北米の殺線虫剤市場:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Nematicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 184 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683206

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

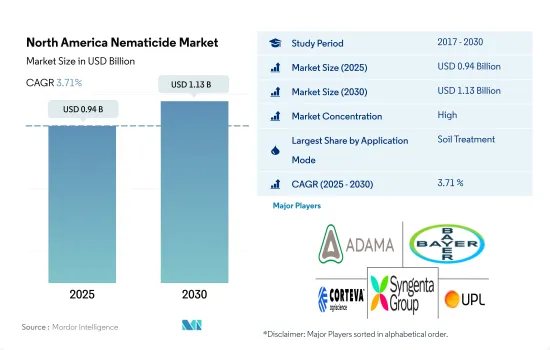

北米の殺線虫剤市場規模は2025年に9億4,000万米ドルと予測され、2030年には11億3,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 3.71%で成長すると予測されます。

土壌用途が殺線虫剤市場を独占

- 北米では、経済的に重要な幅広い作物を襲う様々な種類の線虫が存在するため、殺線虫剤の需要が増加しています。植物寄生性線虫は、単独で被害をもたらすだけでなく、他の微生物と病害複合体を形成し、作物の損失を増大させています。線虫による年間作物損失は米国で80億米ドルと推定されています。殺線虫剤は、害虫タイプや作物の生育ステージに応じて、さまざまな方法で散布することができます。

- 葉面散布(線虫剤を植物の葉に直接散布する)などの他の散布方法と比較すると、線虫の土壌散布は一般的に、有益な昆虫や受粉媒介者を含む非標的生物に暴露するリスクが少ないです。このため、土壌施用が70.7%のシェアを占め、2022年の市場規模は5億9,870万米ドルとなりました。

- 葉面散布は、2022年の北米線虫市場の10.9%を占めました。葉面散布の主要目的は、線虫による花序と葉の侵入を制御することです。例えば、キク線虫は白米穂先病の原因となる葉面線虫であり、サマークリンプ線虫は穀類の春季萎黄病の原因となります。

- 線虫の蔓延による作物の損失は年々増加しており、農業従事者にとって大きな懸念となっており、線虫駆除剤の使用を余儀なくされています。そのため、この市場は予測期間中にCAGR 3.2%を記録すると予測されています。

北米の農業従事者は、作物の健康と収量の最大化のために線虫管理に重点を置いており、これが市場を牽引します。

- 北米には多様な農業セグメントがあります。線虫は、穀物、果物、野菜、特殊作物などの主要作物を含む幅広い作物に影響を与える可能性があります。その結果、線虫の個体数を防除し、作物の損失を軽減するための線虫駆除剤の需要が高まっています。2022年、この地域は世界の殺線虫剤市場の30.7%の市場シェアを占めています。

- 米国は殺線虫剤の主要消費国です。線虫は作物に大きなダメージを与え、収穫量の損失や経済的な影響をもたらします。農業従事者は、作物の健康状態を最適に保ち、収量を最大化するための線虫管理の重要性を認識しています。その結果、米国では線虫駆除剤の需要が旺盛で、北米市場での主要シェアに貢献しています。

- メキシコの殺線虫剤市場は急速な成長を遂げています。2023~2029年のCAGRは5.2%と予測されています。メキシコは、この地域における主要な農産物輸出国のひとつです。メキシコは国際市場の厳しい品質基準や要件を満たすことを目指しているため、農作物の線虫個体数を効果的に管理する必要性が高まっています。メキシコ産農産物の輸出需要の高まりが同国の線虫剤市場の成長を牽引しており、北米で最も急成長している市場の一つとなっています。

- 農業従事者の意識の向上、農業技術の進歩、農業の拡大といった要因が殺線虫剤市場の成長に寄与しています。そのため、北米の殺線虫剤市場は予測期間中(2023~2029年)にCAGR 3.9%を記録すると予測されています。

北米の殺線虫剤市場動向

単作農と不耕起栽培が線虫密度を増殖させ、その結果、1ヘクタール当たりの殺線虫剤消費量が増加

- 近年、北米では1ヘクタール当たりの殺線虫剤消費量が顕著に増加しています。2022年には、この消費量は2017年に記録されたレベルと比較して1ヘクタール当たり4gと大幅に増加しました。この増加傾向の主要原動力は、線虫を駆除するための殺線虫剤への依存度が高まっていることです。

- 2022年には、米国が殺線虫剤の大幅な消費量で際立っており、1ヘクタール当たり82.9 gに達し、他国を大きく上回りました。この顕著な増加は主に、線虫の個体数の増殖を促進する様々な要因により、殺線虫剤の需要が高まり、使用量が増加したことに起因すると考えられます。この増加傾向の要因のひとつは、土壌攪乱を減らし作物残渣の保持を高める不耕起栽培の採用です。しかし、不耕起栽培は土壌中の線虫数を増加させています。

- 特に、小麦(68%)、トウモロコシ(76%)、綿花(43%)、大豆(74%)といった主要作物では、不耕起農法がかなり採用されており、殺線虫剤の必要性がさらに高まっています。同国の熱帯・亜熱帯地域では、主に単作農法が採用されており、これらの地域では温暖で湿度が高いため、線虫の生育に適した環境となっています。そのため、1ヘクタール当たりの殺線虫剤の使用量は増加しています。

- カナダ、メキシコ、その他の北米地域では、1ヘクタール当たりの殺線虫剤使用量にほとんど変化はないです。気候の変化、土壌条件、その他の農業プラクティスが線虫の増加の理由であり、ha当たりの殺線虫剤の消費量をさらに増加させています。

フルエンスルホンは需要が高いため、他の殺線虫剤の中で最も高い価格となっています。

- 線虫は農作物に大きな被害を与え、収量減と経済的影響をもたらします。農業従事者は、作物の健康状態を最適に保ち、収量を最大化するための線虫管理の重要性を認識しています。米国はこの地域における線虫駆除剤の主要な消費国です。

- フルエンスルホンはフルオロアルキル系化学品に分類され、植物寄生性線虫を防除するために農業で使用されています。フルエンスルホンの作用機序は、線虫や昆虫の神経系を破壊して麻痺させ、最終的に死に至らせるというものです。野菜、果物、観賞用植物などさまざまな作物に使用され、これらの害虫による被害を軽減することで作物の収量と品質を向上させています。フルエンスルホンの2022年の価格は1トン当たり1万9,100米ドルでした。

- アバメクチンは種子処理に利用される浸透性殺線虫剤で、根こぶ線虫の防除を含め、線虫による初期成長期の根の感染を最小限に抑える効率的な解決策を記載しています。アバメクチンの有効成分コストは上昇傾向にあり、2022年にはトン当たり12.3米ドルに達します。

- オキサミルはカルバマート系殺虫・殺線虫剤で、さまざまな線虫の駆除によく使われます。オキサミルは野菜、果物、観賞用植物などの作物に散布され、かじったり吸ったりする昆虫や植物の根を攻撃する線虫による被害から作物を守る。オキサミルは、これらの害虫の神経系を混乱させ、麻痺させ、最終的に死に至らせることで効果を発揮します。顆粒や濃縮液などさまざまな製剤があり、対象となる害虫や作物に応じて土壌や葉に散布されます。オキサミルは2022年に1トン当たり8,600米ドルと評価されました。

北米の殺線虫剤産業概要

北米の殺線虫剤市場はかなり統合されており、上位5社で89.63%を占めています。この市場の主要企業は、ADAMA Agricultural Solutions Ltd、Bayer AG、Corteva Agriscience、Syngenta Group、Upl Limitedです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション(市場規模(単位:米ドル、数量)、2030年までの予測、成長見込みの分析を含む)

- 用途モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- Albaugh LLC

- American Vanguard Corporation

- Bayer AG

- Corteva Agriscience

- Syngenta Group

- Tessenderlo Kerley Inc.(Novasource)

- Upl Limited

- Vive Crop Protection

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 64569

The North America Nematicide Market size is estimated at 0.94 billion USD in 2025, and is expected to reach 1.13 billion USD by 2030, growing at a CAGR of 3.71% during the forecast period (2025-2030).

Soil application dominated the nematicide market

- The demand for nematicides has been increasing due to the presence of various nematode species attacking the wide range of economically important crops in North America. Plant parasitic nematodes cause damage individually and form disease complexes with other microorganisms, thereby increasing crop loss. Annual crop losses due to nematodes are estimated at USD 8.0 billion in the United States. Nematicides can be applied through different methods depending on the type of pest and growth stage of the crop.

- Compared to other application methods, such as foliar application (spraying the nematicide directly onto the plant leaves), soil application of nematodes generally poses fewer risks of exposing non-target organisms, including beneficial insects and pollinators, as the nematicide remains primarily in the soil, where the target nematodes reside. Owing to this, soil application dominated the market with a share of 70.7%, valued at USD 598.7 million in 2022.

- Foliar applications accounted for 10.9% of the North American nematicide market in 2022. The main purpose of foliar application is to control the infestation of inflorescence and leaves by the nematodes. For instance, chrysanthemum nematodes are foliar nematodes that cause white rice tip, and summer crimp nematodes cause spring dwarf diseases in cereal crops.

- The crop losses due to nematode infestation are increasing every year, acting as a major concern for farmers and forcing them to use nematicides. Therefore, the market is anticipated to register a CAGR of 3.2% during the forecast period.

North American farmers' emphasis on nematode management for optimal crop health and yield maximization will drive the market

- North America has a diverse agricultural sector. Nematodes can impact a wide range of crops, including major commodities like grains, fruits, vegetables, and specialty crops. As a result, there is a growing demand for nematicides to control nematode populations and mitigate crop losses. In 2022, the region accounted for 30.7% market share value of the global nematicide market.

- The United States is a major consumer of nematicide products. Nematodes can cause substantial damage to crops, leading to yield losses and economic impact. The farmers recognize the importance of nematode management to ensure optimal crop health and maximize yields. As a result, there is a strong demand for nematicide products in the United States, contributing to its major share in the North American market.

- Mexico is experiencing rapid growth in its nematicide market. It is anticipated to register a CAGR of 5.2% during 2023-2029. Mexico is one of the leading exporters of agricultural products in the region. As Mexico aims to meet the stringent quality standards and requirements of international markets, there is an increasing need to effectively manage nematode populations in crops. The rising export demand for Mexican agricultural products is driving the growth of the nematicide market in the country, making it one of the fastest-growing markets in North America.

- Factors such as increasing awareness among farmers, advancements in agricultural technologies, and expansion of agriculture contribute to the growth of the nematicide market. Therefore, the North American nematicide market is expected to register a CAGR of 3.9% during the forecast period (2023-2029).

North America Nematicide Market Trends

Monoculture and no-tillage practices proliferate the nematode density, resulting in increased consumption of nematicides per ha

- In recent years, there has been a notable growth in the consumption of nematicide per hectare in North America. In 2022, this consumption witnessed a considerable increase of 4 g per ha compared to the levels recorded in 2017. The primary driving force behind this upward trend is the growing dependency on nematicides to control nematodes.

- In 2022, the United States stood out with a substantial consumption of nematicide, reaching 82.9 g per ha, which was significantly higher than other countries. This notable increase can be primarily attributed to various factors promoting the proliferation of nematode populations, leading to a higher demand for nematicides and increased usage levels. One of the contributing factors to this upward trend is the adoption of no-tillage practices, which reduce soil disturbance and increase the retention of crop residue. However, this practice also inadvertently results in a higher nematode population in the soil.

- Notably, major crops like wheat (68%), corn (76%), cotton (43%), and soybeans (74%) have recorded considerable adoption of no-tillage methods, further intensifying the need for nematicides. The country's tropical and subtropical regions predominantly adopt monoculture agricultural practices, and the warm and humid conditions in these areas create favorable environments for nematode growth. Therefore, the utilization of nematicides per ha is growing.

- There is a minimal change in the consumption of nematicides per ha in Canada, Mexico, and the Rest of North America. Climate changes, soil conditions, and other agricultural practices are reasons for nematodes' growth, further increasing the consumption of nematicides per ha.

Fluensulfone was priced highest among other nematicides due to the high demand

- Nematodes can cause substantial damage to crops, leading to yield losses and economic impact. The farmers recognize the importance of nematode management to ensure optimal crop health and maximize yields. The United States is a major consumer of nematicide products in the region.

- Fluensulfone falls under the fluoroalkyl chemical class and is used in agriculture to control plant-parasitic nematodes. Fluensulfone's mode of action involves disrupting the nervous systems of nematodes and insects, leading to their paralysis and eventual death. It is used in a variety of crops, including vegetables, fruits, and ornamental plants, to enhance crop yield and quality by reducing the damage caused by these pests. Fluensulfone was priced at USD 19.1 thousand per metric ton in 2022.

- Abamectin is a systemic nematicide utilized for seed treatment, providing an efficient solution to minimize early-growth root infections caused by nematodes, including controlling root-knot nematode species. The cost of abamectin's active ingredient has been on the rise, reaching USD 12.3 per metric ton in 2022.

- Oxamyl is a carbamate insecticide and nematicide that is commonly used to control a variety of nematodes. It is applied to crops like vegetables, fruits, and ornamental plants to protect them from damage caused by chewing and sucking insects, as well as nematodes that attack the plant roots. Oxamyl works by disrupting the nervous system of these pests, leading to paralysis and eventual death. It is available in various formulations, including granules and liquid concentrates, and is applied to the soil or foliage depending on the target pests and crops. Oxamyl was valued at USD 8.6 thousand per metric ton in 2022.

North America Nematicide Industry Overview

The North America Nematicide Market is fairly consolidated, with the top five companies occupying 89.63%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group and Upl Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 Albaugh LLC

- 6.4.3 American Vanguard Corporation

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 Syngenta Group

- 6.4.7 Tessenderlo Kerley Inc. (Novasource)

- 6.4.8 Upl Limited

- 6.4.9 Vive Crop Protection

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

北米の殺線虫剤市場:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 184 Pages

- 納期

- 2~3営業日