殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 329 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685780

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

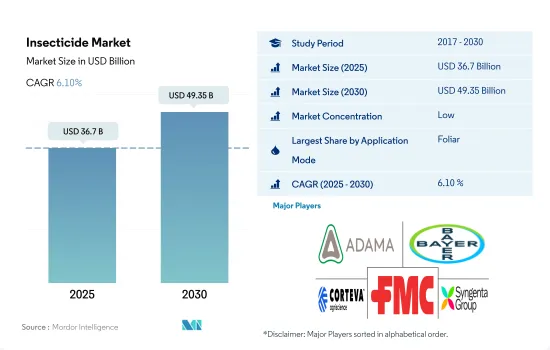

殺虫剤の市場規模は2025年に367億米ドルと推計され、2030年には493億5,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.10%で成長します。

害虫圧力の高まりと害虫から作物を守る必要性が殺虫剤需要を牽引している

- 殺虫剤の使用は、害虫から作物を守るためにさまざまな散布方法で増加しています。2022年には、葉面散布分野が殺虫剤市場全体の56.9%を占め、大きなシェアを占めています。これは害虫駆除圧力の増大と、害虫駆除効果、速効性、標的防除によるものと考えられます。

- 金額ベースでは、世界の殺虫剤市場における種子処理法のCAGRは2023年から2029年の間に4.5%を記録すると予想されています。この方法は、アブラムシ、アザミウマ、ヨトウムシ、カイガラムシなど、種子や苗を加害する多くの害虫を作物のライフサイクルの初期に防除できるため、主に採用されています。

- 殺虫剤市場における土壌処理は、2023年から2029年にかけてCAGR 4.1%を記録すると予想されます。小麦、大豆、アブラヤシ、ココア、コーヒーなど、経済的に重要な作物の根の成長に影響を及ぼす主な害虫は、ナメクジ、針金虫、フナクイムシ、土壌メアリ虫です。したがって、これらの害虫から作物を守るために、土壌処理という観点から殺虫剤の需要が増加すると予想されます。

- 農家の間では、化学灌漑法に対する意識が高まっています。殺虫剤の散布と灌漑を組み合わせることで、農家は時間と労力を節約することができ、大規模な農業経営を管理する農家にとって便利な選択肢となっています。これらの要因から、このアプリケーションモードにおける殺虫剤市場価値は、予測期間中(2023-2029年)に3.7%のCAGRで推移すると予測されています。

- これらの適用方法における世界の殺虫剤市場は大きな成長が見込まれ、2023年から2029年にかけてCAGR 4.2%を記録すると予測されます。

気候条件の変化に伴う作付面積の拡大が市場の成長に寄与している

- 世界人口の増加と食糧増産へのニーズが農業生産の拡大につながり、それが害虫から作物を守るための殺虫剤の需要を押し上げています。過去期間(2017~2022年)中、殺虫剤市場は84億4,980万米ドル成長した3。

- 南米は農業生産の主要地域のひとつであり、2022年の市場規模は24.9%でした。大豆、トウモロコシ、サトウキビ、その他の作物の膨大な生産量が、害虫を効果的に管理するための殺虫剤の大きな需要を生み出しています。ミナミキクイムシ(Spodoptera eridania)のような昆虫の侵入の増加が市場の成長を促進しています。

- 殺虫剤市場の金額シェアはアジア太平洋地域が最も大きく、予測期間(2023~2029年)のCAGRは3.9%を記録し、同地域で市場が最も急成長すると予測されています。農作物に被害を与える可能性のある害虫は、気候の変化により広がっています。その結果、殺虫剤はこれらの害虫に対処し、作物の生産性を確保するための効率的な手段であるため、需要の増加が見込まれています。

- 北米は予測期間中(2023~2029年)にCAGR 4.7%を記録すると予測されています。作物を保護する必要性と侵略的害虫の導入または蔓延が相まって、これらの新たな脅威を管理・駆除するための殺虫剤の需要が増加する可能性があります。

- しかし、欧州とアフリカは農業部門が充実しており、世界の殺虫剤市場で重要な役割を果たしています。これらの地域のCAGRは、期間中にそれぞれ4.6%と3.7%を記録すると予測されます。

- 世界の殺虫剤市場は、2023~2029年の間にCAGR 4.2%を記録すると予測されます。気候の変化に伴う農業セクターの急拡大が市場の成長を促進しています。

世界の殺虫剤市場動向

地球温暖化による害虫の増加で殺虫剤の使用量が増加

- 化学殺虫剤の世界平均消費量は農地1ヘクタール当たり918.7gです。これは、農業の集約化、害虫の増加、世界の食糧安全保障を確保するための高収量と作物生産性の必要性などの要因により、年々増加しています。国連食糧農業機関のデータによると、世界の農作物生産の40%が毎年害虫によって失われており、その経済的損失は平均約700億米ドルにのぼる。

- 欧州では世界の他の地域と比較して殺虫剤の使用量が多く、中でもドイツは1ヘクタール当たりの使用量が3,028.0 gと多くなりました。これは、作物の収量を最大化することに重点を置いた、非常に集約的な農法を行っているためと考えられます。集約的農業では、害虫を管理し、最適な作物生産を確保するために、殺虫剤を含む高投入量を使用することが多いです。欧州に続くのはアジア太平洋で、殺虫剤の平均散布量は1ヘクタール当たり975.1gです。

- 北米諸国の中では米国が1ヘクタール当たりの殺虫剤消費量が最も多く、2022年には791.7 gとなりました。これは作物の栽培面積が広く、常に変化する気候条件により害虫の侵入にさらされる機会が増えるためです。

- 地球温暖化による気候条件の変化は、特定の害虫にとって好条件を生み出し、深刻な大発生を引き起こしています。例えば、2020年に発生したイナゴの大発生では、23カ国、すなわち中東9カ国、北中東・アフリカ11カ国、南アジア3カ国が深刻な被害を受け、85億米ドルの損失が発生したと推定されています。このような状況により、農家は農業で殺虫剤を多量に使用しなければならなくなりました。

イミダクロプリドは最も手頃な価格の殺虫剤で、幅広い活性スペクトルを持っています。

- ラムダ-シハロトリンはピレスロイド系殺虫剤に属し、菊の花に含まれる天然ピレトリンをモデルにした合成化学物質です。ラムダ-シハロトリンは、綿、トウモロコシ、大豆、野菜、果実などの作物において、アブラムシ、アザミウマ、ヨコバイ、コナジラミ、各種イモムシなどの害虫駆除に使用されます。この有効成分は神経毒として作用し、昆虫の神経系を標的にします。神経細胞の正常な働きを阻害し、麻痺を引き起こし、最終的には害虫を死に至らしめる。2022年の価格は1トン当たり2万2,700米ドルでした。

- シペルメトリンは非合成ピレスロイド系で、ノミ・カブトムシ、ハクビシン、ゴキブリ、シロアリ、テントウムシ、サソリ、イエロージャケットの駆除に使用されます。2022年の価格は2万1,000米ドルでした。ブラジルはシペルメトリンの世界の輸入国トップ3に入り、EU-Mercosur協定により欧州連合がブラジルへの主要輸出国となっています。

- エマメクチン安息香酸塩はアベルメクチンという化学分類に属する殺虫剤です。神経系を標的として害虫を殺します。神経細胞の特定のレセプターに結合し、害虫を麻痺させ、最終的に死に至らしめる。エマメクチン安息香酸塩は欧州諸国で農業におけるさまざまな害虫駆除に使用されています。価格はトン当たり1万7,300米ドルです。

- イミダクロプリドはネオニコチノイド系殺虫剤で、アブラムシ、ヨコバイ、コナジラミ、アザミウマ、ある種の甲虫など、さまざまな害虫を効果的に駆除します。この有効成分の2022年の価格はトン当たり1万7,170米ドルでした。マラチオンは殺虫剤の中で最も手ごろな価格の化学物質です。2022年の価格は1トン当たり1万2,500米ドルでした。

殺虫剤業界の概要

殺虫剤市場は細分化されており、上位5社で33.15%を占めています。この市場の主要企業は以下の通りです。 ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- チリ

- 中国

- フランス

- ドイツ

- インド

- インドネシア

- イタリア

- 日本

- メキシコ

- ミャンマー

- オランダ

- パキスタン

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- ウクライナ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用方法

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 地域

- アフリカ

- 国別

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他欧州

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 47401

The Insecticide Market size is estimated at 36.7 billion USD in 2025, and is expected to reach 49.35 billion USD by 2030, growing at a CAGR of 6.10% during the forecast period (2025-2030).

The rising pest pressure and the need to protect crops from damaging insects are driving the demand for insecticides

- Insecticide use is increasing through different application modes to protect crops from insect pests. In 2022, the foliar segment held the major share, accounting for 56.9% of the overall insecticide market. This could be attributed to increasing pest pressure and its effectiveness in controlling insects, rapid action, and targeted control.

- In terms of value, the seed treatment method in the global insecticide market is expected to record a CAGR of 4.5% between 2023 and 2029. This method is being majorly adopted because it protects against many pests that attack seeds or seedlings, such as aphids, thrips, wireworms, and beetles, at the very beginning of a crop's life cycle.

- Soil treatment in the insecticide market is expected to record a 4.1% CAGR between 2023 and 2029. The main pests affecting the root growth of economically significant crops such as wheat, soybean, oil palm, cocoa, and coffee are slugs, wireworms, fungi gnats, and soil mealybugs. Therefore, to protect crops from these pests, the demand for insecticides in terms of soil treatment is expected to increase.

- Farmers are becoming more and more aware of the chemigation method. By combining insecticide application with irrigation, farmers can save time and labor, making it a convenient choice for farmers managing large-scale agricultural operations. Due to these factors, the insecticide market value in this application mode is projected to record a 3.7% CAGR during the forecast period (2023-2029).

