自動車用MLCC:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Automotive MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 322 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684041

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

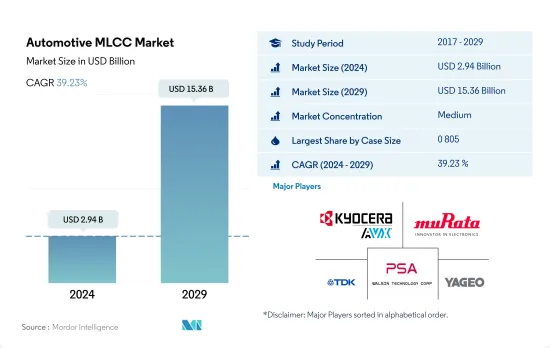

自動車用MLCC市場規模は2024年に29億4,000万米ドルと推定・予測され、2029年には153億6,000万米ドルに達し、予測期間(2024年~2029年)のCAGRは39.23%で成長すると予測されています。

自動車の進化におけるMLCCの多面的役割の解明がMLCC需要を牽引

- 進化を続ける自動車業界の情勢において、MLCCの役割は単なる電子部品の域を超えています。これらの小型パワーハウスは、配電やノイズ抑制からシグナル・コンディショニングや電圧レギュレーションに至るまで、さまざまな機能の交響曲を奏でる、現代の自動車システムの要となっています。

- 0 603 MLCCは、コンパクトでありながら、なくてはならない存在です。これらのコンデンサは、小型でエネルギー効率の高い設計にシフトする上で極めて重要な役割を果たします。自動車技術の進歩に伴い、合理化されたソリューションへの需要が0 603セグメントの存在感を高めています。

- 0 805コンデンサは、特に電気自動車(EV)が主流になるにつれて、市場で重要な位置を占めています。EVの急速な普及は、効果的な配電と制御の必要性を強調し、0 805セグメントの重要性を強調しています。EVが自動車の展望を再定義する中、これらのコンデンサは性能と効率の実現者として機能します。

- 1 206コンデンサは、サイズと汎用性のバランスが取れており、多様な自動車用途に適した選択肢となっています。自動車産業が技術の進歩を受け入れるにつれ、1 210セグメントの重要性が明らかになります。

- その他」セグメントは、特殊な自動車要件に対応する様々な静電容量値を包含しています。新しい技術からユニークなアプリケーションまで、この多様なセグメントは、自動車の明確なニーズを満たすMLCCの適応性を例証しています。

アジア太平洋、欧州、北米におけるMLCCの影響力を明らかにする

- アジア太平洋、欧州、北米は自動車産業における変革の原動力となっています。技術の進歩、持続可能性、スマートモビリティソリューションの追求は、自動車の進化を支える積層セラミックコンデンサ(MLCC)の重要な役割を浮き彫りにしています。各地域が革新と効率の未来に向かって推進する中、高品質MLCCへの需要は拡大し続けており、自動車のバリューチェーンにおけるMLCCの重要性は確固たるものとなっています。

- アジア太平洋は、急速な技術進歩と消費者需要の拡大を特徴とする自動車技術革新の震源地です。中国、日本、韓国といった主要な自動車拠点があるこの地域は、電気自動車(EV)の導入、コネクテッドカー、自律走行において最先端を走っています。

- 欧州の自動車産業は、技術革新、持続可能性、厳格な環境規制の代名詞です。この地域は、二酸化炭素排出量の削減と、よりクリーンなモビリティ・ソリューションへの移行に取り組んでおり、自動車の展望を再構築しています。電気自動車やハイブリッド車の普及に伴い、電源管理、ノイズ抑制、電圧調整用MLCCの需要が高まっています。

- 北米の自動車セクターは、スマートモビリティソリューションと先進技術の追求を特徴としています。北米の消費者がより充実した運転体験と最先端機能を求める中、EV、インフォテインメント・システム、ADASなどのアプリケーションにおけるMLCCの需要は増加傾向にあります。この地域のダイナミックな自動車事情は、MLCC市場拡大の主要な促進要因となっています。

世界の自動車用MLCC市場動向

水素ステーションのインフラ整備が販売拡大を継続

- 燃料電池電気自動車(FCEV)は、燃料として貯蔵した水素エネルギーを燃料電池で電気に変換し、電気自動車と同様の推進メカニズムを持っています。従来の内燃機関を動力源とする自動車と比較して、FCEVは有害な排気ガスを排出しないです。

- 燃料電池電気自動車の出荷台数は、2022年には4万3,000台であり、2029年には7万1,000台に達すると予想されます。風力や太陽光のような再生可能エネルギーが水素製造プロセスにますます貢献するようになると、エネルギー効率の高いFCEVの需要が大幅に増加します。

- 低排出ガス車への需要が高まるにつれ、より厳しい二酸化炭素排出規制が実施され、迅速な燃料補給のような利点からFCEVの採用がより重視されています。FCEVの開発を促進するため、複数の政府機関や商業団体が協力し、燃料電池技術の進歩や水素補給インフラの開発に投資しています。IEAによると、2021年末には世界で約730箇所の水素ステーション(HRS)があり、約51,600台のFCEVに燃料を供給しています。これは、2020年からFCEVの世界ストックがほぼ50%増加し、HRSの数が35%増加することを意味します。これらの要因は、FCEVの今後の高成長に寄与しています。

厳しい政府規制が電気自動車の普及を促進

- MLCCは、高温耐性と容易な表面実装フォームファクターを提供し、EVエレクトロニクスとサブシステムに最適な部品として登場しました。電気自動車には約8,000~1万個のMLCCが使用されています。電気自動車のMLCCは、バッテリー管理システム(BMS)、車載充電器(OBC)、DC/DCコンバーターで一般的に使用されています。これらのEVサブシステムに要求される一般仕様を満たし、EV内の過酷な環境でも確実に機能する能力を持つことに加え、部品メーカーはIATF16949認定を受け、AEC-Q200に準拠している必要があります。

- 電気自動車の出荷台数は、2022年に1,640万台を占め、2029年には2,552万台まで増加すると予想されています。温室効果ガスの排出を削減し、気候変動と闘うために、いくつかの国が厳しい環境規制を実施しています。その結果、自動車メーカーはより多くの電気自動車を生産し、化石燃料への依存を減らすよう、ますます強く求められています。消費者の環境意識も高まり、従来のガソリン車に代わる持続可能な自動車を求めるようになっています。

- COVID-19パンデミックとロシアのウクライナ戦争は世界のサプライチェーンを混乱させ、自動車産業は大きな影響を受けました。しかし、長期的に見れば、EV市場は世界の一部の地域で売上を伸ばしています。これは、公的に利用可能な充電インフラの配備を支援する政府や企業の取り組みが、EVの売上をさらに伸ばすための強固な基盤となっているためです。世界で公的に利用可能な充電器は180万基に近づき、2021年には約50万基が設置され、そのうち3分の1が急速充電器であり、2017年に設置された公営充電器の総数を上回りました。

自動車用MLCC産業の概要

自動車用MLCC市場は適度に統合されており、上位5社で60.58%を占めています。この市場の主要企業は以下の通りです。 Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, TDK Corporation, Walsin Technology Corporation and Yageo Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車販売台数

- 世界のBEV(バッテリー電気自動車)生産台数

- 世界の電気自動車販売台数

- FCEV(燃料電池電気自動車)の世界生産台数

- 世界のHEV(ハイブリッド電気自動車)生産台数

- 世界の大型商用車販売台数

- 世界のICEV(内燃エンジン車)生産台数

- 小型商用車の世界販売台数

- 非電気自動車の世界販売台数

- PHEV(プラグインハイブリッド車)の世界生産台数

- 乗用車の世界販売台数

- 世界の二輪車販売台数

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 大型商用車

- 小型商用車

- 乗用車

- 二輪車

- 燃料タイプ

- 電気自動車

- 非電気自動車

- 推進タイプ

- BEV-バッテリー電気自動車

- FCEV-燃料電池電気自動車

- HEV-ハイブリッド電気自動車

- ICEV-内燃機関自動車

- PHEV-プラグインハイブリッド電気自動車

- その他

- コンポーネントタイプ

- ADAS

- インフォテインメント

- パワートレイン

- 安全システム

- その他

- ケースサイズ

- 0 603

- 0 805

- 1 206

- 1 210

- 1 812

- その他

- 電圧

- 50V~200V

- 50V未満

- 200V以上

- 静電容量

- 10μF~1,000μF

- 10μF未満

- 1,000μF以上

- 誘電体タイプ

- クラス1

- クラス2

- 地域

- アジア太平洋

- 欧州

- 北米

- 世界のその他の地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Automotive MLCC Market size is estimated at 2.94 billion USD in 2024, and is expected to reach 15.36 billion USD by 2029, growing at a CAGR of 39.23% during the forecast period (2024-2029).

Unveiling the multifaceted role of MLCCs in the automotive evolution is driving MLCC demand

- In the ever-evolving landscape of the automotive industry, the role of MLCCs has moved beyond mere electronic components. These miniature powerhouses are the cornerstone of modern vehicular systems, orchestrating a symphony of functions ranging from power distribution and noise suppression to signal conditioning and voltage regulation.

- The 0 603 MLCCs are compact yet indispensable contributors. These capacitors play a pivotal role in shifting toward compact and energy-efficient designs. With advancements in automotive technologies, the demand for streamlined solutions has elevated the prominence of the 0 603 segment.

- The 0 805 capacitors occupy a significant position in the market, particularly as electric vehicles (EVs) become mainstream. The surge in EV adoption emphasizes the need for effective power distribution and control, underscoring the relevance of the 0 805 segment. As EVs redefine the automotive landscape, these capacitors act as enablers of performance and efficiency.

- The 1 206 capacitors represent a balance between size and versatility, making them a preferred choice for diverse automotive applications. As the automotive industry embraces technological advancements, the importance of the 1 210 segment becomes evident.

- The 'others' segment encompasses an array of capacitance values that cater to specialized automotive requirements. From emerging technologies to unique applications, this diverse segment exemplifies the adaptable nature of MLCCs in meeting distinct automotive needs.

Unveiling the impact of MLCCs in Asia-Pacific, Europe, and North America

- Asia-Pacific, Europe, and North America are driving transformative changes in the automotive industry. Their pursuit of technological advancements, sustainability, and smart mobility solutions underscores the crucial role of multi-layer ceramic capacitors (MLCCs) in supporting the evolution of vehicles. As each region propels toward a future of innovation and efficiency, the demand for high-quality MLCCs continues to grow, cementing their significance in the automotive value chain.

- Asia-Pacific stands as an epicenter of automotive innovation characterized by rapid technological advancements and growing consumer demand. With major automotive hubs like China, Japan, and South Korea, this region is at the forefront of electric vehicle (EV) adoption, connected cars, and autonomous driving.

- Europe's automotive industry is synonymous with innovation, sustainability, and stringent environmental regulations. The region's commitment to reducing carbon emissions and transitioning toward cleaner mobility solutions is reshaping the automotive landscape. As electric and hybrid vehicles gain traction, the demand for MLCCs for power management, noise suppression, and voltage regulation is escalating.

- North America's automotive sector is characterized by its pursuit of smart mobility solutions and advanced technologies. As North American consumers seek enhanced driving experiences and cutting-edge features, the demand for MLCCs in applications like EVs, infotainment systems, and ADAS is on the rise. The region's dynamic automotive landscape positions it as a key driver of the MLCC market's expansion.

Global Automotive MLCC Market Trends

Infrastructure improvement for hydrogen stations continues to increase sales

- Fuel cell electric vehicles (FCEVs) use hydrogen energy stored as fuel, which is then converted into electricity by the fuel cell and has a propulsion mechanism similar to that of an electric vehicle. Compared to vehicles powered by conventional internal combustion engines, FCEVs do not emit any harmful exhaust emissions.

- Fuel cell electric vehicle shipments accounted for 0.043 million units in 2022, and these are expected to reach 0.071 million units in 2029. As renewable energies like wind and solar contribute increasingly to the hydrogen manufacturing process, there will be a huge increase in the demand for energy-efficient FCEVs.

- As the demand for low-emission vehicles rises, stricter carbon emission standards are being implemented, and more emphasis is being placed on the adoption of FCEVs due to benefits like quick refueling. To encourage the development of FCEVs, several government and commercial organizations are collaborating and investing in advancing fuel cell technology and the development of hydrogen refueling infrastructure. According to the IEA, at the end of 2021, there were about 730 hydrogen refueling stations (HRSs) globally providing fuel for about 51,600 FCEVs. This represents an increase of almost 50% in the global stock of FCEVs and a 35% increase in the number of HRSs from 2020. These factors contribute to the high growth of FCEVs in the future.

