|

市場調査レポート

商品コード

1684000

南米の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)South America Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 189 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

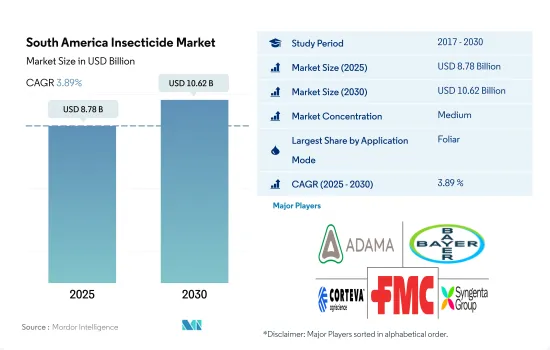

南米の殺虫剤市場規模は2025年に87億8,000万米ドルと推定・予測され、2030年には106億2,000万米ドルに達し、予測期間(2025~2030年)のCAGRは3.89%で成長すると予測されます。

葉面散布は、その有効性と散布時期の柔軟性から市場を独占しています。

- 殺虫剤の葉面散布は、対象害虫を駆除する効果が高いこと、他の方法と比べて散布時間や散布量が柔軟であることなどの要因により、多くの人気を集めました。殺虫剤の葉面散布法は、2022年に53.8%の最高シェアを占め、同年の市場価値は42億1,000万米ドルでした。

- 植物の感染拡大を抑制する殺虫剤種子処理の重要性は、その大幅な市場シェアが例証しています。2022年、南米の種子処理市場は殺虫剤種子処理の優位性が際立っており、全用途の64.9%という素晴らしい市場シェアを占めています。この統計は、昆虫媒介生物と闘い、作物の生産性を守る上で種子処理が有効であるという認識が高まっていることを裏付けています。

- 殺虫剤の土壌施用は、植物の根や下部に深刻な影響を及ぼす土壌伝染性害虫を対象とするもので、この方法は2022年の南米における殺虫剤市場全体の10.5%を占めています。シロイチモジのような土壌伝染性害虫の蔓延は、ダイズでは約25%、トウモロコシでは約64%の根系を減少させることが知られています。フィロファガ・カピラータ(Phyllophaga capillata)とエゴプシス・ボルボセリドゥス(Aegopsis bolboceridus)は、すべての評価変数に被害を与え、ダイズ全体の生産性を58.62%、トウモロコシの生産性を59.76%低下させることが観察されました。

- 南米における殺虫剤の燻蒸と化学的散布の採用は、害虫駆除に有効な方法が異なるため、それぞれの必要性と効果に基づいて増加しています。

市場でのブラジルの優位性は、効果的な害虫駆除の必要性による殺虫剤需要の増加が後押ししています。

- 南米の殺虫剤市場は大幅な拡大を見せており、同地域のさまざまな国が著しい拡大を示しています。この殺虫剤需要の増加は、害虫を効果的に管理し、作物の損失を最小限に抑える必要性が背景にあります。2022年現在、南米は世界の殺虫剤市場において市場シェア全体の24.9%を占めています。

- 2022年には、ブラジルが南米の殺菌剤市場で87.7%という大きなシェアを占め、その優位性を主張しています。ブラジルには広大で多様な農業地帯があり、さまざまな地域でさまざまな作物が栽培されています。この多様性により、作物はさまざまな害虫の被害を受けやすく、殺虫剤の必要性が高まっています。国内で最も頻繁に使用されている殺虫剤の有効成分は、カルバマートとピレスロイドです。

- その他南米は9.0%という大きな市場シェアを持ち、殺虫剤の第2位の消費国となっています。エクアドル、パラグアイ、ペルー、ウルグアイ、ボリビアなどの国々の農家は、虫害による経済的損失を認識するようになってきています。しかし、このような集約的なやり方は、アブラムシ、ウジ、コナジラミ、ノミムシ、カツオブシムシ、ツノゼミ、アザミウマなどの害虫を急速に蔓延させる好条件をもたらしています。これらの害虫は穀物や穀類に大きな脅威を与え、作物への被害や収量の低下をもたらします。そのため、殺虫剤の使用は作物を守り、継続的な生産性を確保するために不可欠となります。

- その結果、予測期間中(2023~2029年)の同市場のCAGRは4.2%に達すると予想され、これは主に農産物の需要増加と、農作物を保護する殺虫剤の重要性の高まりによるものです。

南米の殺虫剤市場動向

南米ではチリが一人当たりの殺虫剤消費率で最高を記録

- 昆虫は葉、茎、根、果実などの植物組織を食害することで、作物に直接的な被害を与えます。この食害は、光合成の低下、成長の阻害、奇形、あるいは植物の枯死をもたらします。こうした悪影響は大幅な収量減につながり、作物全体の生産性に影響を及ぼします。

- 南米では、大豆、トウモロコシ、コーヒー、小麦、サトウキビ、バナナ、柑橘類など、主要作物を含む幅広い作物を栽培しています。これらの作物における主な害虫は、カメムシ、ルーパー、アーミーワーム、アブラムシ、コナジラミなどです。

- 南米ではチリが最大の殺虫剤消費国で、2022年の消費量は1.6kg/haです。チリは農産物、特に果物やワインの主要輸出国です。輸出市場では、害虫の蔓延を防ぎ食品の安全を確保するため、厳しい植物検疫規制や品質基準が設けられていることが多いです。殺虫剤の使用は、これらの要件を遵守し、国際市場におけるチリ産農産物の市場アクセスを守るために極めて重要です。

- パラナ州、リオ・グランデ・ド・スル州、ブラジル中部のセラード地域を含むブラジル南部地域は、大豆、トウモロコシ、綿花の大規模な農業生産で知られています。ブラジルは、秋のアーミーワーム、ルートワーム、ボルワーム、コーンイヤーワームなどの害虫に大きな悩みを抱えており、南米で2番目に殺虫剤の消費量が多く、その消費量は765.6g/haです。

- 南米は熱帯雨林から乾燥・半乾燥地域まで、幅広い気候条件を示しています。こうした多様な農業生態学的条件は、害虫の個体数や動態に影響を与えます。最良の作物保護を提供するためには殺虫剤の使用が必要であり、これが殺虫剤市場をさらに牽引することになります。

シペルメトリンは1トン当たり2万1,080米ドルで最も高価格の殺虫剤

- シペルメトリンはピレスロイド系殺虫剤に属し、菊由来のピレトリンの天然殺虫特性を模倣するように設計された非合成化学物質です。南米では、シペルメトリンはアブラムシ、カイガラムシ、イモムシ、オオヨコバイ、コナジラミなど、幅広い害虫の駆除に使用されています。シペルメトリンの作用機序は昆虫の神経系を混乱させ、麻痺を引き起こし、最終的には死に至らしめるというものです。2022年、シペルメトリンの価格はトン当たり2万1,080米ドルでした。

- イミダクロプリドはネオニコチノイド系殺虫剤で、ネオニコチノイドという化学分類に属します。ネオニコチノイドはニコチンと同様に昆虫の神経系に作用し、神経細胞の過剰刺激を引き起こし、最終的に麻痺や死に至る。この有効成分の2022年の価格は、1トン当たり1万7,170米ドルでした。南米ではイミダクロプリドはアブラムシ、ヨコバイ、コナジラミ、アザミウマ、特定の甲虫類など、さまざまな害虫を効果的に駆除するために広く使用されています。

- マラチオンは有機リン系殺虫剤で、有機リン酸塩の一種に属します。様々な害虫駆除に広く使われています。南米では、さまざまな作物でアブラムシ、ハダニ、アザミウマ、ミバエ、ヨコバイなどの害虫を効果的に駆除するために使用されています。マラチオンの作用機序は、昆虫の適切な神経機能に不可欠な酵素であるアセチルコリンエステラーゼを阻害することです。神経系を混乱させることで、神経細胞に過剰な刺激を与え、麻痺を引き起こし、最終的に対象害虫を死に至らしめる。2022年の価格は1トン当たり1万2,500米ドルで、3つの中で最も手頃な価格の化学物質です。

南米の殺虫剤産業概要

南米の殺虫剤市場は適度に統合されており、上位5社で46.80%を占めています。この市場の主要企業は以下の通りです。 ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- ブラジル

- チリ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用方法

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- アルゼンチン

- ブラジル

- チリ

- その他南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The South America Insecticide Market size is estimated at 8.78 billion USD in 2025, and is expected to reach 10.62 billion USD by 2030, growing at a CAGR of 3.89% during the forecast period (2025-2030).

Foliar mode of application dominated the market due to its effectiveness and flexibility in the time of application.

- The foliar application of insecticides gained much popularity owing to factors like its effectiveness in controlling the target pests, and flexibility in the time and dosage of application compared to other methods. The foliar method of insecticide application accounted for the highest share of 53.8% in the year 2022, with a market value of USD 4.21 billion in the same year.

- The significance of insecticide seed treatment in controlling the spread of plant infections is exemplified by its substantial market share. In 2022, the South American seed treatment market witnessed a notable dominance of insecticide seed treatments, holding an impressive market share of 64.9% of all the application modes. This statistic underlines the growing recognition of the effectiveness of seed treatments in combatting insect vectors and safeguarding crop productivity.

- Soil application of insecticides aims to target soilborne insect pests that can cause severe effects on the root and lower parts of the plants and this method accounted for 10.5% of the total insecticides market in South America in the year 2022. The infestation of soil borne pests like white grub is known to reduce the root system by approximately 25% in soybean and 64% in maize. It was observed that Phyllophaga capillata and Aegopsis bolboceridus damaged all evaluated variables, reducing overall soybean productivity by 58.62% and maize productivity by 59.76%, which can effectively be treated with soil treatment.

- The adoption of fumigation and chemigation of insecticides in South America is increasing based on the need and effectiveness of each method based on the requirement as different methods are effective in controlling different pests.

Brazil's dominance in the market is fueled by the increasing demand for insecticides driven by the necessity for effective insect control

- The insecticide market in South America is witnessing significant expansion, with various countries in the region witnessing remarkable expansion. This increased demand for insecticides is driven by the necessity to effectively manage insect pests and minimize crop losses. As of 2022, South America accounted for 24.9% of the total market share value in the global insecticide market.

- In 2022, Brazil held a significant share of 87.7% in the South American fungicide market, asserting its dominance. Brazil has a vast and diverse agricultural landscape, cultivating a wide array of crops across different areas. This diversity makes crops more vulnerable to a variety of insect pests, resulting in an increased need for insecticides. The most frequently utilized insecticide active ingredients in the country are carbamates and pyrethroids.

- With a significant market share of 9.0%, the Rest of South America ranks as the second largest consumer of insecticides. Farmers in countries like Ecuador, Paraguay, Peru, Uruguay, and Bolivia are increasingly recognizing the economic losses caused by insect infestations. However, this intensive approach also creates favorable conditions for the rapid spread of insect pests, such as aphids, maggots, whiteflies, flea beetles, cutworms, hornworms, and thrips. These pests pose a substantial threat to grains and cereals, resulting in crop damage and diminished yields. Therefore, the use of insecticides becomes essential to safeguard crops and ensure continued productivity.

- As a result, the market is expected to experience a CAGR of 4.2% during the forecast period (2023-2029), primarily driven by the increasing demand for agricultural products and the rising significance of insecticides in protecting crops.

South America Insecticide Market Trends

Chile recorded the highest per capita consumption rate of insecticides in South America

- Insects can cause direct damage to crops by feeding on plant tissues such as leaves, stems, roots, or fruits. This feeding can result in reduced photosynthesis, stunted growth, deformities, or even plant death. These adverse effects can lead to substantial yield losses and affect the overall productivity of the crops.

- South America cultivates a wide range of crops, including major commodities such as soybeans, corn, coffee, wheat, sugarcane, bananas, and citrus fruits. The major pests in these crops include stink bugs, loopers, armyworms, aphids, and whiteflies.

- In South America, Chile is the largest consumer of insecticides, with a consumption of 1.6 kg/ha in 2022. Chile is a major exporter of agricultural products, particularly fruits and wine. Export markets often have stringent phytosanitary regulations and quality standards to prevent the spread of pests and ensure food safety. Insecticide use is crucial to comply with these requirements, safeguarding market access of Chilean produce in international markets.

- The southern regions of Brazil, including the states of Parana, Rio Grande do Sul, and Cerrado region in central Brazil, are known for extensive agricultural production of soybeans, corn, and cotton. They face major concerns with pests like the fall armyworm, rootworm, bollworm, and corn earworm, contributing to Brazil's rank as the second-highest consumer of insecticides in South America, with a consumption rate of 765.6 g/ha.

- South America exhibits a wide range of climatic conditions, from tropical rainforests to arid and semi-arid regions. These diverse agroecological conditions influence pest populations and dynamics. The use of insecticides is necessary to provide the best crop protection, which will further drive the insecticide market.

Cypermethrin is the highest-priced insecticide at USD 21.08 thousand per metric ton

- Cypermethrin belongs to the class of pyrethroid insecticides, which are non-synthetic chemicals designed to mimic the natural insecticidal properties of pyrethrins derived from chrysanthemums. In South America, cypermethrin is used to effectively manage a wide range of pests, including, but not limited to, aphids, beetles, caterpillars, leafhoppers, and whiteflies. The mode of action of cypermethrin involves disrupting the nervous systems of insects, leading to paralysis and, ultimately, their death. In 2022, cypermethrin was priced at USD 21.08 thousand per metric ton.

- Imidacloprid is a neonicotinoid insecticide belonging to the chemical class of neonicotinoids. Neonicotinoids act on the nervous system of insects in a similar way to nicotine, causing overstimulation of nerve cells and ultimately leading to paralysis and death. This active ingredient was priced at USD 17.17 thousand per metric ton in 2022. In South America, imidacloprid is widely used to effectively manage various pests, including aphids, leafhoppers, whiteflies, thrips, and certain beetle species.

- Malathion is an organophosphate insecticide belonging to the chemical class of organophosphates. It is widely used to control a variety of insect pests. In South America, malathion is used to effectively manage pests, such as aphids, spider mites, thrips, fruit flies, and leafhoppers in various crops. Malathion's mode of action involves inhibiting acetylcholinesterase, an enzyme essential for proper nerve function in insects. By disrupting the nervous system, it causes overstimulation of nerve cells, leading to paralysis and, ultimately, death of the target pests. This is the most affordable chemical among the three, with a price of USD 12.5 thousand per metric ton in 2022.

South America Insecticide Industry Overview

The South America Insecticide Market is moderately consolidated, with the top five companies occupying 46.80%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms