引

オンライン小売の浸透に伴い、複数の取扱工程に耐え得る強度と寸法最適化を備えた輸送容器が求められています。箱メーカーは高性能フルートプロファイルと、SKU形状に合わせた包装設計を可能にするリアルタイム設計ツールを組み合わせることで、急増する受注を獲得しました。2025年初頭のPCA(Packaging Corporation of America)によるトン当たり70米ドルの価格引き上げは、需給バランスの逼迫を如実に示しています。消費者直販モデルは外装パッケージへのブランディングスペースの必要性をさらに強化し、コンバーターが高精細デジタル印刷モジュールの統合を促進する要因となっています。位置情報や衝撃を監視するスマートラベル技術が段ボールライナーに搭載されるようになり、保護機能を超えた価値を創出しています。

プラスチック代替規制が繊維包装を後押し

欧州連合(EU)の包装・包装廃棄物規制では、2030年までに90%のリサイクル性を義務付けており、多層プラスチックからリサイクル可能な繊維素材への移行が加速しています。北米の州では拡大生産者責任制度が導入され、アジア太平洋地域の複数の市場でも同様の法令が策定中です。生産者は分散型バリアコーティングやPFASフリーの耐油性化学処理技術で対応し、食品保護と再生パルプ化の両立を図っています。ブランドオーナーはこれらのソリューションを活用し、公約した持続可能性目標を達成するとともに、導入が迫るプラスチック税を回避しています。

森林破壊と繊維調達への監視強化

欧州連合(EU)の森林破壊防止規則の実施により、製紙工場は2020年12月以降に森林破壊が行われていないと認証された区画まで木材の追跡を義務付けられ、監査コストが増加するとともに、非準拠サプライチェーンは輸入禁止措置の対象となります。多国籍企業は同様のプロトコルを全世界に拡大し、事実上コンプライアンスを世界の化します。中小コンバーターは不釣り合いな管理負担に直面し、認証プールやプランテーション所有者との垂直的提携へと向かっています。認証原木に支払われるプレミアムは特定グレードの損益分岐点を押し上げ、管理連鎖システムが成熟するまでマージンを圧迫します。

セグメント分析

再生繊維は、広範な家庭ごみ回収ネットワークと成熟した脱墨技術に支えられ、2025年に板紙包装市場の72.10%のシェアを獲得しました。このセグメントは循環性目標に関連する規制上のクレジットにより、バージングレードを上回る6.65%のCAGRを記録すると予測されています。ブランドオーナーが高需要SKUにおける最低限の再生紙含有率を義務付ける動きを受け、再生紙グレードの板紙包装市場規模は拡大が見込まれます。一方、化粧品ギフトボックスや医薬品ブリスターカードなど、完璧な視覚品質や高い湿潤強度が必須の用途では、バージン繊維の重要性が維持されます。

低コストな植林林業への継続的な投資が再生紙の優位性を強化しています。スザノ社の新たなブラジル産ユーカリ複合施設は、年間255万トンの高輝度パルプを供給し、回収原料とシームレスにブレンドされるため、世界中の製紙工場における平均原料コストを低減します。FSCおよびPEFC認証は再生紙シートの差別化をさらに促進し、コンバーターが環境意識の高い消費者に響くカーボンニュートラル主張を追加することを可能にします。こうした供給安定性とブランディング効果により、再生繊維は板紙包装市場の最前線に立っています。

段ボール箱は、オムニチャネル小売に伴う出荷頻度の急増に後押しされ、2025年には売上高シェア42.10%を占めました。組み込まれた防湿層と耐圧性マイクロフルートにより、これらの箱は自動仕分けシステムを最小限の損傷で通過でき、その不可欠性を強化しています。折り畳み式カートンは生産量は少ないもの、高精細印刷能力がプレミアム食品・パーソナルケア製品の配置と合致するため、5.55%という最速のCAGRが見込まれます。鮮やかな印刷とリサイクル性の向上を両立する「棚出し可能包装」の需要拡大に伴い、折り畳み式カートンの紙製包装市場規模も拡大すると予測されます。

