|

市場調査レポート

商品コード

1911807

欧州のLED照明:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のLED照明:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 161 Pages

納期: 2~3営業日

|

概要

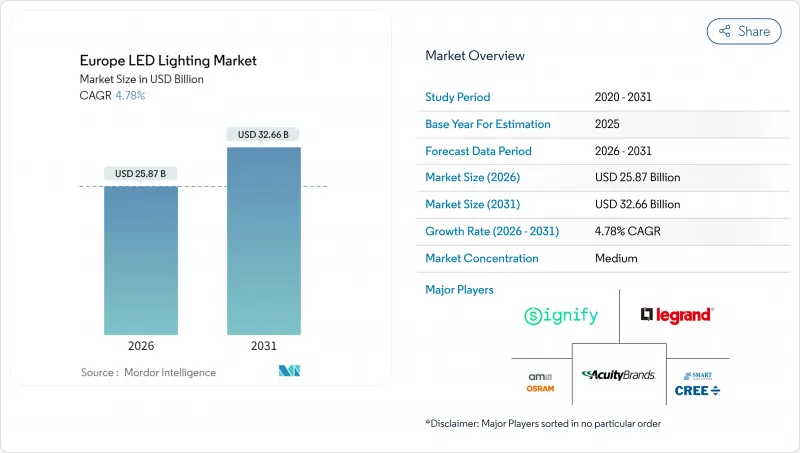

欧州のLED照明市場は、2025年に246億9,000万米ドルと評価され、2026年の258億7,000万米ドルから2031年までに326億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは4.78%と見込まれます。

この成長は、純粋な技術革新よりも規制順守と持続可能性目標が優先される、成熟した置換主導のサイクルを反映しています。EU全域でのエネルギー効率義務化、ハロゲン灯や蛍光灯の段階的廃止、企業のネットゼロ達成ロードマップが改修需要の高まりを維持する一方、ルーメン当たりのコスト低下とスマートシティ入札が新規設置機会を拡大しています。既存サプライヤーは、設置サービス、コネクテッド照明プラットフォーム、循環型経済設計を活用してシェアを守りますが、電子商取引チャネルはニッチな新規参入者の参入障壁を低下させています。希土類蛍光体に関するサプライチェーンリスク、エコデザインおよびWEEE義務の管理負担は、短期的な上昇余地を抑制する一方で、潜在的な新規競合他社を阻み、規模の大きいプレイヤーの利益率を安定させます。

欧州のLED照明市場の動向と分析

厳格なEUエネルギー効率規制

2024年7月に法的効力を発効した「持続可能な製品のためのエコデザイン規制(ESPR)」は、低エネルギー消費、長寿命、高い修理可能性といったLED技術に固有の特性を備えた製品を優遇することで、調達形態を再構築します。2027年導入予定のデジタル製品パスポートでは、メーカーが環境フットプリントを文書化することが義務付けられ、これにより従来型照明器具のコンプライアンス負担が増大し、ライフサイクルデータを既に公表している確立されたLEDブランドへの供給者選好が強まります。また、本規制では2026年以降、未販売品の廃棄が禁止されるため、流通業者は在庫管理の改善と非適合在庫の早期処分を迫られます。公共部門の資金は、イタリアの国家復興・レジリエンス計画(エネルギー転換プロジェクトに555億2,000万ユーロ=627億4,000万米ドルを配分)などの施策を通じて、適合照明機器へ集中的に投入されます。

ハロゲンランプおよび蛍光灯の急速な段階的廃止

EUおよび英国の規制により従来型ランプは流通から排除され、施設は予算サイクルに関わらずLEDへの移行を余儀なくされています。北欧諸国では最も厳しい廃止期限が設定されており、在庫豊富なサプライヤーを優遇する地域的な発注急増を引き起こしています。統合型LED照明器具は筐体全体を置き換えることが多いため、数量が安定しているにもかかわらず単価が上昇し、平均販売価格を引き上げています。ターンキー設置サービスを備えたメーカーは、規制順守の緊急性を活用して保守契約をバンドルし、顧客の囲い込みを強化しています。

中小企業における価格敏感型改修の投資回収期間

中小企業では、エネルギー節約効果が2年以内に資本支出を回収できない場合、アップグレードを先送りします。これにより、規制期限が迫っているにもかかわらず、改修量は伸び悩んでいます。デンマークのルメガ制度のようなパフォーマンス契約モデルは初期費用を不要にしますが、申請者を躊躇させる資格要件を設けており、設置ベースのかなりの部分が旧式の照明に依存したままとなっています。

セグメント分析

照明器具カテゴリーは、光エンジン・光学系・制御機能を統合した完全設計済み器具の需要により、2025年に欧州のLED照明市場の62.10%のシェアを獲得しました。セグメント収益は平均販売価格の上昇とプロジェクトベースの設置サービスにより恩恵を受けています。ランプは絶対値では小規模ながら、コスト低下とスマート電球機能による改修需要の喚起により、2031年までCAGR7.45%で成長すると予測されています。トラック照明および非常用照明器具は、保険規制により適合器具が義務付けられる商業オフィスで採用されています。LEDVANCE社のEVERLOOPシリーズのような循環型経済設計は、交換可能なモジュールがライフサイクルを延長し、ESPR修理可能性要件を満たす方法を示しています。

数量ベースでは、ランプの出荷台数がより急速に増加します。交換作業に配線工事が不要なため、中小企業の資金繰りの制約に適合するからです。一方、照明器具プロジェクトはビル管理システムとの統合が一般的であり、施設管理者が占有率分析を通じて収益化するデータストリームを生成します。このサービス層がプレミアム価格設定を支え、コモディティ化が進むハードウェア市場における利益率圧縮のリスクを軽減します。

卸売・小売ネットワークは2025年時点で欧州のLED照明市場の51.70%のシェアを維持しており、これは物流一括化と販売前設計支援を重視する電気工事会社によるものです。一方で電子商取引はCAGR5.75%で拡大しており、透明性のある価格設定と迅速な配送を重視する中小企業に対応しています。メーカーは現在ハイブリッドモデルを展開しており、例えばIKEAではJETSTROMスマートパネルのオンライン注文と店舗での設定サポートを組み合わせています。大規模プロジェクトでは現場監査や特注の照明設計が不可欠なため、直接販売は依然として重要です。

デジタルプラットフォームにおける価格透明性は、流通業者のマージンを圧縮する一方で、サプライヤーにリアルタイムの需要データを提供し、予測精度を向上させます。これに対し流通業者は、現場での試運転や保証管理といった付加価値サービスを多層化することで、自らの存在意義を守ろうとしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUの厳格なエネルギー効率規制

- ハロゲンランプおよび蛍光灯の急速な段階的廃止

- 企業のネットゼロ目標が改修を促進

- ルーメン当たりのLEDコストの低下

- オンサイト再生可能エネルギー+直流マイクログリッドの導入

- IoTセンサーを組み込んだスマートシティ入札案件

- 市場抑制要因

- 中小企業における価格感応度の高い改修投資回収期間

- 希土類蛍光体のサプライチェーン変動性

- EUエコデザインの複雑性/WEEE(廃電気電子機器)指令への適合

- 接続型照明システム向けの熟練設置技術者の不足

- 業界バリューチェーン分析

- マクロ経済要因の影響

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- ランプ

- 照明器具/ 照明装置

- 流通チャネル別

- 直販

- 卸売/小売

- 電子商取引

- 設置タイプ別

- 新規設置

- 改修設置

- 用途別

- 商業オフィス

- 小売店舗

- ホスピタリティ

- 産業

- 高速道路・一般道路

- 建築

- 公共施設

- 病院

- 園芸・庭園

- 住宅

- 自動車

- その他(化学、石油・ガス、農業)

- エンドユーザー別

- 屋内

- 屋外

- 自動車

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- スウェーデン

- ポーランド

- ロシア

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Signify N.V.

- Zumtobel Group AG

- Osram Licht AG(ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand S.A.

- Eaton Corporation plc(Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione S.p.A.

- Glamox AS

- Cree Lighting Europe S.p.A.

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Samsung Electronics Europe(LED business)

- LG Innotek Europe GmbH

- Valmont Industries(EU lighting poles)

- Opple Lighting Europe B.V.