アジア太平洋の殺線虫剤市場:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia Pacific Nematicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 205 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683205

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

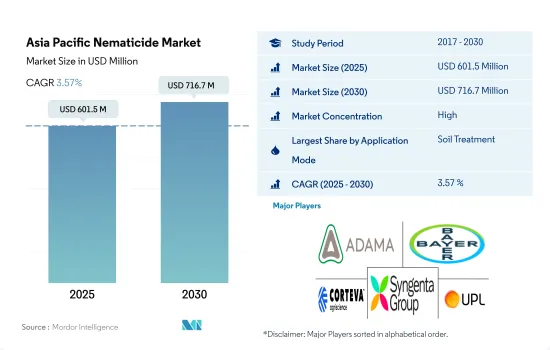

アジア太平洋の殺線虫剤市場規模は、2025年には6億150万米ドルと予測され、2030年には7億1,670万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.57%で成長すると予測されます。

非標的生物への暴露リスクが少ないことから、土壌施用型殺線虫剤が市場を席巻

- 植物の一部を食害する線虫は植物寄生線虫(PPN)と呼ばれます。線虫駆除剤は、葉面散布、化学散布、土壌処理など、さまざまな散布方法を通じてこれらの線虫を防除するために使用されます。

- 葉面散布など他の散布方法と比較すると、一般に、線虫剤の土壌散布は、有益な昆虫や花粉媒介者を含む非標的生物に暴露するリスクが少ないです。というのも、殺線虫剤は主に土壌中に留まり、標的線虫が生息しているからです。このため、土壌施用が2022年には69.3%のシェアを占め、市場を独占しています。

- 葉面散布は2022年にアジア太平洋の殺線虫剤市場の12.8%を占めました。葉面散布の主要目的は、小麦などの穀類の原因線虫としても知られるAnguina triticiなどの線虫による花序への侵入や葉への侵入を防除することです。葉面散布は、臭化メチル、オキサミル、パラチオンなどの有効成分を使用するため、線虫に対して効果的です。

- 化学灌漑は2022年のアジア太平洋の線虫剤市場の8.0%を占めました。中国が化学灌漑セグメントで36.2%の市場シェアを占め、2022年の市場規模は1,640万米ドルでした。穀類シスト線虫Heterodera avenaeは、中国の青海チベット高原と黄河地域における主要な線虫害虫の1つで、小麦などの主要作物で10~90%の収量損失を引き起こすと報告されています。

- 線虫の侵入による農作物の損失は年々増加しており、農業従事者にとって大きな問題となっています。

食糧需要の増加による農作物保護の必要性が市場成長の原動力となっています。

- 農業が盛んで食糧需要が増加しているアジア太平洋では、線虫の侵入から作物を守るために殺線虫剤の使用が増加しています。2022年には、この地域は金額ベースで世界の作物保護市場の19.8%を占めました。

- この地域は農業が盛んで、中国、インド、日本、オーストラリアなどが主要な貢献国です。農業従事者は需要の増加に対応し、作物の品質を確保するため、線虫から作物を保護する対策を採用しており、市場の成長を促進しています。

- 同市場は2023~2029年にかけて1億3,890万米ドルの成長が見込まれています。農業従事者は、線虫が作物の収量に及ぼす悪影響について認識を深めています。線虫の蔓延は、生産性の低下、成長の阻害、さらには不作につながる可能性があります。このような認識から、農業従事者は作物を守るために線虫駆除剤に投資するようになっています。

- 特にインドネシア、タイ、中国、インドなどの国々では、商業的農業の拡大が線虫剤の需要を押し上げています。大規模な農業経営では、限られた場所に作物が集中するため、線虫の侵入を受けやすいです。そのため、営利目的の農業従事者は作物を保護し、より高い収量を確保するために、しばしば殺線虫剤に頼っています。

- アジア太平洋の殺線虫剤市場は、農産物需要の増加、線虫による農作物の損失に対する意識の高まり、商業的農業の拡大により、予測期間中(2023~2029年)に金額ベースでCAGR 3.8%を記録すると予測されます。この地域の農業がさらに発展し、線虫の蔓延がもたらす課題に対処するにつれて、こうした動向は今後も続くと予想されます。

アジア太平洋の線虫剤市場動向

線虫駆除の重要性に対する農業従事者の意識の高まりが、殺線虫剤の散布を増加させています。

- 日本は1ヘクタール当たりの線虫剤消費量が最大で、2022年の農地1ヘクタール当たりの平均消費量は478.7グラムです。しかし、日本はこの地域の農地全体の0.45%を占めるにすぎず、2022年にはわずか290万ヘクタールにすぎないです。日本では、ハウス栽培や単作などの集約的農法が普及しています。こうした農法は生産性を最大化するという利点がある一方で、線虫のような土壌伝染性害虫に対する作物の脆弱性を高めるため、日本の農業従事者は作物を守るために線虫駆除剤に頼るようになります。

