|

市場調査レポート

商品コード

1683988

欧州の殺菌剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の殺菌剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 211 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

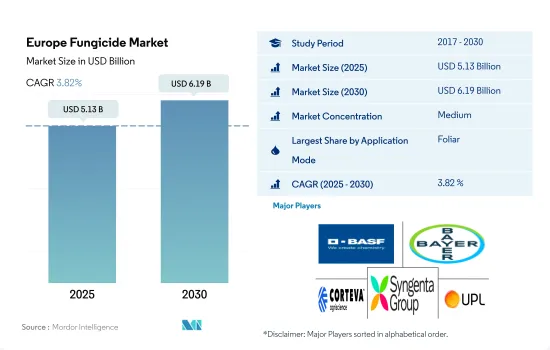

欧州の殺菌剤市場規模は2025年に51億3,000万米ドルと推定・予測され、2030年には61億9,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは3.82%で成長すると予測されています。

作物保護のための効果的な方法へのニーズが、あらゆる適用方法における市場の成長に拍車をかけています。

- 欧州では、作物を保護し高い収量を確保するために、さまざまな散布方法で殺菌剤の成長が見られます。その中でも葉面散布が市場を独占し、2022年には28億2,000万米ドルを占めました。この方法は、果物、野菜、穀物など様々な作物で一般的に使用されています。欧州の農家は、葉面散布を使用して作物を菌類病害から守ることの利点を認識するようになっており、葉面散布法の需要増につながっています。

- 種子治療は、2023年~2029年の予測期間中、欧州の殺菌剤市場で最も急成長しているセグメントの1つであり、CAGRは3.6%を記録すると予想されます。この方法は、発芽および初期成長段階において真菌病原体から早期に保護し、より健全な植物の定着を保証します。欧州では精密農業の採用が増加しています。種子治療は、無駄を省きながら殺菌剤を効率的に使用できるため、精密農業戦略に適しています。

- 化学灌漑法は、2023年から2029年にかけてCAGR 3.4%を記録すると予測されています。マイクロ灌漑の採用が増加し、点滴灌漑の面積が拡大していることが、このセグメントの成長を促進しています。

- 土壌治療の市場価値は、予測期間(2023年~2029年)に9,090万米ドル増加すると予測されます。土壌の健全性の重要性とそれが作物の生産性に及ぼす影響に関する農家や農業利害関係者の認識の高まりが、殺菌剤の需要を促進しています。このため、欧州の殺菌剤市場は予測期間(2023年~2029年)に3.7%のCAGRが見込まれています。

スペインが欧州の殺菌剤市場を独占

- 欧州の殺菌剤市場は歴史的期間に着実な成長を遂げ、同地域は2022年に世界の殺菌剤市場の金額ベースで28.4%のシェアを占める。プロチオコナゾールはこの地域で最も一般的に使用されている殺菌剤です。

- 欧州では小麦が圧倒的に重要な作物です。この地域は世界最大の小麦生産地であり、2021年には1億3,900万トンが生産されました。欧州は主食用穀物の最大の輸出国であり生産国でもあるため、この地域では主に穀物・穀類に殺菌剤が使用されています。穀物・穀類セグメントは2022年に金額ベースで59.2%の市場シェアを占めました。

- フランス、イタリア、スペインは、欧州における殺菌剤の総使用量の約64%を占めています。スペインは2022年に金額ベースで18.1%の最大シェアを占めました。これは、これらの国が小麦やトウモロコシなどの主要作物の生産で優位を占めているためです。しかし、ブドウの晩枯病、早枯病、うどんこ病、フザリウム枯病、セプトリア病、細菌性疫病などの病気が、この地域の主要作物を襲う一般的な病気です。殺菌剤抵抗性の発生は、効果的な病害管理のための殺菌剤の選択肢を狭めるため、重要な課題となっています。ロシアやオランダなどの各国政府は、新たな病害とそれに対抗する効果的な殺菌剤を発見するための研究イニシアチブに投資しており、農家を支援する制度を立ち上げています。

- 政府によるこのような政策と農民の意識の高まりが、作物保護慣行の採用をさらに後押ししています。このような要因が市場の成長に寄与し、予測期間(2023年~2029年)のCAGRは3.7%を記録すると予想されます。

欧州の殺菌剤市場の動向

病害の蔓延と作物損失の増加が殺菌剤の消費量増加につながっている

- 欧州では、作物病害に関連する経済的損失の増加により、殺菌剤の消費が増加しています。消費量は2019年から2022年には1ヘクタール当たり32.7%増加しました。同地域における殺菌剤の使用は、気候条件の変化、殺菌剤耐性の開発、侵入真菌種により増加すると予測されています。

- 穀物・穀類に影響を及ぼす真菌病には、さび病、うどんこ病、スマット病、フザリウム菌核病があります。これらの病害は穀物・穀類にとって大きな脅威であり、収穫量の減少や収穫物の品質低下をもたらす可能性があります。例えば、小麦さび病は、無処理の感受性の小麦では最大100%の作物損失を引き起こす可能性があります。こうした要因から、欧州ではこれらの病害を防除・管理し、より高い収量と作物の品質向上を確保するために、殺菌剤が広く使用されています。

- イタリアでは殺菌剤の消費量が大幅に増加しています。殺菌剤の消費量は2022年に前年から2,300g/ha増加しました。これは、作物病害の発生が増加し、農業生産が拡大し、作物の収量と品質を向上させたいという願望があるためです。

- 食糧生産は将来の人口を維持するために必要です。食料生産の拡大は、より多くの農地を利用し、1ヘクタールあたりの収穫量を増やすことで達成できるかもしれないです。1ヘクタールあたりの収量を高めるための重要な手段のひとつが、植物保護製品の使用です。殺菌剤などの製品は、植物を有害な病気から守るのに役立つからです。

- そのため、作物の病害の発生が増加し、作物を保護し収量を増加させるために、殺菌剤の消費が増加すると予想されます。

テブコナゾールは他の殺菌剤有効成分と比較して最も高い価格を維持しています。

- トリアゾール系殺菌剤の一種であるテブコナゾールは、植物病害の治療と予防の両方を行う全身性で知られる有効成分です。テブコナゾールは、真菌、細菌、ウイルスに効果的に対抗し、植物を保護するために、いくつかの異なる一般的な殺菌剤製品に使用されています。テブコナゾールの全身的なアプローチは、胞子の拡散を妨げ、成長を抑制し、ブドウ、サクランボ、アーモンド、穀物、キャノーラなどの作物に影響を与える有害な真菌に対して人気のある選択肢となっています。2022年の価格は1トン当たり8,700米ドルでした。

- 農業で広く使用されている殺菌剤であるアゾキシストロビンは、抗真菌剤として最も幅広い活性スペクトルを持っています。アゾキシストロビンは強力な有効成分として機能し、小麦栽培を中心に様々な作物で広く利用されています。葉斑病、さび病、うどんこ病、べと病、ネットブロッチ、疫病などの重要な病害を効果的に防除します。特にドイツはアゾキシストロビンの大半をインドから輸入しており、2022年の市場価格は1トン当たり4,400米ドルに達しました。

- メタラキシルは、ジャガイモ、ブドウ、レタスやキュウリなどの野菜などの作物に一般的に散布されます。メタラキシルは、ジャガイモでは晩枯病、ブドウや野菜ではべと病などの病害を効果的に防除します。メタラキシルの使用は、これらの真菌感染症の管理に役立ち、欧州農業におけるより健康的で生産性の高い作物収量に貢献します。2018年から2022年にかけて、メタラキシルの価格は顕著な上昇を経験し、1メートルトン当たり235.7米ドルの上昇となりました。現在、メートルトン当たり4,400米ドルです。

欧州の殺菌剤産業の概要

欧州の殺菌剤市場は中程度に統合されており、上位5社で64.73%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001690

The Europe Fungicide Market size is estimated at 5.13 billion USD in 2025, and is expected to reach 6.19 billion USD by 2030, growing at a CAGR of 3.82% during the forecast period (2025-2030).

The need for effective methods for crop protection is fueling the market's growth in all application methods

- Europe is witnessing the growth of fungicides in various application modes to protect crops and ensure high yields. Among these modes, foliar application dominated the market, which accounted for USD 2.82 billion in 2022. This method is commonly used in various crops, including fruits, vegetables, and cereals. Farmers in Europe are increasingly recognizing the benefits of using foliar applications to protect their crops from fungal diseases, leading to higher demand for foliar methods.

- Seed treatment is expected to be one of the fastest-growing segments in the European fungicide market during the forecast period 2023-2029, registering a CAGR of 3.6%. This method provides early protection against fungal pathogens during germination and early growth stages, ensuring healthier plant establishment. The adoption of precision agriculture practices has increased in Europe. Seed treatment fits well into precision agriculture strategies, as it allows for the efficient use of fungicides while reducing wastage.

- The chemigation method is anticipated to register a CAGR of 3.4% during 2023-2029. The expansion of area under drip irrigation with the rising adoption of micro-irrigation is driving the growth of this segment.

- The market value of soil treatment is expected to increase by USD 90.9 million during the forecast period (2023-2029). The rising recognition among farmers and agricultural stakeholders regarding the significance of soil health and its influence on crop productivity is driving the demand for fungicides. Thus, the European fungicide market is expected to witness a CAGR of 3.7% during the forecast period (2023-2029).

Spain dominates the European fungicide market

- The fungicides market in Europe witnessed steady growth during the historical period, with the region occupying a share of 28.4% by value of the global fungicides market in 2022. Prothioconazole is the most commonly used fungicide in the region.

- Wheat is by far the most important crop throughout Europe. The region is the world's largest wheat producer and contributed 139 million metric tons in 2021. Fungicides are primarily used in grains and cereals in the region, as Europe is also the largest exporter and producer of staple grains. The grains and cereals segment occupied a market share of 59.2% by value in 2022.

- France, Italy, and Spain account for approximately 64% of the total use of fungicides in Europe. Spain held the largest share of 18.1% by value in 2022. This is due to the predominance of these countries in the production of major crops, such as wheat and corn. However, diseases like grape late blight, early blight, powdery mildew, downy mildew, Fusarium wilting, Septoria, and bacterial blight are the common diseases attacking major crops in the region. The occurrence of fungicide resistance presents a significant challenge as it limits fungicide choices for effective disease management. Governments of various countries, such as Russia and the Netherlands, are investing in research initiatives to discover new diseases and effective fungicides to combat them, along with launching supportive schemes for farmers.

- Such policies initiated by governments and a rise in awareness among farmers have further encouraged the adoption of crop protection practices. Such factors are expected to contribute to the market's growth, which is anticipated to record a CAGR of 3.7% during the forecast period (2023-2029).

Europe Fungicide Market Trends

The increasing disease infestation and rising crop losses are leading to an increase in the consumption of fungicides

- Europe is experiencing an increase in the consumption of fungicides due to the rising economic losses associated with crop diseases. The consumption increased by 32.7% per hectare in 2022 from 2019. Fungicide use in the region is predicted to increase because of changes in climatic conditions, the development of fungicide resistance, and invasive fungal species.

- The fungal diseases affecting grains and cereals include rust, powdery mildew, smut, and fusarium head blight. These diseases pose a substantial threat to grains and cereals, as they may result in yield losses and reduce the quality of the harvested crops. For instance, wheat rust may cause crop losses of up to 100% in untreated susceptible wheat. Due to these factors, fungicides are extensively used in Europe to control and manage these diseases, ensuring higher yields and better crop quality.

- The region has witnessed a significant increase in the consumption of fungicides in Italy. The consumption of fungicides increased by 2.3 thousand g/ha in 2022 from the previous year. It was because of the rising occurrence of crop diseases, the expansion of agricultural production, and the desire to enhance crop yields and quality.

- Food production is required to sustain the future population. Growth in food production may be achieved with the use of more farmland and an increase in yield per hectare. One of the important means to bring about high yields per hectare is the use of plant protection products because products such as fungicides help protect plants from harmful diseases.

- Therefore, due to the increasing occurrence of crop diseases and to protect and increase yields of the crops, the consumption of fungicides is expected to increase.

Tebuconazole holds the highest price compared to other active ingredients of fungicide

- Tebuconazole, part of the triazole fungicide family, is an active ingredient known for its systemic nature, providing both curative and preventive control over plant diseases. Tebuconazole is used in several different popular fungicide products to protect plants, effectively countering fungi, bacteria, and viruses. Tebuconazole's systemic approach hinders spore spread and curbing growth, making it a popular choice against harmful fungi affecting crops like grapes, cherries, almonds, cereals, canola, and other crops. Its value in 2022 stood at USD 8.7 thousand per metric ton.

- Azoxystrobin, a widely used fungicide in agriculture, has the broadest spectrum of activity as an antifungal agent. It serves as a potent active ingredient and is extensively utilized across various crops, with a significant focus on wheat farming. It effectively controls important diseases such as leaf spots, rusts, powdery mildew, downy mildew, net blotch, and blight. Notably, Germany imports most of its azoxystrobin from India, and its market value in 2022 amounted to USD 4.4 thousand per metric ton.

- Metalaxyl is commonly applied to crops such as potatoes, grapes, and vegetables like lettuce and cucumbers. Metalaxyl effectively controls diseases such as late blight in potatoes and downy mildew in grapes and vegetables. Its application helps manage these fungal infections, contributing to healthier and more productive crop yields in European agriculture. Between 2018 and 2022, the price of metalaxyl experienced a notable rise, with an increase of USD 235.7 per metric ton. Currently, it stands at USD 4.4 thousand per metric ton.

Europe Fungicide Industry Overview

The Europe Fungicide Market is moderately consolidated, with the top five companies occupying 64.73%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Ukraine

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Ukraine

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms