|

市場調査レポート

商品コード

1685942

殺線虫剤:市場シェア分析、産業動向、成長予測(2025年~2030年)Nematicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 殺線虫剤:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 318 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

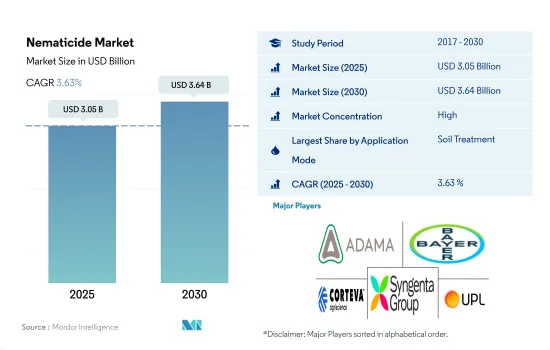

殺線虫剤の市場規模は2025年に30億5,000万米ドルと予測され、2030年には36億4,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは3.63%で成長する見込みです。

土壌媒介性線虫による作物生育初期の被害が増加し、線虫剤の土壌処理適用モードが高まる

- 農業における線虫の増殖は、干ばつ、熱波、温暖多湿といった気候の変化によって好都合になります。また、単一栽培、不耕起、砂質土壌も線虫の生育に好都合です。線虫の種類、地域、作物に応じて、農家は線虫の管理を改善し、作物生産を向上させるため、様々な線虫剤の散布方法を実施しています。

- 土壌治療による線虫剤散布は、2022年に70.3%と大半の市場シェアを占めたが、これは主に、土壌を媒介する線虫の個体数を減らし、作物の生産性を向上させる上で、この方法が有効であることに起因しています。これは、土壌を媒介する線虫の個体数を減らし、作物の生産性を向上させるのにこの方法が有効であるためです。土壌処理による殺線虫剤散布は、2023年~2029年の間に約1万7,300トン増加すると予想されます。

- 殺線虫剤の葉面散布法は、次に多く使用される散布モードで、最も急速に成長しているセグメントであり、予測期間中にCAGR 3.4%を記録すると予測されます。葉面線虫剤散布は、植物の葉を食害し、食用作物の収量を減少させる葉面線虫を効果的に管理します。ドローンによる散布やその他の技術的・デジタル的改良のような葉面散布モードの進歩が、葉面散布モードを引き上げています。

- 水と殺線虫剤量の効果的な管理は、化学灌漑モードによって達成することができ、2022年の市場シェアは8.5%でした。高度な灌漑システムと水不足の深刻化により、化学灌漑の普及率が高まり、殺線虫剤の散布が増加します。

- すべての散布モードは線虫の侵入を減らし、作物の生産性を高めることを目的としており、これが市場を牽引すると予想されます。

線虫蔓延の増加と殺線虫剤の採用拡大が南米で顕著な地位を占める

- 気候変動や他の病害虫とは別に、線虫は世界中の農業セクターに大きな損害を与えています。4100種以上の植物寄生性線虫が確認され、世界中で様々な作物に被害をもたらしています。

- 米国植物病理学会によると、線虫は世界の作物損失の約14%を毎年引き起こしており、これはほぼ1,250億米ドルの経済損失に相当します。様々な線虫の中でも、根こぶ線虫(Meloidogyne spp.)、シスト線虫(Heterodera spp.、Globodera spp.)、根こぶ線虫(Pratylenchus spp.、Hirschmanniella spp、およびRadopholus spp.)、茎線虫(Ditylenchus spp.)、およびマツ材線虫(Bursaphlenchus spp.)は、水と養分の吸収に影響を与えることによって、作物の成長と生産性に大きなダメージを与えます。

- 農作物栽培における殺線虫剤の消費は、2022年に世界の殺線虫剤市場の37.4%を占めた南米が大部分を占めています。これは線虫による作物の損失が主な原因であり、毎年約65億米ドルが記録されています。大豆は主要な栽培作物であり、南米は世界で生産される大豆の50%以上を生産しています。線虫は、この地域で約30%(30億米ドル相当)の収量損失を引き起こしています。過去の期間中、殺線虫剤の消費量は2017年から2022年の間に約7,600トン増加し、さらに2023年から2029年の間に1万100トン以上増加すると予想されています。このことは、南米の農業における殺線虫剤の必要性を強調しています。

