|

市場調査レポート

商品コード

1907273

北米の飼料添加物:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)North America Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の飼料添加物:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

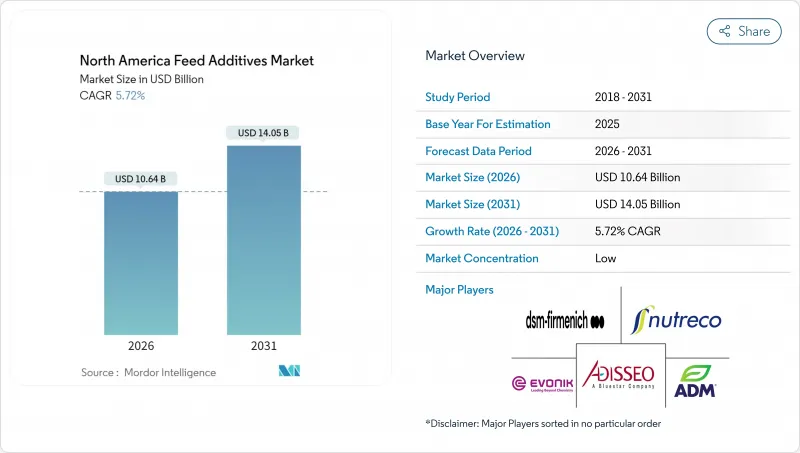

北米の飼料添加物市場は、2025年の100億6,000万米ドルから2026年には106億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR5.72%で推移し、2031年までに140億5,000万米ドルに達すると予測されております。

精密畜産栄養への堅調な需要、抗生物質成長促進剤に対する規制上の制限、そして高まる持続可能性への要請が、北米の飼料添加物市場の着実な拡大を支えています。産業規模の畜産統合が進む中、大規模農場では飼料要求率と家畜の生産性を向上させるカスタマイズされた添加剤パッケージの導入が促進されています。同時に、リアルタイムデータ分析を活用したデジタル配合プラットフォームがサプライヤーの差別化を強化する一方、アミノ酸調達におけるサプライチェーンの脆弱性は価格動向に影響を与え続けております。合併・買収活動の活発化は、主要企業が戦略的事業売却やポートフォリオ再編を通じて中核能力に注力する中、競争環境が成熟化していることを示しております。

北米の飼料添加物市場の動向と洞察

高タンパク質肉・乳製品への需要増加

消費者の食習慣がタンパク質豊富な食品を好む傾向が強まる中、畜産農家は標的を絞った添加物補給により飼料転換効率の最大化を図っています。北米の一人当たり肉消費量は世界最高水準を維持しており、鶏肉消費量だけでも年間50.8kgに達するため、急速な筋肉発達と産卵を支える最適化されたアミノ酸プロファイルが不可欠です。特に酪農経営では、精密なミネラル補給とルーメン保護型アミノ酸が乳タンパク質含有量を向上させつつ窒素排泄を低減する効果を発揮します。この動向は、有機微量ミネラル、バイパスタンパク質、代謝エネルギー増強剤など、タンパク質生産指標と直接相関する特殊添加剤の導入を加速させています。飼料費が畜産総費用の60~70%を占めることから、経済的な乗数効果が明らかになり、変動する商品価格の中で利益率を維持するためには、添加剤による効率向上が極めて重要となります。

工業的畜産・養鶏生産の拡大

大規模経営への統合は、添加物需要のパターンを根本的に変えます。メガファームでは、一貫性のある科学的に検証された飼料配合を必要とする高度な栄養管理システムを導入しているためです。1万頭を超える規模の経営体が北米の畜産を支配する傾向が強まっており、これらの施設は規模の経済を生み出し、高品質な添加物パッケージや精密給餌技術への投資を正当化する要因となっています。垂直統合の動向では、主要なタンパク質企業が飼料工場や添加剤サプライヤーを買収し、生産チェーン全体の品質とコストを管理しています。気候、水資源、輸送インフラに恵まれた地域への地理的集中は、特に米国コーンベルトやカナダ・プレーリー地方において、地域的な添加剤需要の急増を促しています。この工業化プロセスは、液体サプリメント、マイクロカプセル化製品、既存の飼料製造設備と統合可能な精密投与システムなど、自動化対応型の添加剤形態の導入を加速させています。

主要添加物の原料価格変動

アミノ酸価格の変動性は飼料添加物市場の市場力学に直接影響を及ぼします。メチオニンとリジンのコストは、エネルギー価格、原料の入手可能性、アジア太平洋地域の製造拠点における生産能力稼働率に基づき、年間20~40%変動します。世界のアミノ酸生産が中国に集中していることは、サプライチェーンの脆弱性を生み出し、北米の飼料メーカーや畜産農家にとって予測不可能なコスト構造につながっています。この経済的影響はバリューチェーン全体に波及します。畜産農家は費用対効果の計算に基づき添加剤の配合率を調整するため、価格変動が極端な時期には家畜の生産性が低下する可能性があります。多くの添加剤原料が特殊な性質を持つこと、また代替サプライヤーが限られていることから、先物契約や価格ヘッジの仕組みによる保護効果は限定的です。

