|

市場調査レポート

商品コード

1851253

クエン酸:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Citric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| クエン酸:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

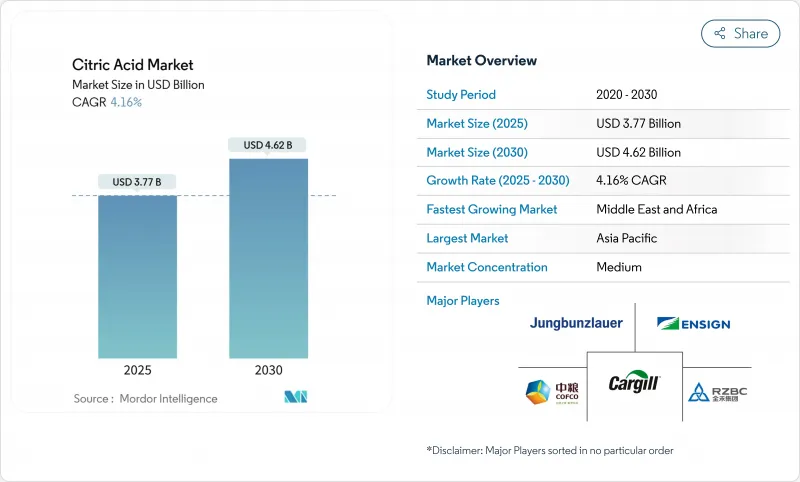

クエン酸の市場規模は、2025年には37億7,000万米ドルと予測され、2030年には46億2,000万米ドルに成長すると予測され、CAGRは4.16%と堅調に推移しています。

クリーンラベル製品に対する消費者の嗜好の高まり、バイオテクノロジー・プロセスの進歩、飲食品、医薬品、クリーニング製品などの産業における用途の多様化が、主にこの成長を後押ししています。米国でのGRASステータスや欧州連合(EU)での量子飽和承認を含む規制の明確化は、参入障壁を下げ続け、市場へのアクセスを促進し、新規参入企業の参入を促しています。しかし、中国からの輸入品に対する反ダンピング関税の賦課は、グローバルな調達戦略を再構築し、メーカーにサプライチェーンリスクを軽減するために中国以外の地域での生産能力拡大を促しています。さらに、サプライチェーン全体の垂直統合とエネルギー効率の高い発酵技術の革新により、生産効率とコスト効率が向上しています。コンビニエンス飲料、生分解性洗浄液、発泡性医薬品、その他の新興用途におけるクエン酸の需要の高まりは、市場範囲をさらに広げています。これらの要因から、クエン酸市場の潜在的な成長力と、進化する規制、技術、消費者主導の動向への適応能力が裏付けられています。

世界のクエン酸市場の動向と洞察

炭酸飲料における天然酸味料への消費者シフトの高まり

飲料業界が天然酸味料にシフトする中、クエン酸は、クリーンラベル製品への取り組みに後押しされ、需要の急増を目の当たりにしています。クエン酸は、ブラジルにおいて、Normative Instruction 211/2023により添加物として認可されました。この規則では、0.1%から0.3%の間で設定される飲料への一般的な添加量が規定されており、メーカーが切望していた指針を提供しています。このような規制の明確化は、配合の不確実性を払拭するだけでなく、ブランドが自然保存の信用を誇示する力を与えます。この動きは、成分表の透明性と簡素化を求める消費者の欲求の高まりと共鳴するものです。クエン酸の重要性は、天然酸味料としての主要な役割を超えています。pH調整剤および防腐剤としての付加的な機能により、メーカーは成分配合を合理化しながら製品の安定性を高めることができます。この戦略は、業界の包括的な目標である、規制ベンチマークの遵守と、クリーンラベル製品に対する消費者の要求との一致に合致しています。さらに、一流飲料メーカーは現在、医薬品グレードのクエン酸に傾倒しており、一貫した品質と市場コンプライアンスの重要性を強調しています。認証された高品質のクエン酸に対するこのような需要の高まりは、認証サプライヤーにプレミアム価格への道を開くだけでなく、市場における競争と革新の精神に火をつける。