イノベーションの面では、グライフ社のEnviroRAP(TM)が、ラミネート加工された郵送用封筒に代わる単一素材の包装形態を実現しながら、家庭でのリサイクル性を維持しています。デジタル段ボール製造機における並行した進歩により、加工業者は印刷速度で可変データを印刷できるようになり、地域ごとの祝祭テーマやインフルエンサーとのコラボレーションをサポートします。このような柔軟性が、板紙包装市場における段ボールソリューションの差別化要因となり、流通の主力としての優位性を維持しています。

地域別分析

北米地域は2025年に38.55%の収益シェアを占め、統合された再生繊維ネットワークと州レベルのプラスチック削減義務化が、コンバーターを家庭ごみ回収可能なソリューションへ導いたことが背景にあります。パッケージング・コーポレーション・オブ・アメリカの18億米ドルに及ぶコンテナボード買収は地域生産能力を強化し、規模の経済性を活用する業界再編の証左となりました。小売業者の即日配送サービスは、適切なサイズの段ボール輸送容器への需要をさらに刺激し、エネルギーコストの上昇という逆風にもかかわらず、板紙包装市場が中程度の単一桁成長を維持するのに貢献しています。

アジア太平洋地域は最も急速に拡大する市場であり、都市部の家庭が包装された日用品やファストフードの購入を増やすことで、2031年までにCAGR6.78%を記録する見込みです。中国では輸出注文において繊維系輸送用包装材の指定が増加しており、ベトナムの国内産業は2026年までに包装収益35億米ドルを見込んでおります。地域政府は新たな廃棄物指令に循環型経済条項を盛り込み、再生シート輸入業者に関税優遇措置を付与しております。こうした政策手段に加え、低コスト労働力と拡大するオンライン小売が相まって、アジア太平洋地域は板紙包装市場の成長エンジンとなっております。

欧州では、PPWR(包装廃棄物指令)やEUDR(欧州廃棄物指令)といった規制を背景に、リサイクル性と調達基準を強化する素材革新が持続しています。サッピ社による5億ユーロ(5億8,773万米ドル)の機械更新は軽量コート紙の生産能力を向上させ、モンディ社の買収攻勢は消費財クラスター全域で折り畳み式カートンの事業基盤を拡大しています。高い回収率と消費者のエコラベルへの受容性により堅調な基盤は維持されていますが、マクロ需要の低迷が生産量の伸びを抑制しています。それでも、厳格なコンプライアンス要件が障壁となり、板紙包装市場における既存プレイヤーに有利な状況を生み出しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の急増が段ボール輸送需要を押し上げる

- プラスチック代替規制は繊維包装を有利にする

- 軽量化技術による物流コスト削減

- アジア太平洋地域における包装食品・飲料の急速な成長

- AIを活用したオンデマンドカスタム印刷

- ラテンアメリカにおけるユーカリパルプブームがバージン繊維コストを低下させている

- 市場抑制要因

- 森林伐採と繊維調達への監視強化

- 再生紙およびエネルギーコストの変動性

- ブランドオーナーによる持続可能性に関する公約の後退

- 柔軟性のあるプラスチック製パウチのシェア浸食

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品・サービスの脅威

- 競争企業間の敵対関係

- マクロ経済要因が市場に与える影響

- テクノロジーの展望

- 規制情勢

第5章 市場規模と成長予測

- 原材料別

- バージンファイバー

- 再生繊維

- 製品タイプ別

- 折り畳み式カートン

- 段ボール箱

- 硬質ボックス

- その他の製品タイプ

- 包装形態別

- 一次包装

- 二次包装

- トランジット/Eコマース配送

- エンドユーザー業界別

- 食品

- 飲料

- ヘルスケア

- パーソナルケアおよび化粧品

- 家庭用品

- 電気・電子機器

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ベトナム

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向と発展

- 市場シェア分析

- 企業プロファイル

- International Paper Company

- Smurfit WestRock

- Mondi plc

- Packaging Corporation of America

- Stora Enso Oyj

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Rengo Co., Ltd.

- Metsa Board Oyj

- Graphic Packaging Holding Company

- Cascades Inc.

- Sonoco Products Company

- Nine Dragons Paper(Holdings)Ltd.

- Georgia-Pacific LLC

- Klabin S.A.

- Sappi Limited

- Mayr-Melnhof Karton AG

- Huhtamaki Oyj

- Visy Industries Holdings Pty Ltd.

- Seaboard Folding Box Company Inc.

- Clearwater Paper Corporation

- ITC Limited