- オーストラリアは1ヘクタール当たりの殺線虫剤の消費量が2番目に多く、2022年には1ヘクタール当たり63.6グラムを消費します。これは、オーストラリアの生産者や芝管理者にとって、植物寄生性線虫がもたらす莫大な隠れたコストが原因であると考えられます。オーストラリアでは、最大1,900万ヘクタールの耕作地とアメニティ芝が寄生線虫の悪影響を受け、年間3億米ドルの損失を被っていると推定されています。

- オーストラリアに続くのはフィリピンとベトナムで、2022年の殺線虫剤使用量はそれぞれ1ヘクタール当たり46.3グラムと41.1グラムです。フィリピンでは根こぶ線虫が大きな問題となっています。特にトマトのような野菜作物では、栽培品種や地域にもよりますが、20%から85%の損失をもたらすことが知られています。

- 中国、タイ、ミャンマー、インドは、この地域で線虫駆除剤を大量に消費している他の国々であり、線虫の蔓延が増加しているためです。しかし、農業従事者の意識が高まり、農作物を保護する必要性が高まるにつれ、殺線虫剤の使用量は増加しています。

線虫の侵入による農作物の損失は年々増加しており、殺線虫剤の価格にも影響を及ぼしています。

- 植物寄生線虫(PPN)は、食糧安全保障と植物の健康にとって最も悪名高く、過小評価されている脅威のひとつです。例えばインドでは、主要な植物寄生性線虫による年間作物損失は19.6%、2,421億インドルピーと推定されています。野菜栽培では、植物寄生線虫は主要害虫のひとつとされています。フルエンスルホン、アバメクチン、オキサミルはアジア太平洋で一般的に使用されている殺線虫剤です。

- フルエンスルホンは2022年に1トン当たり1万9,000米ドルと評価されました。フルエンスルホンは、根こぶ線虫(Meloidogyne spp.)、ポテトシスト線虫、針線虫、披針線虫、刺線虫、矮性根線虫(Trichodorus spp.とParatrichodorus spp.)、病斑線虫などの線虫を抑制するために使用されます。

- アバメクチンは、根病線虫(Pratylenchus penetrans)、腎状線虫(Rotylenchulus reniformis)、根こぶ線虫(Meloidogyne incognita)、シスト線虫(Heterodera schachtii)など、いくつかの植物寄生線虫に対して殺線虫活性があることが知られています。アバメクチンは2022年に1トン当たり1万2,200米ドルと評価されました。

- オキサミルはカルバマート系殺線虫剤で、液体と粒状で製造されています。Oxamylは下方に移動する全身活性を持つ唯一の殺線虫剤であるため、Pratylenchus線虫の減少に役立つ葉面殺線虫用途があります。オキサミルは2022年に1トン当たり8,700米ドルと評価されました。

- 線虫の侵入による農作物の損失は年々増加しており、農業従事者にとって大きな懸念事項となっているため、農作物を保護するために線虫駆除剤を使用せざるを得なくなっています。この要因は、殺線虫剤の価格に影響を与えると予想されます。

アジア太平洋の殺線虫剤産業概要

アジア太平洋の殺線虫剤市場はかなり統合されており、上位5社で86.26%を占めています。この市場の主要企業は、ADAMA Agricultural Solutions Ltd、Bayer AG、Corteva Agriscience、Syngenta Group、UPL Limitedです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- アプリケーションモード

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- Bayer AG

- Corteva Agriscience

- Syngenta Group

- UPL Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 64382

The Asia Pacific Nematicide Market size is estimated at 601.5 million USD in 2025, and is expected to reach 716.7 million USD by 2030, growing at a CAGR of 3.57% during the forecast period (2025-2030).

Soil application of nematicides dominated the market owing to fewer risks of exposing non-target organisms

- Nematodes that feed on plant parts are called plant parasitic nematodes (PPN). Nematicides are used to control these nematodes through various application methods like foliar application, chemigation, and soil treatment.

- Compared to other application methods, such as foliar application, soil application of nematicides generally poses fewer risks of exposing non-target organisms, including beneficial insects and pollinators. This is because the nematicide remains primarily in the soil, where the target nematodes reside. Owing to this, soil application dominated the market with a share of 69.3% in 2022.

- Foliar applications accounted for 12.8% of the Asia-Pacific nematicide market in 2022. The main purpose of the foliar application is to control the infestation of inflorescence and the infestation of leaves by nematodes such as the Anguina tritici (seed gall nematode), also known as seed gall disease-causing nematodes, which are present in cereals such as wheat. Foliar application is effective against nematodes due to the use of active ingredients like methyl bromide, Oxamyl, and parathion.

- Chemigation accounted for 8.0% of the Asia-Pacific nematicide market in 2022. China dominated the chemigation segment with a market share of 36.2%, valued at USD 16.4 million in 2022. The cereal cyst nematode, Heterodera avenae, is one of the major nematode pests in the Qinghai-Tibetan Plateau and Yellow River regions of China; it is reported to cause 10-90% yield losses in major crops like wheat.

- Crop losses due to nematode infestation are increasing every year and are acting as a major concern for farmers, forcing them to use nematicides in order to protect the crops.

The need to protect the crops due to rising food demand is driving the growth of the market

- Asia-Pacific, with its large agricultural industry and increasing demand for food, has witnessed a rise in the use of nematicides to protect crops from nematode infestations. In 2022, the region accounted for 19.8% of the global crop protection market by value.

- The region has a substantial agricultural industry, with countries like China, India, Japan, and Australia being major contributors. Farmers are adopting measures to protect their crops from nematodes to meet the growing demand and ensure the quality of crops, thus driving the market's growth.

- The market is expected to grow by USD 138.9 million during 2023-2029. Farmers are becoming more aware of the detrimental effects of nematodes on crop yields. Nematode infestations can lead to reduced productivity, stunted growth, and even crop failure. This awareness has prompted farmers to invest in nematicides to protect their crops.

- The expansion of commercial farming, particularly in countries like Indonesia, Thailand, China, and India, has driven the demand for nematicides. Large-scale farming operations are more susceptible to nematode infestations due to the concentration of crops in a confined area. Therefore, commercial farmers often rely on nematicides to protect their crops and ensure higher yields.

- The Asia-Pacific nematicide market is projected to register a CAGR of 3.8% by value during the forecast period (2023-2029) due to the increasing demand for agricultural products, rising awareness about nematode-related crop losses, and expansion of commercial farming. These trends are expected to continue as the region's agricultural industry further develops and addresses the challenges posed by nematode infestations.

Asia Pacific Nematicide Market Trends

Growing awareness among farmers about the importance of nematode control is increasing the application of nematicides

- Japan is the largest consumer of nematicides per hectare, with an average consumption of 478.7 grams per hectare of agricultural land in 2022. However, Japan only accounted for 0.45% of the total agricultural land in the region, with just 2.9 million hectares in 2022. Intensive farming practices, such as greenhouse cultivation and monocropping, are prevalent in Japan. While these practices have their advantages in maximizing productivity, they also increase the vulnerability of crops to soil-borne pests like nematodes, leading the farmers in Japan to rely on nematicides to safeguard their crops.

- Australia is the second-highest consumer of nematicides per hectare, with a consumption of 63.6 grams per hectare in 2022. This could be attributed to the huge hidden cost posed by plant parasitic nematodes to Australian producers and turf managers. It has been estimated that up to 19 million hectares of cultivated land and amenity turf are negatively impacted by parasitic nematodes in Australia, resulting in annual losses of USD 300 million.

- Australia is closely followed by the Philippines and Vietnam, with nematicide consumptions of 46.3 and 41.1 grams per hectare, respectively, in 2022. Root-knot nematode is a major problem in the Philippines. It is known to cause losses between 20% and 85%, especially in vegetable crops like tomatoes, based on the cultivar and region grown.

- China, Thailand, Myanmar, and India are other countries in the region that consume significant amounts of nematicides, owing to the increasing incidences of nematode infestation, which are often neglected by the farmers because of their hidden nature. However, the usage of nematicides is increasing with growing awareness among farmers and the need to protect the crops.

Crop losses due to nematode infestation are increasing every year, influencing the prices of nematicides

- Plant parasitic nematodes (PPNs) are among the most notorious and underrated threats to food security and plant health. For instance, in India, the annual crop losses due to major plant parasitic nematodes are estimated to be 19.6%, valued at INR 242.1 billion. In vegetable cultivation, plant parasitic nematodes are considered among the major pests. Fluensulfone, Abamectin, and Oxamyl are commonly used nematicides in Asia-Pacific.

- Fluensulfone was valued at USD 19.0 thousand per metric ton in 2022. It can be used to suppress nematodes, including root-knot nematodes (Meloidogyne spp.), potato cyst nematodes, needle nematodes, lance nematodes, sting nematodes, stubby root nematodes (Trichodorus and Paratrichodorus spp.), and lesion nematodes.

- Abamectin is known to have nematicidal activity against some plant parasitic nematodes, including the root lesion nematode (Pratylenchus penetrans), the reniform nematode (Rotylenchulus reniformis), the root-knot nematode (Meloidogyne incognita), and the cyst nematode (Heterodera schachtii). Abamectin was valued at USD 12.2 thousand per metric ton in 2022.

- Oxamyl is a carbamate nematicide that is manufactured in liquid and granular forms. Oxamyl is the only nematicide with downward-moving systemic activity; thus, it has foliar nematicidal applications that help to reduce Pratylenchus nematodes. Oxamyl was valued at USD 8.7 thousand per metric ton in 2022.

- Crop losses due to nematode infestation are increasing every year and are acting as a major concern for farmers, forcing them to use nematicides in order to protect the crops. This factor is expected to influence the prices of nematicides.

Asia Pacific Nematicide Industry Overview

The Asia Pacific Nematicide Market is fairly consolidated, with the top five companies occupying 86.26%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Syngenta Group

- 6.4.6 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋の殺線虫剤市場:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 205 Pages

- 納期

- 2~3営業日