|

市場調査レポート

商品コード

1683985

中国の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 167 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

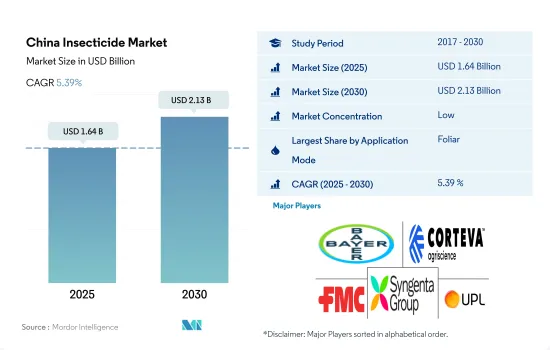

中国の殺虫剤市場規模は2025年に16億4,000万米ドルと推定され、2030年には21億3,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.39%で成長する見込みです。

害虫圧力の上昇、農作物損失の増加、効果的な害虫駆除方法の必要性が殺虫剤需要を促進している

- 中国の殺虫剤市場は、さまざまな散布方法で成長を遂げています。こうした多様な散布技術は、害虫を効果的に駆除し、作物を確実に保護するための幅広い選択肢を提供します。

- 中国の殺虫剤市場を独占しているのは葉面散布法です。この分野は2023年から2029年にかけて金額ベースでCAGR 5.8%を記録すると予測されています。機械化、強化された作物品種、高度な農業技術などの近代的農業慣行の急速な導入が、この成長の主要な推進力となっています。農家がこうした進歩を採用するにつれて、作物の収量を最適化する上で効果的な害虫駆除が果たす役割を認識するようになっています。この認識は、中国における害虫管理戦略の不可欠な一部として、特に葉面散布による殺虫剤の需要をさらに促進しています。

- 2023年から2029年の間に、商業用作物における殺虫剤種子処理市場は450万米ドル成長すると予測されています。中国の大規模商業生産者は、種子処理を標準的な方法として採用しています。この方法を採用することで、彼らは価値の高い作物への投資を保護する利点を認識しています。

- 土壌処理は、中国の殺虫剤市場で最も急成長しているセグメントの1つであり、予測期間中に金額ベースでCAGR 5.2%を記録すると予想されています。同国の農家は、長期的な害虫駆除、土壌伝染性病害の予防、作物全体の健全性と生産性の向上に有効であることから、この方法を害虫管理戦略に取り入れる傾向が強まっています。したがって、中国の殺虫剤市場は2023年から2029年にかけて金額ベースでCAGR 5.7%を記録すると予測されます。

中国の殺虫剤市場動向

農薬使用量のゼロ成長とIPM戦略により、1ヘクタール当たりの殺虫剤消費量が大幅に減少

- 中国の1ヘクタール当たりの殺虫剤消費量は、2017年から2022年にかけて13.1%減少したが、これはいくつかの要因によるものです。近年、中国は殺虫剤の使用量を削減し、有害な殺虫製品を禁止し、化学農薬消費量のゼロ成長を達成することを目的としたいくつかの政府政策を実施しています。これらの政策は、持続可能な農業を推進し、農法が環境に与える影響を最小限に抑えるという、国の広範な取り組みの一環です。その結果、遺伝子組み換え作物や植物由来のプロテアーゼ阻害剤の使用など、害虫駆除の代替方法へとシフトしています。

- 遺伝子組み換え作物(GMO)としても知られるトランスジェニック作物は、特定の害虫に対する抵抗性を組み込んで開発されました。天然の害虫抵抗性種の遺伝子を作物に導入することで、化学殺虫剤を使わずに特定の害虫から作物を守ることができます。このアプローチは中国で人気を博しており、遺伝子組み換え綿花、トウモロコシ、その他の作物の栽培に成功しています。

- 遺伝子組み換え作物に加え、中国は合成殺虫剤に代わる天然物質として、植物由来のプロテアーゼ阻害剤の使用を模索しています。プロテアーゼ阻害剤は、昆虫の様々な生理作用に関与する酵素であるプロテアーゼの活性を阻害する物質です。この阻害剤を農作物に取り入れることで、害虫の消化器官を混乱させ、植物への害を少なくすることができます。

- 上記のような政府政策の実施と、代替害虫駆除方法の採用増加により、中国では1ヘクタール当たりの殺虫剤使用量が減少しています。

有効成分の価格は、国内の天候、病気の発生、エネルギー価格、人件費などの要因に大きく影響されます。

- 中国では、作物害虫の被害を受ける農地が過去50年間で4倍に増加しているが、これは主に気候変動が原因です。中国で最も多く発生している害虫は、蛾や蝶を含む鱗翅目(および秋のアーミーワーム)で、被害を受けた農地の3分の1以上を占めています。次いでアブラムシ、セミ、ヨコバイを含む同翅目です。

- シペルメトリンはピレスロイド系農薬の中で最も広く使用されており、中国では野菜や果実のミバエ、ホウキムシ、メアリ虫など多くの害虫を駆除しています。2022年には1トン当たり2万900米ドルと評価されました。

