北米の無糖チューインガム市場:シェア分析、産業動向、成長予測(2025年~2030年)

North America Sugar-free Chewing Gum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 147 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684026

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

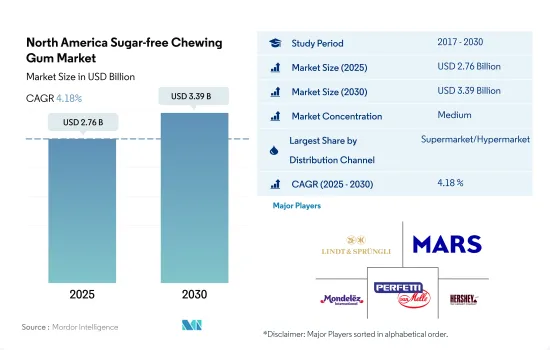

北米の無糖チューインガム市場規模は2025年に27億6,000万米ドルと推計され、2030年には33億9,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは4.18%で成長します。

スーパーマーケット/ハイパーマーケットおよびその他セグメントによる機能性製品への需要の増加が、2023年に70%の金額シェアを有することにより、無糖チューインガムの流通を牽引しています。

- 北米の全体的な流通チャネルは、無糖ガム市場の成長に重要な役割を果たしています。流通セグメントでは、小売業者は消費者の関心を引きつけるために多種多様な無糖チューインガム製品を提供しています。さらに、これらの小売業者は、無糖ガムを多種多様なフレーバー、テクスチャー、パッケージにセグメント化しています。2023年、流通チャネルは2022年と比較して1.34%のシェアを占めています。

- 金額ベースでは、スーパーマーケットとハイパーマーケットが北米の主要小売業者と考えられています。これらの小売業者は、様々な価格帯(低価格、中価格、高価格)でチューインガムを販売しています。2023年の無糖の平均販売価格は2.12米ドルでした。それぞれの動向により、この地域の消費者の購買力を促進するため、消費者は主にこれらの小売ユニットに傾いています。

- コンビニエンスストアは北米で2番目に大きな小売業者と考えられています。これは、コンビニエンスストアが消費者により大きな利便性を提供できるからです。2023年には、ベッカーズはオンタリオ州に45店舗を所有していることが確認されています。

- 北米全土でインターネット・ユーザーの普及が進むにつれ、オンライン食料品店への需要は、同地域の小売業にとって極めて重要な要素となっています。2022年末までに、メキシコのインターネットユーザー総数は8,950万人で、総人口の75.7%を占めました。

- 予測期間中(2026年~2029年)、同市場は2.21%の成長が見込まれます。無糖食品業界を牽引する主な要因は、アメリカ国民の健康増進に対する需要の高まりと関連しています。また、無糖ガムの小売業者がユニークなフレーバーのガムを発売することも予想されます。

米国では消費者の10人中8人が砂糖の削減に取り組んでおり、同国は2023年に北米で無糖チューインガムの最も高い需要を経験しました。

- 北米の無糖チューインガム市場は、2023年には2022年比で3.4%の成長を記録しました。口腔の健康や砂糖が歯の健康に与える影響に対する意識の高まりが、無糖ガムの需要拡大につながりました。無糖ガムは、虫歯や虫歯のリスクを最小限に抑えながらチューインガムを楽しむ方法を提供します。

- 国別では、米国がこの地域の無糖ガム市場をリードしており、2023年と比較して2027年には16.1%の成長が見込まれています。チューインガム市場は、糖尿病や砂糖関連疾患の発生による無糖食品・飲食品への国民の傾斜により、「無糖」前線の開発へとパラダイムシフトしつつあります。2021年末時点で、米国の消費者10人中8人が砂糖削減に取り組んでいます。

- メキシコは同地域で無糖チューインガムの第2位の市場です。同国は2021年から2023年にかけて14.3%の成長率を記録しました。無糖ガムの人気のため、無糖ガムの種類には継続的な進歩があり、ガムには消費者ごとに異なる組成とフレーバーがあります。国内のほとんどの企業は、菜食主義者の消費者を引き付けるために、無糖チューインガムに非動物性グリセリンを使用しています。

- カナダは、この地域で無糖チューインガムの売上が最も急成長している国です。カナダにおける無糖チューインガムの販売額は、2024年から2030年にかけてCAGR 3.01%で拡大すると予想されています。消費者が砂糖を使用した製品を控える中、無糖チューインガムの利便性と汎用性により、甘いスナックやキャンディに代わる健康的な選択肢を求める消費者の間で人気が高まっています。

北米の無糖チューインガム市場動向

砂糖の過剰摂取に対する意識の高まりが、地域全体で消費者の無糖ガムへの傾斜をもたらしました。

- 北米では、無糖チューインガムは、砂糖ベースのガムや砂糖ベースのキャンディの代替品として、肥満問題を抱える消費者に好まれています。2022年、米国の肥満有病率は35.2%でした。北米では糖尿病患者の間で無糖ガムの消費が強く奨励されています。

- 無糖チューインガム・セグメントでは、ブランド・ロイヤルティが製品属性の下で重要な価値を獲得しています。北米では、消費者の43%が好きなブランドの無糖ガムを好んで選んでいることが観察されました。Trident、Double Mint、Orbit、Extra、Pur Gumなどが市場で高いシェアを持つブランドです。

- 2023年には、無糖チューインガムの売上が増加しました。2023年、無糖製品は前年比1.34米ドルの成長を記録しました。製品価格の変動は、キシリトール、ガムベース、マルチトールシロップ、マンニトールなどの原材料価格の上下と関連しています。

- 北米では、無糖チューインガムの消費は一般的に健康の観点から見られています。また、無糖チューインガムの売上は、肥満の人の間で無糖製品に対する需要が高まっているかどうかにも左右されます。

北米の無糖チューインガム産業概要

北米の無糖チューインガム市場は適度に統合されており、上位5社で63.39%を占めています。この市場の主要企業は以下の通り。 Chocoladefabriken Lindt & Sprungli AG, Mars Incorporated, Mondelez International Inc., Perfetti Van Melle BV and The Hershey Company.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 流通チャネル

- コンビニエンスストア

- オンライン小売店

- スーパーマーケット/ハイパーマーケット

- その他

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Chocoladefabriken Lindt & Sprungli AG

- Ford Gum & Machine Company Inc.

- Mars Incorporated

- Mazee LLC

- Mondelez International Inc.

- Perfetti Van Melle BV

- Simply Gum Inc.

- The Bazooka Companies Inc.

- The Hershey Company

- The PUR Company Inc.

- Tootsie Roll Industries Inc.

- Xylichew

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Sugar-free Chewing Gum Market size is estimated at 2.76 billion USD in 2025, and is expected to reach 3.39 billion USD by 2030, growing at a CAGR of 4.18% during the forecast period (2025-2030).

Increasing demand for functional products with supermarkets/ hypermarkets and others segment are driving the distribution of sugar-free chewing gum together owing to having a 70% value share in 2023

- The overall distribution channel in North America is playing a vital role in the growth of the sugar-free gum market. Under the distribution segment, retailers offer a wide variety of sugar-free chewing gum products to drag the consumer focus. In addition, these retailers have also segmented sugar-free gum into a wide variety of flavors, textures, and packaging. In 2023, the distribution channel was holding a share of 1.34% as compared to 2022.

- By value, supermarkets and hypermarkets were considered the major retailers in North America. These retailers are selling chewing gum in varied price ranges (low, medium, and high). The average selling price of sugar-free was USD 2.12 in 2023. Due to the respective aspects, consumers are majorly trending toward these retailing units as they promote consumer buying power in this region.

- Convenience stores are considered the second largest retailers in North America. This is because these stores have the capability to offer a greater convenience experience to their consumers. In 2023, it was observed that Becker's owned 45 stores in Ontario.

- With the growing penetration of internet users across North America, the demand for online grocery has become a crucial part of the region's retailing segment. By the end of 2022, the total number of internet users in Mexico was 89.5 million, which was 75.7% of the total population.

- During the forecasted period (2026-2029), it is expected that the market will grow by 2.21%. The major factor that will be driving the sugar-free industry is linked to the growing demand for better health among the American population. It is also expected that sugar-free gum retailers will be introducing gums with unique flavors.

With 8 out of 10 consumers in the United States engaged in sugar reduction, the country experienced the highest demand for sugar-free chewing gums in 2023 in North America

- The North American sugar-free chewing gum market witnessed a growth of 3.4% in 2023 compared to 2022. Increasing awareness about oral health and the impact of sugar on dental health led to a growing demand for sugar-free gum. Sugar-free gums provide a way to enjoy chewing gum while minimizing the risk of tooth decay and cavities.

- By country, the United States is the leading market for sugar-free gums in the region and it is anticipated to grow by 16.1% in 2027 compared to 2023. The chewing gum market is undergoing a paradigm shift toward developing a "sugar-free" front due to the inclination of the population toward sugar-free food and beverages due to the occurrence of diabetes and sugar-related diseases. At the end of 2021, 8 out of 10 United States consumers were engaged in sugar reduction.

- Mexico is the second-leading market for sugar-free chewing gums in the region. The country registered a growth rate of 14.3% from 2021 to 2023. There have been continuous advancements in the types of sugar-free gums due to their popularity, and the gums come in different compositions and flavors for different consumers. Most companies in the country are using non-animal glycerin in sugar-free chewing gums to attract vegan consumers.

- Canada is the fastest-growing country for the sales of sugar-free chewing gums in the region. The sales value of sugar-free chewing gums in Canada is anticipated to expand at a CAGR of 3.01% from 2024 to 2030. As consumers cut back on sugar-based products, the convenience and versatility of sugar-free chewing gums have made them a popular choice among consumers looking for a healthier alternative to sugary snacks and candies.

North America Sugar-free Chewing Gum Market Trends

Growing awareness regarding excessive intake of sugar resulted in consumers' inclination toward sugar-free gums across the region

- In North America, sugar-free chewing gums are preferred by consumers with obesity problems as a replacement for sugar-based gums and sugar-based candies. In 2022, the United States' obesity prevalence was 35.2%. The consumption of sugar-free gums is highly encouraged among diabetic patients in North America.

- In the sugar-free chewing gum segment, brand loyalty acquires a significant value under product attributes. In North America, it was observed that 43% of consumers prefer choosing sugar-free chewing gums of their favorite brands. Trident, Double Mint, Orbit, Extra, Pur Gum, etc., are some brands that hold higher shares in the market.

- In 2023, sugar-free chewing gums witnessed a hike in their sales. In 2023, sugar-free products recorded a Y-o-Y growth of USD 1.34. The fluctuation in the product's price is connected with the rise and fall in the prices of its raw materials, including xylitol, gum base, maltitol syrup, and mannitol.

- In North America, the consumption of sugar-free chewing gum is generally viewed from a health perspective. The sales of sugar-free chewing gum also depend on the growing demand for sugar-free products among individuals with obesity.

North America Sugar-free Chewing Gum Industry Overview

The North America Sugar-free Chewing Gum Market is moderately consolidated, with the top five companies occupying 63.39%. The major players in this market are Chocoladefabriken Lindt & Sprungli AG, Mars Incorporated, Mondelez International Inc., Perfetti Van Melle BV and The Hershey Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Distribution Channel

- 5.1.1 Convenience Store

- 5.1.2 Online Retail Store

- 5.1.3 Supermarket/Hypermarket

- 5.1.4 Others

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 United States

- 5.2.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Chocoladefabriken Lindt & Sprungli AG

- 6.4.2 Ford Gum & Machine Company Inc.

- 6.4.3 Mars Incorporated

- 6.4.4 Mazee LLC

- 6.4.5 Mondelez International Inc.

- 6.4.6 Perfetti Van Melle BV

- 6.4.7 Simply Gum Inc.

- 6.4.8 The Bazooka Companies Inc.

- 6.4.9 The Hershey Company

- 6.4.10 The PUR Company Inc.

- 6.4.11 Tootsie Roll Industries Inc.

- 6.4.12 Xylichew

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 147 Pages

- 納期

- 2~3営業日