北米のガム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America Gums - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 177 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684024

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

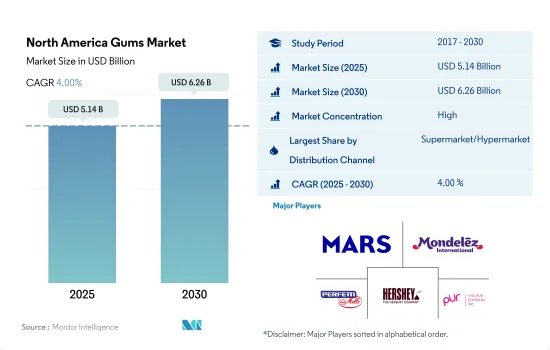

北米のガム市場規模は2025年に51億4,000万米ドルと推定・予測され、2030年には62億6,000万米ドルに達し、予測期間(2025-2030年)のCAGRは4.00%で成長すると予測されます。

スーパーマーケット/ハイパーマーケットとその他セグメントがこの地域のガム流通を牽引し、2023年には70%近い金額シェアを占める。

- スーパーマーケットとハイパーマーケットは、この地域におけるガム販売の主要流通チャネルです。スーパーマーケットとハイパーマーケットにおけるガムの販売量は、2021年から2023年にかけて11%増加しました。これらのチャネルに対する消費者の嗜好は、季節的なオファー、大量購入の割引、単一のマーケットプレースにおける多様なブランドと製品品種へのアクセスによってもたらされます。Safeway、Walmart、Costco、Amazon Fresh、Target、Whole Foods、Publix、Aldiなどのスーパーマーケット・チェーンには、ガムを展示する専用コーナーがあります。

- コンビニエンスストアは、この地域でスーパーマーケット、ハイパーマーケットに次いでガム購入に広く選ばれている流通チャネルです。このセグメントは、2023年には流通チャネルを通じた販売量全体の20%を占めていました。プライベートブランドへの幅広いアクセスと容易なアクセスが、消費者が他の小売チャネルよりも伝統的な食料品店を好む原動力となっています。コンビニエンスストアを通じたガム販売は、2023年から2029年にかけてCAGR 3.41%を記録すると推定されます。

- オンラインチャネルは、ガムの流通チャネルとして最も急速に成長すると予測され、2023年から2029年にかけて金額ベースで4.86%のCAGRが予測されます。インターネット・ユーザーの増加に対応したオンライン・ガム・ショップの増加が、予測期間中のガムのオンライン販売を促進すると予想されます。2022年には、この地域の人口の93.4%がインターネットにアクセスしていました。米国、カナダ、メキシコはインターネット利用者の普及率が高い国です。有機ガム、無糖ガム、フレーバーガムなど幅広い種類のガムを提供する主要オンラインガム小売業者は、Simply Gum、Project 7、Glee Gum、Chewy、Walgreens、iHerb、Vita Cost、Gummi Boutiqueなどです。

米国とメキシコは、2024年にはほぼ85%の金額シェアでガムの地域市場を構成すると予想される。

- 北米のガム市場は、2021年と比較して2022年には6.88%の成長を観察しています。この成長は、チューインガム消費の健康上の利点に関する意識の高まりに関連しています。さらに、この地域の消費者の間では、より健康的な食生活が増加しています。その結果、この地域ではチューインガムとバブルガムの需要が大幅に増加しています。チューインガムやバブルガムには、砂糖を使ったものや砂糖を使わないものなど、さまざまな形態があります。さらに、甘いキャンディーや甘いベースの製品を好む多くの消費者が、砂糖ベースのチューインガムを消費しています。

- 2023年には、米国が最大の成長セグメントであることが観察されました。これは、チューインガムやバブルガムが様々な形状、色、フレーバーなどで入手可能であることが主な原因です。米国では、チューインガム消費者の45.5%がミント味のガムを好み、フルーツ味は29.1%の消費者に好まれています。さまざまなフレーバーのガムが手に入ることで、消費者は自分の好みに合わせてこれらの製品を購入できるため、購買力も促進されます。

- カナダのガム市場は、2021年から2023年にかけてCAGR 5.37%を記録し、最も急成長しているチャネルと考えられています。カナダでは、小売部門ではMars、Ford Gum、Big League Crewなど、さまざまなブランドのガム(チューインガムとバブルガム)を販売しています。こうした点から、顧客は好みに合った様々なブランドの製品を購入することができます。

- 推定・予測期間(2024-2030年)の間に、北米地域のガム市場は7.25%の成長を観察すると推定されます。この成長は、同地域における消費者の口中を爽やかにする製品に対する需要の高まりが主な要因です。

北米ガム市場の動向

健康志向の消費者の増加により、機能性チューインガムの需要が増加。

- チューインガムはこの地域で最も消費されているアイテムの一つです。この地域の消費者は、面白い食感を体験したいときに、バブルガム、シュガーガム、無糖ガムなどのガムを選ぶことが増えています。2022年現在、米国の消費者の59%が定期的にガムを消費しています。ガムは一般的に、口臭を爽やかにし、一日中口腔衛生を維持するために使用されます。

- 北米のガムには、消費者の嗜好やニーズに応える様々な製品特性があります。この地域の多くの消費者は、砂糖の摂取量を減らすために無糖ガムを好みます。無糖ガムは、キシリトール、ソルビトール、ステビアのような代替甘味料で甘くされています。

- 経済パラメータは、北米の消費者のガム購買行動に影響を与える重要かつ主要な要因の一つです。北米では、2023年現在、地元の食料品店で12~60個入りのシンプルな無糖ガムのパッケージの平均価格は、1個当たり1~2米ドルです。

- 歯を清潔に保ち、息を爽やかにするなど、機能的なチューインガムへの消費者の嗜好の高まりが市場を牽引しています。チューインガムには健康上の利点もあります。

北米ガム産業概要

北米のガム市場はかなり統合されており、上位5社で84.87%を占めています。この市場の主要企業は以下の通りです。 Mars Incorporated, Mondelez International Inc., Perfetti Van Melle BV, The Hershey Company and The PUR Company Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- バブルガム

- チューインガム

- 砂糖含有量別

- 砂糖入りチューインガム

- 無糖チューインガム

- 流通チャネル

- コンビニエンスストア

- オンライン小売店

- スーパーマーケット/ハイパーマーケット

- その他

- 国

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Canel's Group

- Ferrero International SA

- Ford Gum & Machine Company Inc.

- GumRunners LLC

- Mars Incorporated

- Mazee LLC

- Mondelez International Inc.

- Perfetti Van Melle BV

- Simply Gum Inc.

- The Bazooka Companies Inc.

- The Hershey Company

- The PUR Company Inc.

- Tootsie Roll Industries Inc.

- Xylichew

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Gums Market size is estimated at 5.14 billion USD in 2025, and is expected to reach 6.26 billion USD by 2030, growing at a CAGR of 4.00% during the forecast period (2025-2030).

Supermarkets/ hypermarkets and the others segment drive the distribution of gums in the region, holding the value share of almost 70% in 2023

- Supermarkets and hypermarkets are the leading distribution channels for gum sales in the region. Volume sales of gums across supermarkets and hypermarkets grew by 11% from 2021 to 2023. Consumer preference for these channels is driven by seasonal offers, discounts on bulk purchases, and access to diversified brand and product varieties in the single marketplace. Supermarket chains such as Safeway, Walmart, Costco, Amazon Fresh, Target, Whole Foods, Publix, and Aldi have a dedicated section to showcase gums.

- Convenience stores are the second most widely preferred distribution channel for purchasing gums in the region after supermarkets and hypermarkets. The segment had a 20% share of the overall volume sales through distribution channels in 2023. The broader reach and easy access to private label brands drive the consumer preference for traditional grocery stores over other retail channels. The gum sales through convenience stores are estimated to register a CAGR of 3.41% from 2023 to 2029.

- The online channel is projected to be the fastest-growing distribution channel for gums, with an anticipated CAGR of 4.86% in terms of value during the period 2023-2029. The increasing number of online gum shops in response to the rising number of internet users is anticipated to drive online sales of gums during the forecast period. In 2022, 93.4% of the region's population had internet access. The United States, Canada, and Mexico are the countries with high penetration of internet users. The leading online gum retailers offering a wide range of gums, including organic, sugar-free, and flavored gums, are Simply Gum, Project 7, Glee Gum, Chewy, Walgreens, iHerb, Vita Cost, and Gummi Boutique, among others.

The United States and Mexico are expected to make up the regional market for gums with almost 85% value share in 2024

- The North American gums market has observed a growth of 6.88% in 2022 as compared to 2021. The growth is associated with the rising awareness about the health benefits of chewing gum consumption. In addition, there is a rise in healthier eating among consumers across the region. As a result, the demand for chewing and bubble gums has been increasing significantly in the region. Chewing gums and bubble gums are available in various formats, including sugar-based and sugar-free products. In addition, many consumers who prefer sweet candy and sweet-based products are consuming sugar-based chewing gums.

- In 2023, it was observed that the United States was the largest growing segment. This is majorly due to the availability of chewing gums and bubble gums in various shapes, colors, flavors, etc. In the United States, 45.5% of chewing gum consumers prefer mint-flavored gums, while fruit flavor is liked by 29.1% of consumers. The availability of gums in different flavors also promotes the consumer's buying power as they can purchase these products in accordance with their preferences.

- The Canadian gums market is considered to be the fastest-growing channel, registering a CAGR of 5.37% from 2021 to 2023. In Canada, the retailing segment sells various gums (chewing gum and bubble gum) from different brands such as Mars, Ford Gum, Big League Crew, and others. These aspects enable the customers to purchase products from different brands that suit their tastes.

- Between the forecast period (2024-2030), it is estimated that the gums market across the North American region will observe a growth of 7.25%. The growth will be majorly associated with the consumer's growing demand for mouth-freshening products in the region.

North America Gums Market Trends

The rising number of health-conscious consumers resulted in increased demand for functional chewing gums due to the health benefits associated with them

- Chewing gums are one of the most consumed items in the region. Consumers in the region increasingly choose gums, including bubble gum, sugar gum, and sugar-free gum, when they want to experience interesting textures. As of 2022, 59% of consumers in the United States regularly consumed gum. Gum is commonly used to freshen breath and maintain oral hygiene throughout the day.

- Gums in North America have various product attributes that cater to consumer preferences and needs. Many consumers in the region prefer sugar-free gums to reduce their sugar intake. Sugar-free gums are sweetened with alternative sweeteners like xylitol, sorbitol, or stevia.

- The economic parameter is one of the important and major factors influencing the consumer's gum-buying behavior in North America. In North America, as of 2023, on average, the cost of a simple package of sugar-free gum that contains 12 to 60 pieces at the local grocery store ranged from USD 1 to USD 2 per individual pack.

- The growing preference of consumers toward functional chewing gums owing to their associated benefits, such as keeping teeth clean and freshening breath, among others, are driving the market. Chewing gum also has certain health benefits associated with it.

North America Gums Industry Overview

The North America Gums Market is fairly consolidated, with the top five companies occupying 84.87%. The major players in this market are Mars Incorporated, Mondelez International Inc., Perfetti Van Melle BV, The Hershey Company and The PUR Company Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Bubble Gum

- 5.1.2 Chewing Gum

- 5.1.2.1 By Sugar Content

- 5.1.2.1.1 Sugar Chewing Gum

- 5.1.2.1.2 Sugar-free Chewing Gum

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Canel's Group

- 6.4.2 Ferrero International SA

- 6.4.3 Ford Gum & Machine Company Inc.

- 6.4.4 GumRunners LLC

- 6.4.5 Mars Incorporated

- 6.4.6 Mazee LLC

- 6.4.7 Mondelez International Inc.

- 6.4.8 Perfetti Van Melle BV

- 6.4.9 Simply Gum Inc.

- 6.4.10 The Bazooka Companies Inc.

- 6.4.11 The Hershey Company

- 6.4.12 The PUR Company Inc.

- 6.4.13 Tootsie Roll Industries Inc.

- 6.4.14 Xylichew

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 177 Pages

- 納期

- 2~3営業日