- マラチオンは、アブラムシ、ノミ、その他多くの貴重な作物の吸汁性害虫など、幅広い害虫駆除に使用されます。中国で広く栽培され、マラチオンを頻繁に使用する5つの作物は、チェリートマト、ブロッコリー、桑、クランベリー、イチジクです。2022年の価格は1トン当たり1万2,400米ドルでした。中国は潜在的な環境リスクを低減するため、低毒性で高効率の農薬の開発に専念しているため、低毒性はマラチオンの最大の利点の1つです。このような要因は、中国におけるマラチオンの価格にさらに影響を与えると思われます。

- イミダクロプリドは典型的なネオニコチノイド系殺虫剤で、2022年の価格はトン当たり1万7,000米ドルです。イミダクロプリドは主に稲、小麦、野菜、綿花などの作物のプラントホッパーやアブラムシの防除に用いられます。イミダクロプリドの最大消費国はコメであり、小麦は中国で栽培されている作物の中で第2位です。

- 有効成分の価格は、国内の天候、病気の発生、エネルギー価格、人件費などの要因に大きく影響されます。

中国の殺虫剤産業の概要

中国の殺虫剤市場は細分化されており、上位5社で37.15%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用方法

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001687

The China Insecticide Market size is estimated at 1.64 billion USD in 2025, and is expected to reach 2.13 billion USD by 2030, growing at a CAGR of 5.39% during the forecast period (2025-2030).

The rising pest pressure, increasing crop losses, and the need for effective pest control methods are driving the demand for insecticides

- The Chinese insecticide market is experiencing growth across various application methods. These diverse application techniques offer a wide range of options to effectively control insect pests and ensure crop protection.

- The foliar application method dominates the insecticide market in China. This segment is projected to register a CAGR of 5.8% in terms of value from 2023 to 2029. The rapid adoption of modern agricultural practices, such as mechanization, enhanced crop varieties, and advanced farming techniques, has been a key driver of this growth. As farmers adopt these advancements, they are increasingly realizing the role of effective pest control in optimizing crop yields. This recognition has further fueled the demand for insecticides, specifically through foliar application, as an essential part of pest management strategies in China.

- Between 2023 and 2029, the insecticide seed treatment market in commercial crops is projected to grow by USD 4.5 million. Large-scale commercial growers in China are adopting seed treatment as standard practice. By adopting this method, they are recognizing the advantages of protecting their investments in highly valuable crops.

- Soil treatment is one of the fastest-growing segments in the insecticide market in China, which is expected to register a CAGR of 5.2% in terms of value during the forecast period. Farmers in the country are increasingly incorporating this method into their pest management strategies due to its effectiveness in long-term pest control, prevention of soil-borne diseases, and enhancement of overall crop health and productivity. Therefore, the Chinese insecticide market is forecast to register a CAGR of 5.7% in terms of value during 2023-2029.

China Insecticide Market Trends

Zero growth in pesticide usage and IPM strategies have contributed to a significant reduction in the per hectare insecticide consumption

- The consumption of insecticides in China per hectare decreased by 13.1% from 2017 to 2022, attributed to several factors. In recent years, China has implemented several government policies aimed at reducing the usage of insecticides, banning harmful insecticidal products, and achieving zero growth in chemical pesticide consumption. These policies are part of the country's broader efforts to promote sustainable agriculture and minimize the environmental impact of agricultural practices. As a result, there has been a shift toward alternative methods of pest control, including the use of transgenic crops and plant-derived protease inhibitors.

- Transgenic crops, also known as genetically modified organisms (GMOs), have been developed with built-in resistance to certain pests. Introducing genes from naturally pest-resistant species into crops can help them defend themselves against specific insects without the need for chemical insecticides. This approach has gained traction in China, where genetically modified cotton, maize, and other crops have been successfully cultivated.

- In addition to transgenic crops, China has been exploring the use of plant-derived protease inhibitors as a natural alternative to synthetic insecticides. Protease inhibitors are substances that inhibit the activity of proteases, which are enzymes involved in various physiological processes of insects. Incorporating these inhibitors into crops can aim to disrupt the digestive systems of insect pests, rendering them less harmful to plants.

- The implementation of the above-mentioned government policies and the rising adoption of alternative pest control methods have contributed to a reduction in the usage of insecticides per hectare in China.

Active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country

- The amount of farmland hit by crop pests in China has quadrupled in the past 50 years, mainly due to climate change. The most prevalent pests in China are lepidoptera, the order that includes moths and butterflies (and fall armyworms), which accounted for more than a third of the affected cropland. This was followed by homoptera, which includes aphids, cicadas, and leafhoppers.

- Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at a price of USD 20.9 thousand per metric ton in 2022.

- Malathion is used to control a wide range of pests, including aphids, fleas, and other sucking pests on a number of valuable crops. Five crops that are extensively grown in China that use malathion frequently are cherry tomato, broccoli, mulberry, cranberry, and fig. It was valued at a price of USD 12.4 thousand per metric ton in 2022. Low toxicity is one of malathion's largest advantages, as China is dedicated to developing low-toxic and highly efficient pesticides to reduce potential environmental risks. Such factors will further influence the price of malathion in China.

- Imidacloprid is a typical neonicotinoid insecticide, priced at USD 17.0 thousand per metric ton in 2022. Imidacloprid is mainly used in the control of planthoppers and aphids on crops like rice, wheat, vegetables, and cotton. Rice is the largest consumer of imidacloprid, and wheat ranks second among crops cultivated in China.

- The active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country.

China Insecticide Industry Overview

The China Insecticide Market is fragmented, with the top five companies occupying 37.15%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms