|

市場調査レポート

商品コード

1911819

インド防水ソリューション市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年)India Waterproofing Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インド防水ソリューション市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

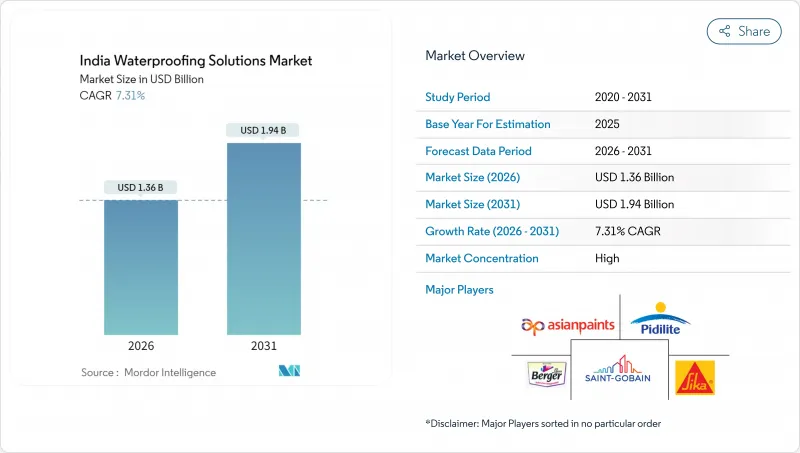

インド防水ソリューション市場は、2025年の12億7,000万米ドルから2026年には13億6,000万米ドルへ成長し、2026年から2031年にかけてCAGR7.31%で推移し、2031年までに19億4,000万米ドルに達すると予測されています。

国家インフラ整備計画に基づく堅調な公共支出、気候変動への耐性を重視した建築基準の厳格化、予防保全への明確な顧客志向の転換により、原材料コストの変動にもかかわらず、インド防水ソリューション市場は安定した成長軌道を維持しております。防水シートは、厳しいモンスーン条件下での実績ある性能と、開発業者や富裕層の住宅所有者が求める長期保証を兼ね備えていることから、依然として主要技術として支持されております。住宅建設がプレミアム化を牽引する一方、商業・産業・インフラプロジェクトは、熱反射ハイブリッド防水シートなどの先進システムに規模をもたらします。多角化を進める塗料大手や専門化学品サプライヤーが、研究開発の強化、施工業者ネットワークの拡充、インド規格局(BIS)の改訂防水仕様への対応を競う中、競合は激化しています。

インド防水ソリューション市場の動向と洞察

急速な都市化と手頃な価格の住宅政策

インドでは年間1,000万人以上の都市住民が増加しており、プラダン・マントリ・アワス・ヨジャナ(PMAY)計画だけでも2025年までに2,000万戸の新規低価格住宅供給を目標としています。改修工事は新規施工の最大5倍の費用がかかるため、開発業者は設計段階で予防的防水を指定するケースが増加しています。2024-25年度予算では気候変動に強いインフラに1,440億米ドルを計上しており、この措置によりBIS準拠防水材への資金供給が直接結びついています。100の自治体で推進されるスマートシティ計画により、地下鉄駅、立体駐車場、複合用途タワーなど地下構造物向けの防水シート需要が高まっています。密集した都心部での垂直建設では、複雑な形状にも継ぎ目なく対応し、不同沈下による損傷リスクの少ないコールド液状防水シートが好まれています。

熱反射性を備えたハイブリッド液体防水シートの採用

防水性と近赤外線反射性を兼ね備えたハイブリッド液体防水シートは、夏のピーク時に屋上温度を最大15℃低下させます。これにより空調エネルギー負荷が軽減され、IGBC(インドグリーンビルディング評議会)やLEED(米国環境設計協会)の認証ポイント取得に貢献します。アジアペインツ社とシーカAG社は、インドの紫外線が強い気候における耐久性と耐変色性の懸念に対応するため、ポリマーの研究開発を拡大しています。早期導入事例としては、広大な屋根面積で省エネルギー効果が急速に累積するデータセンターや製造工場が挙げられます。この技術は住宅高層プロジェクトにも浸透し始めており、熱取得量の低減は中高級層購入者をターゲットとする開発業者にとってマーケティング上の付加価値となります。長期的な普及拡大には、現地原料調達と生産量拡大による製品コスト削減が鍵となります。

施工業者の分散化が施工不良を招く

全国的に防水システムの約80%は、正式な訓練が限られた小規模業者が施工しており、施工品質のばらつきや早期故障を招いています。都市部の開発業者はOEM認定施工業者の採用を義務付ける傾向が強まっていますが、インドの広大な建設市場への浸透は依然として課題です。メーカーは地域研修センターへの資金提供を行っていますが、労働者が短期プロジェクト間を移動するため、熟練労働者の定着率は低くなっています。短期的には、施工不良がエンドユーザーの信頼を損ない、精密な施工を必要とする高級防水シートへの移行を遅らせています。

セグメント分析

防水シートは2025年時点でインド防水ソリューション市場の65.62%を占め、2031年までCAGR7.46%を維持し、要求の厳しい用途における機能基準としての地位を強化します。常温液体塗布型防水シートは、複雑な屋根形状に継ぎ目のないバリアを形成し、トーチを必要とせずに硬化するため、住宅建設業者に支持されています。これにより現場の安全性が向上します。全面接着シートシステムは、実績ある20年間の現場性能が重視される大規模商業施設屋根やポディウムスラブで主流です。高温液体塗布型は化学プラントや製油所向けであり、敷設式シートはプレハブ施工を可能にすることで、迅速なインフラプロジェクトを支援します。

高度なエラストマー化学技術により、防水シートは最大2mmのひび割れを橋渡し可能であり、変位が生じる高層構造物において決定的な優位性を発揮します。プレミアム住宅セグメントでは保証期間が12年に延長され、デジタル検査ツールによりメーカーは保証適用前に施工監査を実施できます。局所的な補修や特殊基材向けには化学製品が依然重要ですが、防水シートの市場規模は規模拡大に伴う平方メートル単価の低下により拡大を続けております。主要サプライヤーによる戦略的な原材料のバックワード・インテグレーションは、原油価格変動による影響から防水シートの価格をさらに保護します。

インド防水ソリューション報告書は、サブ製品別(化学薬品と防水シート)および最終用途分野別(商業・産業・公共施設、インフラ、住宅)に分類されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 急速な都市化と手頃な価格の住宅政策の推進

- 熱反射性を付加したハイブリッド液体膜の採用

- 強まるモンスーンによる気候変動対応型建築基準の必要性

- 住宅所有者のプレミアム志向と10年保証の需要

- 低VOCナノ浸透技術への移行

- 市場抑制要因

- 施工業者の基盤が分散しているため、施工不良が発生しています

- 原油連動の原材料価格変動がポリウレタン(PU)及びアスファルトに影響

- 予防的防水に対する地方都市部・農村部の認知度が限定的

- バリューチェーン分析

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- サブ製品別

- 化学品

- エポキシ系

- ポリウレタン系

- 水性

- その他の技術

- 防水シート

- コールド液状塗布

- 完全接着シート

- ホット液状塗布

- ルーズレイドシート

- 化学品

- 最終用途分野別

- 商業用

- 産業・公共施設

- インフラ

- 住宅用

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Ardex Group

- Asian Paints

- Berger Paints India Limited

- Bostik(Arkema)

- Choksey FixGuruu

- CICO Group

- Kryton International Inc.

- MAPEI S.p.A.

- MC-Bauchemie

- Pidilite Industries Ltd.

- Saint-Gobain

- Sika AG

- Soprema Group

- STP Limited, India

- Ultratech Cement Ltd.

- Xypex Chemical Corporation