- 世界の殺線虫剤市場は、予測期間中(2023年~2029年)にCAGR 3.7%で成長すると予測され、これは世界的に様々な線虫から作物を保護するために殺線虫剤の採用が増加していることに牽引されます。

世界の殺線虫剤市場の動向

集約的な農法により、殺線虫剤散布の必要性が増加

- 2022年の化学殺線虫剤の世界平均消費量は、農地1ヘクタール当たり2.1kgでした。アジア太平洋地域が最大の殺線虫剤消費国で、2022年の1ヘクタール当たりの消費量は737.02グラムでした。日本を含むアジア諸国は、温室栽培や単作などの集約的農法を一般的に採用しています。こうした方法は生産性を高めるが、線虫のような土壌伝染性害虫に対する作物の脆弱性も高める。その結果、農家は作物を守るために線虫駆除剤に頼ることが多いです。

- 欧州は、2022年には1ヘクタール当たり591.7グラムの殺線虫剤を使用し、ヘクタール当たりの消費量が2番目に多くなりました。欧州諸国では、線虫の被害を受けやすい野菜、果物、観葉植物などの高価値作物の栽培が拡大しています。植物寄生性線虫は、欧州諸国において年間21.3%の収量損失を引き起こし、その額は15億8,000万米ドルに達します。その結果、欧州でこれらの侵入を効果的に管理・防除するには、殺線虫剤の使用が必要となっています。

- 南米は2022年に1ヘクタール当たり570.14グラムの殺線虫剤を使用し、第3位の消費国でした。根こぶ線虫はこの地域のトマト、ジャガイモ、ニンジンなど様々な植物の根や塊茎を加害します。ニンジンは平均20.0%、ジャガイモはさらに高い33.0%の損失を被る可能性があります。北米諸国では、土壌の攪乱を減らし作物残渣の保持を高める不耕起栽培の導入が進むにつれ、線虫の数が増加しています。このような状況から、世界的に線虫駆除剤の散布が行われています。

気候条件の変化とそれが線虫の蔓延に及ぼす影響により、殺線虫剤の需要と価格が同時に高まる可能性があります。

- 殺線虫剤は、植物寄生性線虫を効果的に防除し、作物を根の被害から守り、最適な収量と生産性を確保することで、農業において重要な役割を果たしています。

- フルフェンスルホンは、アリールスルホン酸塩の化学クラスに属する殺線虫剤です。様々な農作物において、根こぶ線虫、シスト線虫、病害線虫、ダガー線虫などの植物寄生性線虫を防除するために使用されます。フルフェンスルホンの作用機序は線虫の神経系に干渉し、麻痺と死に導くことです。線虫を標的にすることで、フルフェンスルホンは線虫の個体数を減らし、農作物に与える被害を最小限に抑えることができます。フルフェンスルホンの2022年の価格は1万9,000トン米ドルでした。

- アバメクチンは、根こぶ線虫(Pratylenchus penetrans)、腎状線虫(Rotylenchus reniformis)、根こぶ線虫(Meloidogyne incognita)、シスト線虫(Heterodera schachtii)など、いくつかの植物寄生性線虫に対する殺線虫活性で知られています。これらの線虫を防除する効果があることから、農作物における線虫管理の貴重なツールとなっています。2022年現在、アバメクチンの市場価値はトン当たり約1万2,200米ドルです。

- オキサミルは広く使用されている殺虫・殺線虫剤で、カルバマートに属します。主に農作物の様々な植物寄生性線虫の駆除に使用されます。殺虫・殺線虫剤としてのオキサミルの作用機序は、昆虫や線虫の神経機能に不可欠な酵素であるアセチルコリンエステラーゼの活性を阻害することです。この酵素を阻害することで、オキサミルは神経の過剰刺激を引き起こし、害虫の麻痺と死に至る。2022年の価格は1トン当たり8,800米ドルでした。

殺線虫剤産業の概要

殺線虫剤市場はかなり統合されており、上位5社で85.65%を占めています。この市場の主要企業は以下の通りです。 ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, Syngenta Group and Upl Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- カナダ

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- メキシコ

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- ウクライナ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他の南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd.

