|

市場調査レポート

商品コード

1686221

農業検査:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Agricultural Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業検査:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

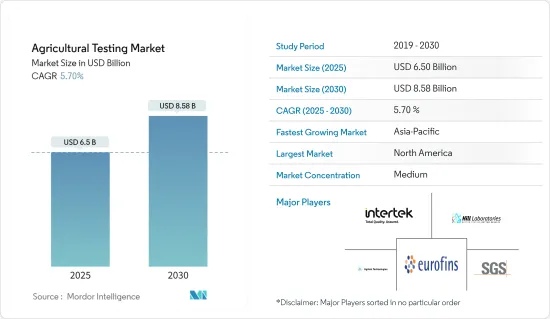

農業検査の市場規模は2025年に65億米ドルと推定され、予測期間(2025-2030年)のCAGRは5.7%で、2030年には85億8,000万米ドルに達すると予測されます。

主なハイライト

- 農業検査では、水、土壌、種子などのサンプルを検査し、その品質と汚染物質のレベルを評価します。この産業は、特に世界中の先進地域や商業化された地域で大きな成長を遂げています。環境の安全性を確保し、農業の生産性を向上させるために、規制や法律が市場の拡大を大きく後押ししています。

- 今後数年間で、農業検査市場は力強く回復すると予想され、その原動力は農産物の需要増による生産量の増加と定期的な土壌検査の必要性です。さらに、消費者の嗜好が、食品の安全性と品質、特に残留化学物質に関するより高い基準へとシフトしています。このため、高品質生産のために土壌特性を維持する必要性が高まっており、市場の成長を後押ししています。

- 世界化により、穀物や油糧種子の取引を促進するために、標準化された評価技術が必要とされています。その結果、輸出業者や輸入業者は、世界の品質・安全基準への適合を証明するために分析証明書を要求するようになっています。このため、特に農産物の輸出が多い地域では、農産物に関連する検査サービスに対する需要が増加しています。例えば、中国の玄米輸出額は2020年の1億6,886万7,000米ドルから2022年には2億1,184万7,000米ドルへと大幅に増加しました。しかし、輸出業者は穀物中の高水分レベルに起因するカビの繁殖による課題に直面しています。カビの繁殖による高い毒性は、許容毒性レベルに関する厳しい規制により、世界市場で玄米の不合格につながっています。

- 農業検査市場は現在北米が支配的です。これは、この地域の食品安全、環境、農業、栄養成分、化学物質、表示に関する規制が厳しいことに起因しています。この地域には数多くの農業検査サービスプロバイダーが存在し、市場の成長に寄与しています。

農業検査市場の動向

農業検査と環境安全性に関する規制と法規制

農業検査と環境安全性に関する規制と法規制が市場成長の主要促進要因となっています。農業と食品の安全性に取り組む政府の取り組みが市場拡大を後押ししています。例えば、食品医薬品局(FDA)は最近、FDA食品安全近代化法(FSMA)農産物安全規則の改定を提案し、灌漑用水中の有害な汚染物質が食中毒の原因となるのを防ぐことで食品の安全性を強化するとしています。提案されたガイドラインでは、対象となる農場は、少なくとも年1回、また変化が生じた場合はいつでも、収穫前の農業用水評価を実施することが義務付けられ、これにより汚染のリスクが低減されます。このような規制の変更は、消費者の製品の安全性を確保しつつ、農家により大きな柔軟性を提供することを目的としています。

サンプル検査は、農産物の輸出成長を維持するため、商業化された農業国で人気を博しています。国際種子検査協会(ISTA)が手順の標準化と種子取引の近代化に重要な役割を果たしています。

2022年4月、カナダ政府はカナダ穀物サンプリング・プログラム(CGSP)を開始し、企業が種子、穀物、穀物製品のバッチからサンプルを収集・提供し、カナダからの輸出の植物検疫認証を支援できるようにしました。この方針は、カナダ食品検査庁(CFIA)がCGSPに参加する企業を承認するためのガイドラインを定めたものです。さらに、この方針には、サンプルの収集とCFIAへの提出に必要な手順が詳述されています。

さらに2024年、英国政府は、認定貿易検査官(ATI)による穀物のサンプリングと検査の手順を含む、イングランドとウェールズから認証を必要とする非EUへのバルク穀物輸出のための植物検疫証明書発行のための穀物標準作業手順書(GSOP)を更新しました。農産物検査市場は、世界・サプライ・チェーン全体の安全性と品質を確保するための検査プロトコルを強制する政府の義務化により、大きな変化を経験しています。これらのガイドラインは、汚染を防止するためにあらゆる段階で綿密な手順を必要とし、それによって世界中の農業検査の需要を促進しています。

