インフラ部門- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Infrastructure Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 324 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685760

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

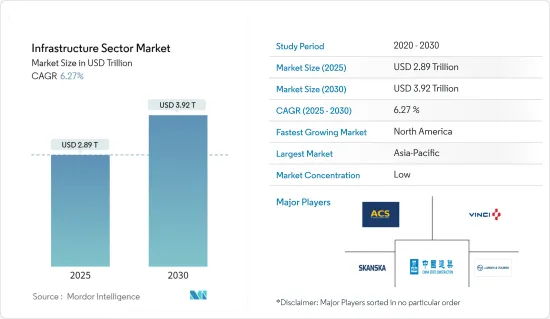

インフラ部門市場規模は2025年に2兆8,900億米ドルと推定され、予測期間中(2025年~2030年)のCAGRは6.27%で、2030年には3兆9,200億米ドルに達すると予測されます。

主なハイライト

- COVID-19は各国経済と政府、企業、個人の経済生活に悪影響を与えました。しかし、パンデミック時のインフラの利用率の大幅な低下と、それに伴う資金調達とメンテナンスの不足は、地方政府および国家政府の注目を集め、政府はパンデミック時のヘルスケアとサプライチェーンの緊急ニーズに対応するための財源配分に注力しました。COVID-19は、世界中で人員不足、サプライチェーンの混乱、政府認可の遅れによる建設の中断や遅延をもたらす需要と供給のショックを引き起こしました。多くのセクターで、利用料に依存する資産は需要の劇的な減少に直面し、その結果、プロジェクト・スポンサーは大幅な収入減に見舞われました。その結果、債務不履行、契約解除、支払不能、政府による契約違反などのプロジェクト・リスクが増大しました。

- COVID-19パンデミックによる混乱の影響を大きく受けたもの、世界各国政府が交通インフラやクリーンエネルギーへの投資を通じて経済活動の活性化を図ったため、世界のインフラ建設生産高は2020年も拡大しました。

- 結局のところ、持続可能なインフラへの世界の移行には、複数の参加者による介入と協調行動が必要です。介入には、官民協力や統合的な努力だけでなく、影響を測定する新しい方法や、グリーン・インフラ・プロジェクトに資金を供給するための革新的な手法の開発も含まれます。国や地域レベルで重要な要素には、規制の枠組み、補助金、税制などがあります。持続可能なインフラの資金調達と建設は、世界の金融・政治システムがこれまでに直面したことのない、最大かつ最も複雑な課題のひとつであることは間違いないです。しかし、この課題は克服しなければならないです。

- インフラストラクチャーは、他の資本集約型産業に比べ、先端技術への投資が相対的に不足しています。現在の環境では、容量削減とコスト上昇による圧力が、資産所有者やプロジェクト管理者に、人工知能やロボット工学などの技術の採用を加速させるかもしれないです。また、インテリジェントドローンなどの技術を利用して、メンテナンスの資本支出を削減する機会もあります。これらのドローンは現場作業員の必要性を減らし、安全性を高める。ドローンは、予防保全、検査、点検を劇的に改善することができます。ドローンは、既存の方法よりも高速に動作し、必要な修理についてのより詳細な情報を提供します。

- より広い意味では、多くの産業でリモートワークへの移行が進み、安全で弾力性のあるクラウドベースの技術や接続インフラに対するニーズが高まっています。クラウド技術の利用拡大により、インフラ投資家の間ですでに人気の高いファイバーネットワーク、データ、エッジデータセンター、通信塔などのデータ伝送・保存資産に対する需要が高まると予想されます。

インフラ市場の動向

交通インフラへの投資拡大

調査によると、2040年まで、経済成長を支えるために毎年2兆米ドル以上の交通インフラへの投資が見込まれています。利害関係者は、急速な都市化、貨物輸送サービスの需要急増、いくつかの国におけるCOVID-19対応刺激策により、インフラ開発を加速させる必要に迫られています。

開発の急速なペースと絶え間ない都市化は、輸送インフラへの支出の重要な要因です。米国運輸省連邦航空局(FAA)は2021年、空港インフラのために、全50州、プエルトリコ、米領サモアの空港における123のプロジェクトに対し、総額4億7,900万米ドルを超える資金を提供しました。

過去2~3年間、世界のパンデミックのために航空旅行は停止していました。CAAC(中国民用航空局)は、2020年末までに中国には241の認定交通空港があると発表しました。約114の空港建設プロジェクトがパンデミック中に開始または継続され、わずか8年前と比較して空港数は全体で58カ所増加しました。

アジア太平洋で急増するインフラ投資

インフラは、先進国・地域が採用したパンデミック対策と景気刺激策の主要な対象であり、世界のプロジェクト・ファイナンスを後押しすると期待されています。アジアは、プロジェクト件数と金額の伸びを示した唯一の地域でした。

アジア太平洋への直接投資流入は、パンデミック期間中も安定しており、同地域は外国投資家にとって望ましい場所として際立っていました。例えば、インド政府は、同国のGDPが近年着実に減速しているにもかかわらず、過去10年間にわたり、相当かつ安定的にFDI(外国直接投資)の流入を受けてきました。

インフラストラクチャーは、インド経済が成長し、産業部門において競争力を維持し、より良い成長に導くための重要な要素のひとつです。インフラプロジェクトの可能性は、インドのインフラ部門が直面する3大障害である官僚の遅れ、実施の遅れ、土地取得政策の実施の遅れを凌駕します。

インフラプロジェクトを加速させるため、現政権はこれらの遅延を最小限に抑え、プロセスを簡素化し、透明性を促進することを公約に掲げています。2019~25年度のNIP(国家インフラ・パイプライン)の一部として、総額111,000インドルピー(1兆5,000億米ドル)にのぼる多数のインフラ・プロジェクトが政府から発表されました。

政府は当初、この金額を6,835のプロジェクトに割り当てたが、2021年末までにその数は7,400に増加しました。プロジェクトの価値の大半は、道路、住宅、都市開発、鉄道、再生可能エネルギー、従来型電力、灌漑で構成されています。

フィリピン政府は、2021年の大幅な景気回復の起爆剤としてインフラ開発を推し進めました。公共事業・高速道路開発省は、2021年国家予算の一部として、橋梁建設、洪水管理、資産保全、交通網整備に65億米ドルを受け取り、インフラ・プロジェクトに重点を置いた。

鉄道輸送、陸上公共交通、海上インフラへの投資として、運輸省は13億米ドルを受け取りました。

インフラ業界の概要

世界のインフラ市場は、あらゆる国や地域に国内外の企業が混在し、非常に細分化された競争市場となっています。

世界の主要企業には、ACS Actividades de Construccion y Servicios SA(ACSグループ)、VINCI、China State Construction Engineering Corp.Ltd.、Skanska AB、Larsen &Toubro、鹿島建設、Hochtief Aktiengesellschaft、China Communications Construction Group Ltd、Balfour Beatty、Bouygues Group、Fluor Corporation、Hyundai Engineering &Construction(HDEC)などです。

この業界の一部とされる建設部門には多くの種類があります。開発、エンジニアリング、特殊建設、計画・開発などは、この活況を呈する業界を構成するいくつかの部門です。世界の建設業界が生み出す収益は、近年大幅に増加しています。欧州と中国の建設請負業者が、世界の建設請負収入の最大シェアを占めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 業界の展望(現在の経済と建設市場のシナリオ)

- GDP、財政政策、金融政策、経済活動

- インフレ率

- 金利

- 為替レート

- 消費者信頼感

- インフラ支出

- 開発指標ランキング

- 世界のインフラ部門の規制環境、コンプライアンス・プロセス、EHS動向、主要政策イニシアティブ

- 建設セクターにおける技術革新

- 市場力学

- 促進要因

- 抑制要因

- 機会

- ポーターのファイブフォース分析

- 業界バリューチェーン分析

- COVID-19の市場への影響

第5章 市場セグメンテーション

- タイプ別

- 社会インフラ

- 学校

- 病院

- 防衛

- その他インフラ

- 交通インフラ

- 鉄道

- 道路

- 空港

- 港湾

- 水路

- 採掘インフラ

- 石油・ガス

- その他の採掘(鉱物、金属、石炭)

- 公益事業インフラ

- 発電

- 送電・配電

- 水

- ガス

- 電気通信

- 製造インフラ

- 金属・鉱石生産

- 石油精製

- 化学製造

- 工業団地とクラスター

- その他のインフラ

- 社会インフラ

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 世界のインフラ部門-投資分析

- 直接投資を含む(公共、民間、PPP)

- 間接投資(INVITs、IOCs、その他)

- EPC、BOT、その他-インフラプロジェクトの資金調達モデルと市場動向

第7章 競合情勢

- 競合概要(概要と市場シェア分析)

- 企業プロファイル

- ACS Actividades de Construccion y Servicios S.A.(ACS Group)

- VINCI SA

- China State Construction Engineering Corporation Ltd

- Skanska AB

- Larsen & Toubro

- Kajima Corporation

- Hochtief Aktiengesellschaft

- China Communications Construction Group Ltd

- Balfour Beatty

- Bouygues Group

- Fluor Corporation

- Hyundai Engineering & Construction Co. Ltd(HDEC)*

第8章 市場の将来展望

目次

The Infrastructure Sector Market size is estimated at USD 2.89 trillion in 2025, and is expected to reach USD 3.92 trillion by 2030, at a CAGR of 6.27% during the forecast period (2025-2030).

Key Highlights

- COVID-19 had a negative impact on national economies and the economic livelihood of governments, businesses, and individuals. But significantly lower usage rates in infrastructure during the pandemic and the resulting shortfall in financing and maintenance received the attention of local and national governments, which focused on allocating financial resources to meet the immediate needs of healthcare and supply chains during the pandemic. COVID-19 caused a demand and supply shock that resulted in construction interruptions or delays due to a lack of personnel, supply chain disruptions, or delays in government approvals throughout the world. In many sectors, assets dependent on user fees faced a dramatic decrease in demand, resulting in substantial revenue losses for project sponsors. This increased project risks, such as default events, termination, insolvency, or governments breaching contracts.

- Although heavily impacted by the disruptions caused by the COVID-19 pandemic, the global infrastructure construction output still expanded in 2020, as governments around the world sought to stimulate economic activity through investments in transport infrastructure and clean energy.

- Ultimately, the global shift to sustainable infrastructure requires interventions and collaborative action from multiple participants. The interventions include not just public-private cooperation and consolidated effort but also new ways of measuring the impact and developing innovative instruments geared to financing green infrastructure projects. Factors important at a national and regional level include regulatory frameworks, subsidies, and tax regimes. These overlapping considerations mean that funding and building sustainable infrastructure is arguably one of the biggest and most complex challenges the global financial and political system has ever faced. But it is a challenge that must be overcome.

- Infrastructure is relatively underinvested in advanced technologies compared to other capital-intensive industries. In the current environment, pressure due to capacity reduction and the rising costs may encourage asset owners and project managers to accelerate the adoption of technologies such as artificial intelligence and robotics. There is also an opportunity to reduce maintenance capital expenses using technologies such as intelligent drones. These drones lessen the need for onsite workers, thus increasing safety. They can dramatically improve preventative maintenance, inspecting, and scoping. They work faster than existing methods and provide more detailed information about required repairs.

- More broadly, the shift to remote working arrangements across many industries has underlined the growing need for secure, resilient, cloud-based technologies, and connective infrastructure. Growing usage of cloud technology is expected to boost the demand for data transmission and storage assets including fiber networks, data, edge datacentres, and telecommunication towers that are already popular among infrastructure investors.

Infrastructure Construction Market Trends

Growing Investment in Transport Infrastructure

According to the research, until 2040, more than USD 2 trillion worth of investments in transport infrastructure is expected annually to support economic growth. Stakeholders are under pressure to accelerate infrastructure development due to rapid urbanization, soaring freight service demand, and the COVID-19 response stimulus programs in several nations.

The rapid pace of development and continuous urbanization is a key factor in the expenditure on transport infrastructure. The Federal Aviation Administration (FAA) of the US Department of Transportation gave funds totaling more than USD 479 million for airport infrastructure in 2021 to 123 projects at airports in all 50 states, Puerto Rico, and American Samoa.

For the past two-three years, aviation travel was halted due to the global pandemic. The CAAC (Civil Aviation Administration of China) said that by the end of 2020, China had 241 accredited transport airports. About 114 airport construction projects were either started or continued during the pandemic, and there were 58 more airports overall compared to that just eight years earlier.

SURGING INFRASTRUCTURE INVESTMENT IN ASIA-PACIFIC

Infrastructure is a major target of the pandemic response and stimulus measures adopted by advanced countries and regions, which are expected to boost global project finance. Asia was the only region to demonstrate growth in project numbers and values.

FDI inflows to the Asia-Pacific region were steady during the pandemic; the region stood out as a desirable location for foreign investors. For instance, the Government of India received considerable and consistent inflows of FDI (foreign direct investment) over the past ten years, despite the country's GDP decelerating steadily in recent years.

Infrastructure is one of the key elements that help the Indian economy grow and remain competitive in the industrial sector, leading to better growth. The possibility of infrastructure projects overrides bureaucratic delays, implementation delays, and delays in the implementation of land acquisition policies, the three major obstacles facing India's infrastructure sector.

To speed up infrastructure projects, the present administration has pledged to minimize these delays, simplify the process, and promote transparency. A number of infrastructure projects totaling INR 111 lakh crore (USD 1.5 trillion) were announced by the government as part of the NIP (National Infrastructure Pipeline) for FY 2019-25.

The government initially allocated the amount for 6,835 projects, but by the end of 2021, that number had increased to 7,400. Majority of the project's worth comprises roads, housing, urban development, railroads, renewable energy, conventional power, and irrigation.

The Philippines' government pushed for infrastructure development to spark a significant economic recovery in 2021. The Department of Public Works and Highways received USD 6.5 billion for bridge construction, flood management, asset preservation, and transportation network development as part of the 2021 national budget, which placed a heavy emphasis on infrastructure projects.

For investments in rail transportation, land public transportation, and maritime infrastructure, the Department of Transportation received USD 1.3 billion.

Infrastructure Construction Industry Overview

The global infrastructure construction market is highly fragmented and competitive, with a mix of domestic and international players existing in all countries and regions.

Some of the top players worldwide include ACS Actividades de Construccion y Servicios SA (ACS Group), VINCI, China State Construction Engineering Corp. Ltd, Skanska AB, Larsen & Toubro, Kajima Corporation, Hochtief Aktiengesellschaft, China Communications Construction Group Ltd, Balfour Beatty, Bouygues Group, Fluor Corporation, and Hyundai Engineering & Construction Co. Ltd (HDEC).

There are many types of construction sectors that are considered part of the industry. Building, engineering, specialty construction, and planning and development are a few sectors that comprise this booming industry. The revenue generated by the global construction industry significantly increased in recent years. European and Chinese construction contractors generated the largest share of construction contract revenues worldwide.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Industry Outlook (Current Economic and Construction Market Scenario)

- 4.1.1 GDP, Fiscal Policy, Monetary Policy, Economic Activity

- 4.1.2 Inflation

- 4.1.3 Interest Rates

- 4.1.4 Exchange Rates

- 4.1.5 Consumer Confidence

- 4.1.6 Infrastructure Spending

- 4.1.7 Development Indices Ranking

- 4.2 Regulatory Environment, Compliance Processes, EHS Trends and Key Policy Initiatives for the Global Infrastructure Sector

- 4.3 Technological Innovations in the Construction Sector

- 4.4 Market Dynamics

- 4.4.1 Drivers

- 4.4.2 Restraints

- 4.4.3 Opportunities

- 4.4.4 Porter's Five Forces Analysis

- 4.4.5 Industry Value Chain Analysis

- 4.5 Impact of COVID - 19 on the Market

5 MARKET SEGMENTATION (Market Size By Value)

- 5.1 By Type

- 5.1.1 Social Infrastructure

- 5.1.1.1 Schools

- 5.1.1.2 Hospitals

- 5.1.1.3 Defense

- 5.1.1.4 Other Infrastructure

- 5.1.2 Transportation Infrastructure

- 5.1.2.1 Railways

- 5.1.2.2 Roadways

- 5.1.2.3 Airports

- 5.1.2.4 Ports

- 5.1.2.5 Waterways

- 5.1.3 Extraction Infrastructure

- 5.1.3.1 Oil and Gas

- 5.1.3.2 Other Extraction (Minerals, Metals, and Coal)

- 5.1.4 Utilities Infrastructure

- 5.1.4.1 Power Generation

- 5.1.4.2 Electricity Transmission & Distribution

- 5.1.4.3 Water

- 5.1.4.4 Gas

- 5.1.4.5 Telecoms

- 5.1.5 Manufacturing Infrastructure

- 5.1.5.1 Metal and Ore Production

- 5.1.5.2 Petroleum Refining

- 5.1.5.3 Chemical Manufacturing

- 5.1.5.4 Industrial Parks and Clusters

- 5.1.5.5 Other Infrastructure

- 5.1.1 Social Infrastructure

- 5.2 By Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Latin America

- 5.2.5 Middle East & Africa

6 GLOBAL INFRASTRUCTURE SECTOR- INVESTMENT ANALYSIS

- 6.1 Includes Direct Investment -Public, Private and PPP

- 6.2 Indirect Investment (INVITs, IOCs, Others)

- 6.3 EPC, BOT, Others-Infrastructure Project Financing Models and Market Trends

7 COMPETITIVE LANDSCAPE

- 7.1 Competition Overview (Overview and Market Share Analysis)

- 7.2 Company Profiles

- 7.2.1 ACS Actividades de Construccion y Servicios S.A. (ACS Group)

- 7.2.2 VINCI SA

- 7.2.3 China State Construction Engineering Corporation Ltd

- 7.2.4 Skanska AB

- 7.2.5 Larsen & Toubro

- 7.2.6 Kajima Corporation

- 7.2.7 Hochtief Aktiengesellschaft

- 7.2.8 China Communications Construction Group Ltd

- 7.2.9 Balfour Beatty

- 7.2.10 Bouygues Group

- 7.2.11 Fluor Corporation

- 7.2.12 Hyundai Engineering & Construction Co. Ltd (HDEC)*

8 FUTURE OUTLOOK OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 324 Pages

- 納期

- 2~3営業日