レディ・トゥ・ドリンク飲料におけるクエン酸需要の増加

レディ・トゥ・ドリンク飲料市場は力強い成長を遂げており、様々な用途でクエン酸の需要を大きく牽引しています。クエン酸は、風味の強化、色の安定化、保存期間の延長など、製品の品質と魅力を維持するために重要な多機能特性を持つため、重要な成分となっています。新興市場における都市化の進展は、利便性を重視した消費習慣の導入を加速させ、レディ・トゥ・ドリンク飲料に大きな成長機会をもたらしています。フルーツ系飲料では、色調保持剤としてのクエン酸の役割が特に重要であり、視覚的アピール、消費者の嗜好、競合市場でのブランド差別化に直接影響するからです。さらに、発酵技術の進歩は生産能力を一変させました。製造業者は現在、アスペルギルス・ニガー(Aspergillus niger)の人工菌株を採用し、174g/Lを超えるクエン酸力価を達成しています。これらの技術革新は、生産効率を高め、操業コストを削減し、サプライチェーンの信頼性を向上させています。その結果、サプライヤーは、競争力のある価格設定を維持しながら需要の高まりに対応できる体制を整え、特に価格に敏感な新興セグメントでの市場拡大を促進しています。

新興国における原材料価格の変動

原材料コストの変動は、クエン酸のサプライチェーン全体に大きなマージン圧力となっており、トウモロコシ、サトウキビ糖蜜、その他の炭水化物源などの発酵基質が特に影響を受けています。この変動は新興市場において最も顕著であり、農産物価格は、予測不可能な天候、政策改革、地政学的緊張、インフラの不備などの外部要因の影響を非常に受けやすいです。投入コストの上昇だけでなく、メーカーは為替変動や物流費の増加にも悩まされており、これがコスト管理をさらに複雑にし、高度なヘッジ戦略の採用を必要としています。しかし、基質利用技術の進歩は、それを軽減する有望な道を提供しつつあります。最近の調査では、サトウキビのバガス、チーズの乳清、その他の製品別など、農業廃棄物の流れからクエン酸を生産することに成功しています。これらの技術革新は、一次産品市場への依存を減らすだけでなく、持続可能性の目標にも合致し、クエン酸のサプライチェーンの強靭性を強化する、費用対効果が高く、環境に優しい代替品を提供します。

セグメント分析

2024年、無水クエン酸は55.35%のシェアを占め、引き続き市場を独占しています。その優れた安定性、保存期間の延長、多様な最終用途を支える確立されたサプライチェーンインフラがその理由です。その結晶構造は安定した品質を保証するため、食品メーカーや製薬会社に好まれます。また、工業用途では、予測可能な溶解速度と製剤化プロセスにおける水分関連の課題が軽減されることから、無水形態が好まれています。しかし、加工効率が重要なファクターとなるにつれ、市場は徐々にシフトしています。Jungbunzlauer社のCITROCOAT Nのような直接圧縮可能なクエン酸は、医薬品の打錠で人気を集めています。これらの変種は、錠剤硬度の向上、加工時間の短縮、特定の用途における性能の向上により、業界のニーズに応えています。

液体クエン酸製剤は力強い成長を遂げており、2030年までのCAGRは6.82%と予測されています。この成長の原動力となっているのは、メーカーが業務効率とコストの最適化を重視するようになっていることです。液体製剤は溶解工程が不要なため、自動化された生産システムでの正確な投与制御が可能になり、製造工程が合理化されます。この動向は特に飲料業界で顕著であり、液体クエン酸はシロップ調製工程とシームレスに統合され、粉末の取り扱いに伴う汚染リスクを低減します。さらに、貯蔵・輸送技術の進歩により、従来の安定性に関する懸念が緩和され、液体形態の実現可能性がさらに高まっています。このような改善により、従来は無水タイプが主流であった用途での液体クエン酸の採用が拡大し、予測期間中の持続的成長が期待されています。

クエン酸市場レポートは、業界を形態別(無水および液体)、用途別(飲食品、医薬品、パーソナルケアおよび化粧品、その他)、グレード別(医薬品グレード、食品グレード、工業グレード)、地域別(北米、南米、欧州、アジア太平洋、中東アフリカ)に分類しています。各セグメントについて、市場セグメンテーションと予測は米ドルベースです。

地域別分析

2024年、アジア太平洋地域の市場シェアは37.74%に達するが、これは主に中国の堅調な生産能力と、食品加工および工業分野における国内需要の急増によるものです。この地域の利点には、確立された発酵インフラ、競争力のある生産コスト、トウモロコシやサトウキビ由来のような重要な原材料への近接アクセスが含まれます。しかし、貿易摩擦やアンチダンピング措置が、この地域の状況を変えつつあります。インド、タイ、その他の東南アジア諸国は、国内需要と輸出需要の両方に対応するため、生産能力を増強しています。日本の洗練された医薬品・食品加工部門は有利な市場展望を示し、オーストラリアの急成長する飲食品産業は地域の消費を後押しします。

中東・アフリカは注目すべき地域で、2030年までのCAGRは7.43%を誇る。この成長の主な要因は、サウジアラビアやアラブ首長国連邦などの国々で急成長する食品加工セクターとインフラ投資です。食料安全保障の強化や産業の多様化を目指すこの地域の政府の取り組みが、クエン酸の新たな需要ハブを生み出しています。NEOMがLiberation Labsと協力して精密発酵施設を設立したことは、この地域の高度バイオ製造における意欲を強調しています。一方、北米と欧州は、食品と製薬部門が定着しており、市場の飽和と規制の一貫性により成長率は抑えられているもの、安定した需要を提供しています。

食品、飲食品、パーソナルケア分野の需要が旺盛な欧州は、厳格な品質基準と確立された加工施設に支えられ、安定した地位を維持しています。北米は、レディ・トゥ・ドリンク飲料、コンビニエンス・フード、医薬品の急増に牽引され、着実に成長しています。この地域の消費者は、天然の保存料や風味調味料としてクエン酸を使用し、クリーンラベルの原料にますます傾倒しています。南米、特にブラジルやアルゼンチンなどの国々では、食品加工セクターの拡大と包装食品への嗜好の高まりにより、成長しつつあります。南米のメーカーは、クエン酸生産のための豊富な農産物原料という二重の利点を享受しており、輸入品への依存度も低くなっています。欧州、北米、南米では、天然添加物を優遇する規制の枠組みがクエン酸の市場可能性をさらに高めており、世界的な大手企業にも地元企業にもチャンスをもたらしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 炭酸飲料における天然酸味料への消費者シフトの高まり

- レディ・トゥ・ドリンク飲料におけるクエン酸の需要増加

- 発泡性医薬品の採用増加

- 工業用洗浄剤における生分解性キレート剤に対する規制の高まり

- 菓子類における糖質削減改質のニーズの高まり

- 生産プロセスの革新は歩留まりを改善させ、コストを削減する

- 市場抑制要因

- 新興国の原材料価格変動

- 中国製クエン酸に対するアンチダンピング関税の上昇

- 代替酸味料との競合。

- 柑橘類の入手可能性に影響を与える季節変動

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 形態別

- 無水

- 液体

- 用途別

- 飲食品

- ベーカリー

- 菓子類

- 乳製品

- 飲料

- セイボリー&スナック

- その他の飲食品

- 医薬品

- パーソナルケアと化粧品

- 洗剤と家庭用クリーナー

- その他

- 飲食品

- グレード別

- 医薬品グレード

- 食品グレード

- 工業用グレード

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- Shandong Ensign Industry Co., Ltd.

- Jungbunzlauer Suisse AG

- COFCO Corporation

- RZBC Group Co., Ltd.

- TTCA Co., Ltd.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Gadot Biochemical Industries Ltd.

- Foodchem International Corporation

- Merck KGaA

- Hawkins, Inc.

- Citrique Belge NV

- BBCA Group(Anhui BBCA)

- FUSO Chemical Co., Ltd.

- Wang Pharmaceuticals and Chemicals

- Hemadri Chemicals

- Vinipul Inorganics India Pvt. Ltd

- Arihant Chemicals

- Anmol Chemicals Private Limited

- Innova Corporate