北米が市場を独占する見込み

北米は世界最大の農業検査市場であり、米国は種子検査の継続的需要により魅力的な市場となっています。この需要は、米国における種子の認証の必要性が原動力となっています。種子規制試験部門(SRTD)は、農業用種子を試験し、種子の効率的かつ秩序ある販売を確保し、市場の成長を支える上で重要な役割を果たしています。さらに、食品安全への取り組みも重視されています。例えば、米国疾病予防管理センター(CDC)は、毎年4,800万人が食中毒で病気になると推定しています。これに対処するため、連邦穀物検査局は、よりスマートな食品安全ブループリント計画の一環として、検査手法の標準化、検査・試験所サービスの評価、最終用途の品質属性を高めるための新たな検査・分析手法の開発を進めています。

カナダでは、農業部門は技術の進歩、政策の変更、消費者の嗜好の進化により大きな変化を遂げており、高品質、安全、栄養的に安定した生産物に対する需要の高まりに対応するため、農産物のマーケティングへの投資が増加しています。このような需要の増加により、厳格な検査プロトコルが必要となり、国内の検査市場をさらに牽引しています。さらに、農業部門における特定要件への傾向は、英国のWarburtonsのような企業がカナダの小麦生産者と契約を結ぶことで実証されており、個別仕様へのニーズの高まりを強調しています。2023年、ハーベストサンプルプログラムは、2022年の256サンプルに対し、379サンプルの油糧種子タイプ大豆を受理しており、検査重視の傾向が強まっていることを浮き彫りにしています。

こうした検査基準の向上は、北米農業セクターの評価を高め、輸出増加への道を開くものであり、国際的な品質・安全基準を満たすための検査サービスに対するニーズの高まりにつながっています。

農業検査業界の概要

世界の農業検査市場は断片化されており、多数の政府系検査機関が世界中の農家に様々な農業検査サービスを提供しています。Eurofins Scientific、R J Hill Laboratories Ltd、Agilent Technologies Inc.、SGS SA、Intertekなどが大手企業です。各社は、機器の品質とプロモーションに基づいて農業検査市場で競争し、市場でより大きなシェアを握るために戦略的な動きに注力しています。新サービス、パートナーシップ、買収は、市場の主要企業が採用する主要戦略です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サンプル

- 水質検査

- 土壌検査

- 種子検査

- バイオソリッド検査

- 糞尿検査

- その他のサンプル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- オーストラリア

- 日本

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他のアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Eurofins Scientific

- Intertek

- SGS SA

- Bureau Veritas SA

- Merieux NutriSciences Corporation

- Temasek Holdings(Element Materials Technology)

- TUV Nord Group

- Agilent Technologies Inc.

- EMD Millipore Corporation

- BioMerieux SA

- R J Hill Laboratories Limited

第7章 市場機会と今後の動向

The Agricultural Testing Market size is estimated at USD 6.50 billion in 2025, and is expected to reach USD 8.58 billion by 2030, at a CAGR of 5.7% during the forecast period (2025-2030).

Key Highlights

- Agricultural testing involves the examination of samples such as water, soil, and seeds to assess their quality and levels of contaminants. This industry is experiencing significant growth, particularly in developed areas and commercialized regions across the world. Regulations and laws largely drive the market's expansion to ensure environmental safety and improve agricultural productivity.

- Over the next few years, the agricultural testing market is anticipated to rebound strongly, driven by increased demand for farm products, leading to higher production and the need for regular soil testing. Additionally, there is a shift in consumer preferences toward higher standards of food safety and quality, particularly about chemical residues. This is creating a greater need to maintain soil properties for quality production, thus bolstering the market's growth.

- Globalization has necessitated standardized assessment techniques to facilitate the trade of grains and oilseeds. Consequently, exporters and importers are requesting analysis certificates to demonstrate compliance with global quality and safety standards. This has led to an increased demand for testing services related to agricultural outputs, particularly in regions with high agricultural exports. For instance, China saw a significant increase in the value of its brown rice exports from USD 168,867 thousand in 2020 to USD 211,847 thousand in 2022. However, exporters are facing challenges due to mold growth caused by high moisture levels in the grains. The high toxicity of the fungal growth has led to the rejection of brown rice in global markets due to stringent regulations on permissible toxicity levels.

- The agricultural testing market is currently dominated by North America. This is attributed to the region's stringent regulations related to food safety, environment, agriculture, nutritional content, chemicals, and labeling. The presence of numerous agricultural testing service providers in the region is contributing to the market's growth.

Agricultural Testing Market Trends

Regulations and Legislations Pertaining to Agriculture Testing and Environmental Safety

Regulations and legislation concerning agricultural testing and environmental safety have been key drivers for the market's growth. Government initiatives to address agricultural and food safety have propelled market expansion. For instance, the Food and Drug Administration (FDA) recently proposed revisions to the FDA Food Safety Modernization Act (FSMA) Produce Safety Rule to enhance food safety by preventing harmful contaminants in irrigation water from causing foodborne illnesses. Under the proposed guidelines, covered farms would be mandated to conduct pre-harvest agricultural water assessments at least once annually and whenever changes occur, thereby reducing the risk of contamination. These regulatory changes aim to provide farmers with greater flexibility while ensuring product safety for consumers.

Sample testing has gained popularity in commercialized agriculture countries to sustain the export growth of agricultural commodities. Seed and soil testing have also seen increased adoption, with the International Seed Testing Association (ISTA) playing a crucial role in standardizing procedures and modernizing the seed trade.

In April 2022, the Canadian government initiated the Canadian Grain Sampling Program (CGSP), allowing companies to gather and deliver samples from batches of seed, grain, and grain products to assist with phytosanitary certification for exports from Canada. This policy sets out the guidelines that the Canadian Food Inspection Agency (CFIA) uses to approve companies participating in the CGSP. Furthermore, this policy details the steps that need to be taken for the collection and submission of samples to the CFIA.

Moreover, in 2024, the UK government updated the grain standard operating protocol (GSOP) for the issue of phytosanitary certificates for the export of bulk grain from England and Wales to non-EU requiring certification, including the procedures for sampling and inspection of grain by authorized trade inspectors (ATI). The agricultural testing market is experiencing a major shift as government mandates enforce testing protocols to ensure safety and quality throughout the global supply chain. These guidelines necessitate meticulous procedures at every stage to prevent contamination, thereby driving the demand for agricultural testing across the world.

North America is Expected to Dominate the Market

North America is the largest market for agricultural testing globally, with the United States being an attractive market due to the ongoing demand for seed testing. This demand is driven by the need for certifications for seeds in the United States. The Seed Regulatory and Testing Division (SRTD) plays a crucial role in testing agricultural seeds, ensuring the efficient and orderly marketing of seeds, and supporting the growth of the market. Furthermore, there is a significant emphasis on food safety initiatives. For instance, the United States Centers for Disease Control and Prevention (CDC) estimated that 48 million people get sick every year from a foodborne illness. To address this, the Federal Grain Inspection Service is standardizing testing methodologies, evaluating testing and laboratory services, and developing new testing and analytical methods to enhance end-use quality attributes as part of the Smarter Food Safety Blueprint plan.

In Canada, the agriculture sector has been undergoing significant changes due to technological advancements, policy changes, and evolving consumer preferences, with increased investments in the marketing of agriculture products to meet the increasing demand for high-quality, safe, and nutritionally consistent output. This increased demand has necessitated rigorous testing protocols, further driving the market for testing in the country. Additionally, the trend toward specific requirements in the agriculture sector is exemplified by companies such as Warburtons in the United Kingdom establishing contracts with Canadian wheat producers, emphasizing the growing need for tailored specifications. In 2023, the Harvest Sample Program received 379 samples of oilseed-type soybean, compared to 256 samples in 2022, highlighting the growing emphasis on testing.

These improved testing standards enhance the reputation of the North American agriculture sector and pave the way for increased exports, leading to a greater need for testing services to meet international quality and safety standards.

Agriculture Testing Industry Overview

The global agricultural testing market is fragmented, with numerous government-operated laboratories providing various agricultural testing services to farmers worldwide. Eurofins Scientific, R J Hill Laboratories Ltd, Agilent Technologies Inc., SGS SA, and Intertek are some of the major players. Companies compete in the agricultural testing market based on equipment quality and promotion and focus on strategic moves to hold larger shares in the market. New services, partnerships, and acquisitions are the major strategies adopted by the leading companies in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sample

- 5.1.1 Water Testing

- 5.1.2 Soil Testing

- 5.1.3 Seed Testing

- 5.1.4 Bio-solids Testing

- 5.1.5 Manure Testing

- 5.1.6 Other Samples

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Rest of Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Eurofins Scientific

- 6.3.2 Intertek

- 6.3.3 SGS SA

- 6.3.4 Bureau Veritas SA

- 6.3.5 Merieux NutriSciences Corporation

- 6.3.6 Temasek Holdings (Element Materials Technology)

- 6.3.7 TUV Nord Group

- 6.3.8 Agilent Technologies Inc.

- 6.3.9 EMD Millipore Corporation

- 6.3.10 BioMerieux SA

- 6.3.11 R J Hill Laboratories Limited