セグメント分析

2025年時点で、アミノ酸は北米の飼料添加物市場において20.18%と最大のシェアを維持しており、高密度養鶏・養豚施設からのメチオニンおよびリジンの絶え間ない需要に支えられています。北米の飼料添加物市場におけるアミノ酸の規模は、エボニック社の生産能力拡大とDSM-フィルメニック社の戦略的再編により地域供給が強化されることから、着実な拡大が見込まれます。酸性化剤は2031年までCAGR6.58%で最も高い成長勢いを示しており、腸内健康管理における有機酸の有効性を浮き彫りにする抗生物質成長促進剤の規制強化が後押ししています。

これらの主要カテゴリーに加え、プロバイオティクス、酵素、有機ミネラルは、生体利用率の向上と環境配慮の訴求を背景に、総合的にシェアを拡大しています。ニッチなイノベーターが耐熱性酵素やマイクロカプセル化技術における未充足ニーズを掘り起こすことで競合は激化していますが、サプライチェーンの集中化により原材料価格の変動性は依然として懸念材料となっています。

北米の飼料添加物市場レポートは、添加物別(酸性化剤、アミノ酸、抗生物質など)、動物別(水産養殖、家禽、反芻動物など)、地域別(カナダ、メキシコ、米国など)に分類されています。市場予測は金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリー主要な調査結果

第4章 主要な業界動向

- 家畜頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 豚

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 高タンパク質肉・乳製品への需要増加

- 産業規模の家畜・家禽生産の拡大

- 抗生物質成長促進剤削減に向けた規制強化

- 家畜のメタン排出量削減を目的とした機能性飼料

- 昆虫由来タンパク質ミール需要の拡大に伴う専用プレミックスの必要性

- デジタルツインモデリングによるカスタマイズされた添加剤導入の加速

- 市場抑制要因

- 主要添加物の原料価格の変動性

- 新規添加物に対するFDAおよびCFIAの承認プロセスが長期化する傾向

- 合成添加物に対する消費者の懐疑的な見方による小売業界からの圧力

- アミノ酸生産の地理的集中によるサプライチェーンリスク

第5章 市場規模と成長予測(数量および金額)

- 添加物

- 酸性化剤

- サブ添加物別

- フマル酸

- 乳酸

- プロピオン酸

- その他の酸味料

- サブ添加物別

- アミノ酸

- サブ添加物別

- リジン

- メチオニン

- トレオニン

- トリプトファン

- その他のアミノ酸

- サブ添加物別

- 抗生物質

- サブ添加物別

- バシトラシン

- ペニシリン類

- テトラサイクリン系

- タイロシン

- その他の抗生物質

- サブ添加物別

- 抗酸化剤

- サブ添加物別

- ブチル化ヒドロキシアニソール(BHA)

- ブチル化ヒドロキシトルエン(BHT)

- クエン酸

- エトキシキン

- プロピルガレート

- トコフェロール

- その他の抗酸化剤

- サブ添加物別

- 結合剤

- サブ添加物別

- 天然結合剤

- 合成結合剤

- サブ添加物別

- 酵素

- サブ添加物別

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- サブ添加物別

- 香料・甘味料

- サブ添加物別

- フレーバー

- 甘味料

- サブ添加物別

- ミネラル

- サブ添加物別

- 主要ミネラル

- 微量ミネラル

- サブ添加物別

- マイコトキシン解毒剤

- サブ添加物別

- 結合剤

- バイオトランスフォーマー

- サブ添加物別

- 植物性原料

- サブ添加物別

- 精油

- ハーブ・スパイス

- その他の植物性原料

- サブ添加物別

- 色素

- 添加物別

- カロテノイド

- クルクミン&スピルリナ

- 添加物別

- プレバイオティクス

- サブ添加物別

- フルクトオリゴ糖

- ガラクトオリゴ糖

- イヌリン

- ラクツロース

- マンナンオリゴ糖

- キシロオリゴ糖

- その他のプレバイオティクス

- サブ添加物別

- プロバイオティクス

- サブ添加物別

- ビフィズス菌

- エンテロコッカス

- 乳酸菌

- ペディオコッカス

- ストレプトコッカス

- その他のプロバイオティクス

- サブ添加物別

- ビタミン

- サブ添加物別

- ビタミンA

- ビタミンB

- ビタミンC

- ビタミンE

- その他のビタミン

- サブ添加物別

- 酵母

- サブ添加物別

- 生酵母

- セレン酵母

- 使用済み酵母

- トルラ乾燥酵母

- ホエイ酵母

- 酵母派生品

- サブ添加物別

- 酸性化剤

- 動物

- 水産養殖

- サブ動物別

- 魚類

- エビ

- その他の水産養殖

- サブ動物別

- 家禽類

- サブ動物別

- ブロイラー

- 採卵鶏

- その他の家禽

- サブ動物別

- 反芻動物

- サブ動物別

- 肉用牛

- 乳用牛

- その他の反芻動物

- サブ動物別

- 豚

- その他の動物

- 水産養殖

- 地域

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- 企業概要

- 企業プロファイル

- Archer Daniels Midland Co.

- DSM-Firmenich AG

- Evonik Industries AG

- Adisseo

- Nutreco NV(SHV Holdings N.V.)

- Alltech, Inc.

- BASF SE

- Cargill Inc.

- IFF Danisco Animal Nutrition(International Flavors and Fragrances Inc.)

- Land O Lakes Inc.

- Novus International

- Kemin Industries

- Phibro Animal Health Corporation

- Zoetis Inc.

- Elanco Animal Health Inc.