- The global insecticide market in these application methods is expected to witness significant growth and is projected to record a 4.2% CAGR from 2023 to 2029.

The expansion of cropland areas with changes in climate conditions is contributing to the growth of the market

- The increase in global population and the need for higher food production have led to the expansion of agricultural production, which, in turn, boosted the demand for insecticides to protect the crops from damaging pests. During the historical period (2017-2022), the insecticide market grew by USD 8,449.8 million.3

- South America was one of the major regions in agriculture production, with a 24.9% market value in 2022. The vast production of soybeans, corn, sugarcane, and other crops creates a significant demand for insecticides to manage pests effectively. The rise of infestation of insects such as southern armyworm (Spodoptera eridania) has driven the growth of the market.

- Asia-Pacific holds the largest insecticide market value share, and the market is anticipated to grow fastest in the region, registering a CAGR of 3.9% during the forecast period (2023-2029). Insect pests that could damage crops are spreading due to the changing climate. Consequently, the demand for insecticides is expected to rise as they are efficient tools for addressing these pests and ensuring crop productivity.

- North America is projected to register a CAGR of 4.7% during the forecast period (2023-2029). The need to protect the crops, coupled with the introduction or spread of invasive pests, could lead to increased demand for insecticides to manage and control these new threats.

- However, Europe and Africa have a substantial agricultural sector and play a vital role in the global insecticide market. These regions are projected to register CAGRs of 4.6% and 3.7%, respectively, during the period.

- The global insecticide market is projected to register a CAGR of 4.2% during 2023-2029. The rapidly expanding agriculture sector with a changing climate is driving the growth of the market.

Global Insecticide Market Trends

Increased pest proliferation due to global warming is increasing the usage of insecticides

- The average global consumption of chemical insecticides is 918.7 g per hectare of agricultural land. It has been increasing over the years owing to factors like the intensification of agriculture, increasing pest populations, and the need for higher yield and crop productivity to ensure global food security. According to the data provided by the Food and Agriculture Organization, 40% of global crop production is lost to pests annually, resulting in an average economic loss of around USD 70.0 billion.

- Europe witnessed higher insecticide applications compared to other regions of the world, with Germany having a higher per-hectare consumption of 3,028.0 g, which may be attributed to its highly intensive agricultural practices, with a significant focus on maximizing crop yields. Intensive agriculture often involves the use of higher inputs, including insecticides, to manage pests and ensure optimal crop production. Europe is followed by Asia-Pacific, with an average insecticide application of 975.1 g per hectare.

- Among the North American countries, the United States witnessed the largest consumption of insecticides per hectare, with 791.7 g in 2022, attributed to the large area under the cultivation of crops and increased exposure to insect pest infestations due to constantly changing climatic conditions.

- Changing climatic conditions due to global warming have created favorable conditions for certain pests, resulting in severe outbreaks. For instance, a locust outbreak in 2020 severely affected 23 countries, i.e., nine in East Africa, 11 in North Africa and the Middle East, and three in South Asia, causing an estimated loss of USD 8.5 billion. These circumstances necessitate farmers to use higher amounts of insecticides in agriculture.

Imidacloprid is the most affordable insecticide with a broad spectrum of activity

- Lambda-cyhalothrin belongs to the class of pyrethroid insecticides, which are synthetic chemicals modeled after natural pyrethrins found in chrysanthemum flowers. Lambda-cyhalothrin is used to control pests such as aphids, thrips, leafhoppers, whiteflies, and various caterpillar species in crops like cotton, corn, soybean, vegetables, and fruits. This active ingredient acts as a neurotoxin, targeting the nervous system of insects. It disrupts the normal functioning of nerve cells, leading to paralysis and, ultimately, the death of the pests. In 2022, it was priced at USD 22.7 thousand per metric ton.

- Cypermethrin is a non-synthetic pyrethroid used to control flea beetles, boxelder bugs, cockroaches, termites, ladybugs, scorpions, and yellow jackets. It was priced at USD 21.0 thousand in 2022. Brazil ranks among the top three importers of cypermethrin globally, with the European Union being a major exporter to Brazil under the EU-Mercosur deal.

- Emamectin benzoate is an insecticide belonging to the chemical class of avermectins. It kills the pests by targeting the nervous system. It binds to specific receptors in nerve cells, leading to paralysis and the eventual death of the pests. Emamectin benzoate is majorly used in European countries to control various insect pests in agriculture. It was priced at USD 17.3 thousand per metric ton.

- Imidacloprid is a neonicotinoid insecticide used to effectively manage various pests, including aphids, leafhoppers, whiteflies, thrips, and certain beetle species. This active ingredient was priced at USD 17.17 thousand per metric ton in 2022. Malathion is the most affordable chemical among the insecticides. It was valued at USD 12.5 thousand per metric ton in 2022.

Insecticide Industry Overview

The Insecticide Market is fragmented, with the top five companies occupying 33.15%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 329 Pages

- 納期

- 2~3営業日