Stringent government regulations are increasing the penetration of electric vehicles

- MLCCs have emerged as a perfect component for EV electronics and subsystems, offering high-temperature resistance and an easy surface-mount form factor. Approximately 8,000-10,000 MLCCs are used in an electric vehicle. MLCCs in electric vehicles are commonly used in battery management systems (BMS), onboard chargers (OBC), and DC/DC converters. In addition to meeting the general specifications required for these EV subsystems and having the ability to function reliably in harsh environments inside an EV, component manufacturers should also be IATF 16949-certified and compliant with AEC-Q200.

- Electric vehicle shipments accounted for 16.4 million units in 2022, and it is expected to rise to 25.52 million units in 2029. Several countries have implemented strict environmental regulations to reduce greenhouse gas emissions and combat climate change. As a result, automakers are under increasing pressure to produce more electric vehicles and reduce their reliance on fossil fuels. Consumers are becoming more environmentally conscious and are looking for more sustainable alternatives to traditional gasoline-powered vehicles.

- The COVID-19 pandemic and Russia's war in Ukraine disrupted global supply chains, and the automotive industry has been heavily impacted. However, in the longer term, the EV market is witnessing sales growth in some regions of the world as government and corporate efforts to support the deployment of publicly available charging infrastructure are providing a solid basis for further increase in EV sales. Publicly accessible chargers worldwide approached 1.8 million, with nearly 500,000 chargers installed in 2021, of which a third were fast chargers, which accounted for more than the total number of public chargers installed in 2017.

Automotive MLCC Industry Overview

The Automotive MLCC Market is moderately consolidated, with the top five companies occupying 60.58%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, TDK Corporation, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Sales

- 4.1.1 Global BEV (Battery Electric Vehicle) Production

- 4.1.2 Global Electric Vehicles Sales

- 4.1.3 Global FCEV (Fuel Cell Electric Vehicle) Production

- 4.1.4 Global HEV (Hybrid Electric Vehicle) Production

- 4.1.5 Global Heavy Commercial Vehicles Sales

- 4.1.6 Global ICEV (Internal Combustion Engine Vehicle) Production

- 4.1.7 Global Light Commercial Vehicles Sales

- 4.1.8 Global Non-Electric Vehicle Sales

- 4.1.9 Global PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.1.10 Global Passenger Vehicles Sales

- 4.1.11 Global Two-Wheeler Sales

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Heavy Commercial Vehicle

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Passenger Vehicle

- 5.1.4 Two-Wheeler

- 5.2 Fuel Type

- 5.2.1 Electric Vehicle

- 5.2.2 Non-Electric Vehicle

- 5.3 Propulsion Type

- 5.3.1 BEV - Battery Electric Vehicle

- 5.3.2 FCEV - Fuel Cell Electric Vehicle

- 5.3.3 HEV - Hybrid Electric Vehicle

- 5.3.4 ICEV - Internal Combustion Engine Vehicle

- 5.3.5 PHEV - Plug-in Hybrid Electric Vehicle

- 5.3.6 Others

- 5.4 Component Type

- 5.4.1 ADAS

- 5.4.2 Infotainment

- 5.4.3 Powertrain

- 5.4.4 Safety System

- 5.4.5 Others

- 5.5 Case Size

- 5.5.1 0 603

- 5.5.2 0 805

- 5.5.3 1 206

- 5.5.4 1 210

- 5.5.5 1 812

- 5.5.6 Others

- 5.6 Voltage

- 5.6.1 50V to 200V

- 5.6.2 Less than 50V

- 5.6.3 More than 200V

- 5.7 Capacitance

- 5.7.1 10 µF to 1000 µF

- 5.7.2 Less than 10 µF

- 5.7.3 More than 1000µF

- 5.8 Dielectric Type

- 5.8.1 Class 1

- 5.8.2 Class 2

- 5.9 Region

- 5.9.1 Asia-Pacific

- 5.9.2 Europe

- 5.9.3 North America

- 5.9.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 322 Pages

- 納期

- 2~3営業日