- Albaugh LLC

- American Vanguard Corporation

- Bayer AG

- Corteva Agriscience

- Syngenta Group

- Tessenderlo Kerley Inc.(Novasource)

- Upl Limited

- Vive Crop Protection

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 49674

The Nematicide Market size is estimated at 3.05 billion USD in 2025, and is expected to reach 3.64 billion USD by 2030, growing at a CAGR of 3.63% during the forecast period (2025-2030).

Increasing early crop growth damage by soil-borne nematodes raises the soil treatment application mode of nematicides

- The growth of nematodes in agriculture is favored by changing climates like drought, heat waves, and warm and humid conditions. Monoculture practices, no-tillage, and sandy soils also favor their growth. Based on the types of nematodes, regions, and crops, farmers implement various nematicide application modes for better nematode management and enhancing crop production.

- Nematicide application via soil treatment held a majority market share of 70.3% in 2022, which was majorly attributed to the effectiveness of this method in reducing soil-borne nematode populations and improving crop productivity. These can be applied prior to planting and after planting by soil drenching, which helps in faster crop germination. The soil treatment mode of nematicide application is expected to increase by around 17.3 thousand metric ton during 2023-2029.

- The foliar method of nematicide application was the next most used application mode and fastest-growing segment, which is anticipated to register a CAGR of 3.4% during the forecast period. The foliar nematicide application effectively manages the foliar nematodes that feed on the foliage of the plant and reduces the yield of food crops. Advancements in foliar mode, like drone applications and other technical and digital improvements, raise the foliar mode of application.

- Effective management of water and nematicide quantity can be achieved through the chemigation mode, which occupied the market share of 8.5% in 2022. Advanced irrigation systems and increased water scarcity will raise the chemigation adoption rate, increasing the nematicide application.

- All the application modes aim to reduce nematode infestations and increase crop productivity, which is expected to drive the market.

Increased nematode infestations and the growing adoption of nematicides stood South America in prominent position

- Apart from climate changes and other pests and diseases, nematodes cause significant damage to the agriculture sector worldwide. More than 4100 plant parasitic nematodes were identified, causing damage to various crops across the world.

- According to the American Society of Phytopathology, nematodes cause around 14% of the global crop loss annually, which is equal to an economic loss of almost USD 125 billion. Among various nematode species root-knot nematodes (Meloidogyne spp.), cyst nematodes (Heterodera spp., Globodera spp.), root-lesion nematodes (Pratylenchus spp., Hirschmanniella spp., and Radopholus spp.), stem nematodes (Ditylenchus spp.), and pine wood nematodes (Bursaphlenchus spp.) majorly damage the crop growth and productivity by effecting the water and nutrients absorption.

- The consumption of nematicides in its cultivation is majorly dominated by South America, which represented 37.4% of the global nematicide market in 2022. This is majorly attributed to the crop losses by nematodes, which are recorded at around USD 6.5 billion every year. Soybean is the major crop grown, and South America produces more than 50% of the soybeans produced in the world. Nematodes cause around 30% of yield loss worth USD 3 billion in the region. During the historical period, the consumption of nematicides increased by around 7.6 thousand metric ton between 2017 and 2022, which is further expected to increase by more than 10.1 thousand metric ton between 2023-2029. This emphasized the nematicide's necessity in the South American agriculture industry.

- The global nematicide market is anticipated to grow during the forecast period (2023-2029) with an estimated CAGR of 3.7%, which will be driven by the growing adoption of nematicides for crop protection from various nematodes globally.

Global Nematicide Market Trends

Intensive agricultural practices have increased the need for nematicide application

- The average global consumption of chemical nematicides was 2.1 kg per hectare of agricultural land in 2022. Asia-Pacific was the largest consumer of nematicides, with a per-hectare consumption of 737.02 grams in 2022. Asian countries, including Japan, commonly adopt intensive farming practices like greenhouse cultivation and monocropping. Although these methods enhance productivity, they also heighten crop vulnerability to soil-borne pests like nematodes. Consequently, farmers frequently resort to nematicides to protect their crops.

- Europe was the second largest per-hectare consumer of nematicides, with 591.7 grams per hectare in 2022. European countries are expanding the cultivation of high-value crops, including vegetables, fruits, and ornamentals, which tend to be more susceptible to nematode damage. The plant-parasitic nematodes cause an annual yield loss of 21.3%, amounting to USD 1.58 billion in European countries. As a result, the use of nematicides becomes necessary to effectively manage and control these infestations in Europe.

- South America was the third largest per-hectare consumer of nematicides, with 570.14 grams per hectare in 2022. Root-knot nematodes attack the roots and tubers of various plants, including tomatoes, potatoes, and carrots in the region. Carrots are susceptible to considerable losses, averaging up to 20.0%, while potatoes can experience even higher losses of up to 33.0% due to infestations caused by these nematode species. The nematode population in North American countries is increasing with the increasing adoption of no-tillage practices, which reduce soil disturbance and increase the retention of crop residue. These circumstances are leading to the application of nematicides globally.

Changing climatic conditions and their effect on nematode infestations may raise the demand for nematicides and their prices simultaneously

- Nematicides play a crucial role in agriculture by effectively controlling plant-parasitic nematodes, protecting crops from root damage, and ensuring optimal yield and productivity.

- Flufensulfone is a nematicide belonging to the chemical class of arylsulfonates. It is used to control plant-parasitic nematodes, such as root-knot nematodes, cyst nematodes, lesion nematodes, and dagger nematodes in various agricultural crops. The mode of action of flufensulfone involves interfering with the nervous systems of nematodes, leading to paralysis and death. By targeting nematodes, flufensulfone helps reduce their populations and minimize the damage they can cause to crops. Flufensulfone was priced at USD 19.0 thousand metric ton in 2022.

- Abamectin is known for its nematocidal activity against several plant-parasitic nematodes, including the root lesion nematode (Pratylenchus penetrans), the reniform nematode (Rotylenchus reniformis), the root-knot nematode (Meloidogyne incognita), and the cyst nematodes (Heterodera schachtii). Its efficacy in controlling these nematodes makes it a valuable tool for nematode management in agricultural crops. As of 2022, the market value of abamectin was approximately USD 12.2 thousand per metric ton.

- Oxamyl is a widely used insecticide and nematicide belonging to the chemical class of carbamates. It is primarily used to control a variety of plant-parasitic nematodes in agricultural crops. Oxamyl's mode of action as an insecticide and nematicide involves inhibiting the activity of acetylcholinesterase, an enzyme essential for nerve function in insects and nematodes. By disrupting this enzyme, oxamyl causes nerve overstimulation, leading to paralysis and eventual death of the pests. It was priced at USD 8.8 thousand per metric ton in 2022.

Nematicide Industry Overview

The Nematicide Market is fairly consolidated, with the top five companies occupying 85.65%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, Syngenta Group and Upl Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Canada

- 4.3.3 China

- 4.3.4 France

- 4.3.5 Germany

- 4.3.6 India

- 4.3.7 Indonesia

- 4.3.8 Italy

- 4.3.9 Japan

- 4.3.10 Mexico

- 4.3.11 Myanmar

- 4.3.12 Netherlands

- 4.3.13 Pakistan

- 4.3.14 Philippines

- 4.3.15 Russia

- 4.3.16 South Africa

- 4.3.17 Spain

- 4.3.18 Thailand

- 4.3.19 Ukraine

- 4.3.20 United Kingdom

- 4.3.21 United States

- 4.3.22 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 Albaugh LLC

- 6.4.3 American Vanguard Corporation

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 Syngenta Group

- 6.4.7 Tessenderlo Kerley Inc. (Novasource)

- 6.4.8 Upl Limited

- 6.4.9 Vive Crop Protection

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms