冷凍食品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Frozen Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044110

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

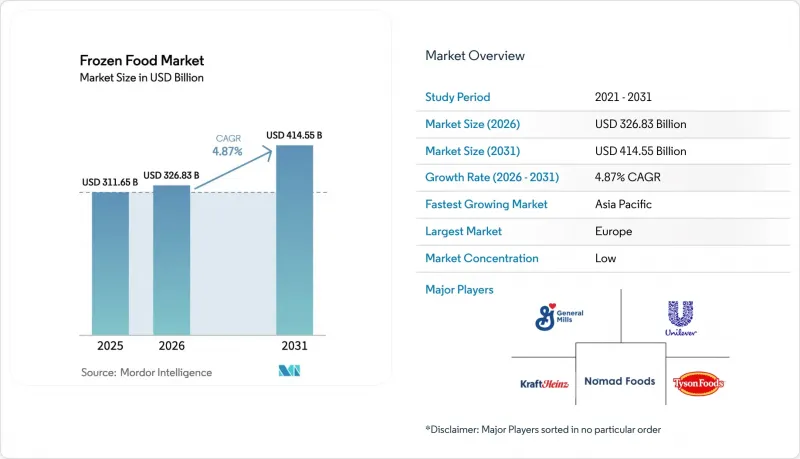

2026年に3,268億3,000万米ドルと評価された世界の冷凍食品市場は、2031年までに4,145億5,000万米ドルに成長し、CAGRは4.87%になると予測されています。

市場の成長は、品質と栄養価を維持しつつ調理時間を短縮できる、便利で保存期間の長い食品に対する消費者の需要の高まりによって牽引されています。個別急速冷凍(IQF)などの技術的進歩により、製品の食感、風味、および栄養素の保持が向上しており、冷凍食品に対する消費者の受容度が高まっています。さらに、近代的な小売店やEコマースプラットフォームの拡大、および温度管理された物流により、製品の入手しやすさが向上しています。加えて、新興経済国におけるコールドチェーンインフラへの投資増加により、冷蔵保管、輸送、および流通ネットワークが強化され、冷凍食品の効率的な供給が可能となり、世界の市場が着実に成長することを支えています。

世界の冷凍食品市場の動向と洞察

在宅での交流に伴う冷凍スナックの需要急増

ホームエンターテインメントの動向が消費者の習慣を形作り続ける中、小規模な集まりや社交イベントにおける冷凍スナックの需要が大幅に増加しており、それによって冷凍食品市場が強化されています。ミレニアル世代やZ世代の消費者は、年配の世代に比べて一口サイズの冷凍前菜にますます惹かれています。市場には、ピザ、スライダー、各種スナック食品など、利便性とバラエティの両方を提供するように設計された幅広い冷凍食品が揃っています。これらの製品は調理が簡単で、多様な味の好みに応えることができるため、社交の場に特に適しています。消費者がおもてなしの場で、効率性と風味豊かな選択肢を兼ね備えたソリューションをますます求めるにつれ、冷凍スナック市場は拡大しています。この成長は主に、便利でバラエティに富んだスナックを好むミレニアル世代とZ世代によって牽引されています。家庭でのエアフライヤーの普及が進んでいることも、この市場の拡大をさらに加速させています。冷凍食品メーカーは、エアフライヤーでの調理に特化した製品の開発に注力しているからです。戦略的な動きとして、2025年4月、マッケイン・フーズ・インディアはフィリップスと提携し、エアフライヤー用に最適化された一連の冷凍スナックを発売しました。これには、レストラン品質の味と食感を再現したクリスピーフライドポテトが含まれており、消費者に自宅で手軽に楽しめる食事ソリューションを提供しています。

食感を守った野菜を実現するIQF技術の急速な普及

個別急速冷凍(IQF)技術は、冷凍野菜市場に革命をもたらし、農産物の構造的完全性と栄養価の維持を保証しています。この技術の進歩により、アボカドや葉物野菜など、従来は冷凍が課題となっていたものを含め、多種多様な野菜の冷凍が可能になりました。保存品質の向上により、特に健康志向の消費者を中心に、冷凍野菜の消費量が大幅に増加しています。さらに、IQF技術は食品廃棄物の削減においても極めて重要な役割を果たしています。農産物の季節的な入手可能性を拡大し、サプライチェーン全体での腐敗を最小限に抑えることで、業界における重大な課題に対処しています。例えば、JBT Frigoscandia社の「FLoFREEZE」個別急速冷凍機は、高度な個別冷凍技術を採用しており、野菜、果物、魚介類、その他の高品質なIQF製品に対応しています。真の流動化機能を備えたこのシステムは、汎用性と高品質な成果の両方を保証します。さらに、JBTの「Sequential Defrost」技術により、Frigoscandia FLoFREEZEシリーズ-Mのラインアップでは、大幅な処理能力が実現されています。調整可能な気流設定により実用性がさらに向上し、多様なサイズや種類の製品に対応することが可能です。

冷凍SKUにおける持続可能な水産物の供給ギャップ

持続可能な方法で調達された水産物に対する消費者の需要が高まり続ける中、冷凍水産物メーカーは深刻なサプライチェーンの課題に直面しています。現在の市場需要は、海洋管理協議会(MSC)の認証を受けた水産物や、責任ある方法で漁獲された魚種の供給量を上回っています。この不均衡は、サーモン、エビ、タラなどの人気のある水産種において特に顕著です。これらの天然魚種の供給は、乱獲や気候変動の悪影響により、ますます厳しい状況に追い込まれています。冷凍食品業界では、確立された持続可能性基準を満たす水産物の著しい不足が生じています。例えば、北海のセイヨウコダラ漁業は、2025年6月末までに海洋管理協議会(MSC)の認証を失う見込みです。同月上旬にMSCが発表したこの認証停止は、資源生産性の低下が続いた結果によるものです。国際海洋調査評議会(ICES)が最近実施した評価により、資源量が持続可能な水準を下回っていることが確認されました。同地域における冷水性魚種の主要な供給源である北海のセイヨウタラ漁業は、この認証取得における後退に直面した最新の事例となります。

セグメント分析

2025年、調理用加工食品は市場シェアの63.32%を占め、圧倒的な存在感を示しました。これは、味付けや調理法を自分で決めたいと望みつつも、野菜の切り分けや肉のマリネといった作業にかかる時間を節約したいと考える消費者に支持されたためです。一方、即食(レディ・トゥ・イート)形式の製品は、年率5.27%という堅調な成長を見せており、この動向は2031年まで続くと予測されています。この急成長は、主にカスタマイズよりもスピードを優先する単身世帯や多忙な社会人に支えられています。このような相違は、カテゴリーの二極化を示しています。調理用製品は家族で一緒に夕食を計画する人々を対象としているのに対し、即食製品は手早い昼食や急な食事に焦点を当てています。

これに対応し、メーカー各社はカテゴリーの境界線をますます曖昧にしています。調理時間がわずか8分の下味付け済み生肉や、食感を引き立てるために軽く焼くだけでよい完全調理済み丼など、ハイブリッドな製品を次々と投入しています。このイノベーションの波は、アジア太平洋地域で最も顕著です。ここでは、日本のセブンーイレブンを代表とするコンビニエンスストアチェーンが、冷凍丼や麺類のキットを提供しており、顧客は店内で電子レンジで加熱できるため、小売スペースが事実上、準外食店舗へと変貌しています。規制面での考慮事項も重要な役割を果たしています。例えば、欧州連合(EU)の「ニュートリスコア(Nutri-Score)」制度では、パッケージ前面の表示において高ナトリウム含有量がペナルティ対象となるため、即食食品メーカーは製品の再配合を迫られています。これは、健康志向の消費者を遠ざける可能性のある低いスコアを回避するために不可欠です。一方、調理用食品は、調理中に塩を加えることでブランドが配合の柔軟性を高められるため、こうした規制の波をよりスムーズに乗り切ることができます。

地域別分析

欧州は、定着した冷凍食品の消費パターンと整備されたコールドチェーンインフラに支えられ、2025年には31.32%の市場シェアを占めています。この市場には、ドイツ、英国、フランス、スペイン、イタリア、ロシアなどの主要経済国が含まれており、それぞれが地域の市場力学に大きく寄与しています。欧州市場では、製品の革新、持続可能な包装ソリューション、およびプレミアム冷凍食品に重点が置かれています。

アジア太平洋地域は、2026年から2031年にかけてCAGR6.80%で最も急速な成長を示しています。冷凍食品業界は、急速な都市化、消費者のライフスタイルの変化、可処分所得の増加に牽引され、大きな成長の可能性を示しています。この地域には、中国、日本、インド、オーストラリアなどの主要市場が含まれており、それぞれが独自の市場特性と成長パターンを示しています。同地域では、コールドチェーンインフラの整備や小売ネットワークの拡大が著しく進展しており、冷凍食品市場の成長を支えています。アジア太平洋地域の消費者、特に第1級および第2級都市の消費者において、冷凍食品への受容度が高まっています。

北米の冷凍食品市場は、消費者のライフスタイルの変化や、手軽な食品への需要の高まりを背景に、堅調な成長を見せています。米国が地域市場を牽引し、カナダ、メキシコが続いていますが、各国で独自の消費パターンや市場力学が見られます。米国の冷凍食品業界では、消費者の嗜好に応えるため、メーカーが新製品バリエーションを導入するなど、プレミアム商品の拡充が進んでいます。例えば、2024年2月、Conagra社は、Bertolliブランドの冷凍食品セグメントを拡大し、Bertolliのオーブン調理用ミールと前菜を発売すると発表しました。オーブン調理用ミールには、チキンアルフレド、チキンパルミジャーナとペンネ、ミートボールリガトーニの3種類があります。前菜には、3種のチーズ入りトーストラビオリとアランチーニ・パルメザンがあり、これらはエアフライヤーでの調理に対応しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 在宅での交流を目的とした冷凍スナック食品の需要急増

- 食感の劣化を防ぐIQF技術の急速な普及

- 消費者直販(D2C)冷凍ミールキットの成長

- クリーンラベルの冷凍メインディッシュに対する需要の高まり

- 小売チャネルにおける冷凍食品売り場の拡大

- 植物由来冷凍食品への需要の高まり

- 市場抑制要因

- 冷凍SKU向け持続可能な水産物の供給ギャップ

- 冷蔵食品との比較における「鮮度ギャップ」に対する消費者の認識

- 原材料費の高騰

- 輸入冷凍食品に対する高関税

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品カテゴリー別

- 即食食品

- 調理用

- 製品タイプ別

- 冷凍果物・野菜

- 冷凍肉・魚介類

- 冷凍レディミール

- 冷凍スナック・ベーカリー

- 冷凍デザート

- その他の製品タイプ

- 流通チャネル別

- オントレード

- 小売(オフトレード)

- スーパーマーケットおよびハイパーマーケット

- コンビニエンスストア

- オンラインストア

- その他の小売形態

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Nestle S.A.

- Conagra Brands Inc.

- General Mills Inc.

- Nomad Foods Ltd.

- Tyson Foods Inc.

- McCain Foods Ltd.

- The Kraft Heinz Company

- Ajinomoto Co. Inc.

- Unilever PLC

- Hormel Foods Corp.

- Bellisio Foods Inc.

- Iceland Foods Ltd.

- Grupo Bimbo SAB de CV

- Charoen Pokphand Foods

- BRF S.A.

- Oetker Group

- Frosta AG

- NH Foods Ltd.

- Maple Leaf Foods Inc.

- CJ CheilJedang Corp.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日