北米の二次包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America Secondary Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683808

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

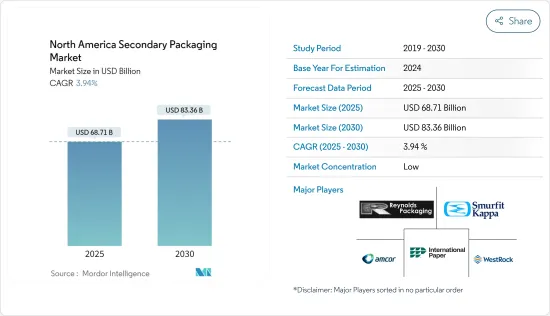

北米の二次包装の市場規模は2025年に687億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.94%で、2030年には833億6,000万米ドルに達すると予測されています。

米国とカナダは巨大な消費者市場であり、人口の購買力が大きいため、あらゆるパッケージ・サプライヤーにとって有利な市場となっています。その結果、北米の二次包装市場は、食品包装の需要拡大、eコマース取引の相次ぐ成功、包装輸送の安全性への要求から、今後1年間で成長すると予測されます。

主なハイライト

- 包装における環境に優しい材料の使用の増加が北米の二次包装市場を牽引しています。リサイクル可能、生分解性、再利用可能、無毒性で環境への影響が少ない包装は環境に優しいと考えられています。環境に優しい包装資材の必要性は、飲食品業界や家庭用ケア用品メーカーを含むエンドユーザーにとってますます明白になってきています。折りたたみカートンや段ボール箱のような包装形態は、板紙のようなリサイクルや生分解が可能な素材で構成されているため、環境に悪影響を及ぼさないです。

- 人々の多忙なライフスタイルにより、コンビニエンス・フードの需要は増加傾向にあります。段ボール包装は製品からの湿気を防ぎ、長時間の輸送にも耐えるため、特に二次包装や三次包装において、より良い結果を顧客に提供するために段ボール包装を採用する企業が増えています。パン、肉製品、その他の生鮮品などの加工食品は、これらの包装材を一度使用する必要があるため、需要が高まっています。

- 段ボールはリサイクルが容易で、パルプ・製紙業界はすでに新世代の段ボールへの転換に長けているため、持続可能性への関心がバリューチェーン全体で高まるにつれて、段ボールは包装材としてますます一般的になりつつあります。このような利点から、段ボールの保護フォームは、発泡ポリスチレン(EPS)のようなポリマーベースの代替品よりも人気を博しています。

- さらに、宅配便やメッセンジャーの収益が増加していることは、製品をある場所から別の場所に運ぶ際に、段ボールや紙器包装などの二次包装が使用されていることを示しています。米国商務省によると、2021年、米国の宅配便・メッセンジャーの営業収入はほぼ1,379億1,000万米ドルでした。UPSは米国最大の宅配便・配達サービス業者で、宅配便市場の約40%を占めています。

- 二次梱包は依然として環境問題を引き起こしているが、解決すべき課題は他にもあります。オンライン購入では、粗悪な二次梱包や不十分な二次梱包のために、欠陥のある、不完全な、あるいは不正確な製品を受け取るという煩わしさや失望に誰もが遭遇しています。しかし、二次包装は一次包装の後に行われるため、停止による問題は他の生産ラインに影響を及ぼします。生産と納品計画は、ダウンタイムによって中断され、製品の廃棄を増加させ、人件費を経費欄に戻すことになります。生産計画には、事前の計画によって停止を予測し、削減することが理想的です。

北米の二次包装市場の動向

コンシューマーエレクトロニクスが著しい成長を遂げる

- 家電メーカーは、消費者主導の持続可能な包装に加え、政府や法律にも後押しされています。これは特に米国で顕著で、生産者責任プログラムの拡大、使い捨て包装の制限、その他の問題の法制化が検討されています。

- 折りたたみカートンや段ボール箱などの二次包装は、重量物や小型電気部品の包装に使用されています。段ボール箱は、家電製品、冷蔵庫、HVACユニットなどの消費者向け製品を包装しています。これらとは別に、サーキットブレーカー、テープ、電球などの小型の電気部品や付属品も、二次包装に紙ベースの材料を使用しています。

- コンシューマーテクノロジー協会によると、米国市場におけるコンシューマーエレクトロニクス(CE)の小売売上高は、2015年から2022年にかけて着実に増加しました。予測によると、2023年の米国における家電小売売上高は4,850億米ドルの成長が見込まれています。OLEDテレビの売上は2023年に23億米ドルに達する見込みです。

- 電子機器包装における偽造防止への強いニーズが北米市場を牽引しています。包装には、バーコード、ホログラム、シーリングテープ、高周波識別装置など、表向きと裏向きの技術が使用され、商品の完全性を保護しています。新興経済国でのeコマースの急成長は、世界の偽造防止電子機器包装業界に利益をもたらしています。

- さらに、環境に優しい包装が電気機器に普及しつつあります。政府当局や規制当局はグリーン包装の採用を強力に推進しています。ブランドと顧客の双方が、環境に優しい包装や、生分解性のない包装ゴミから環境を守ることの重要性を認識するようになっています。

著しい成長が期待されるカナダ

- カナダの二次包装市場は、前年に67億9,000万米ドルと評価されました。段ボール包装は、様々な商品を保護し輸送する経済的な方法です。段ボールの軽量性、生分解性、リサイクル性といった特質により、段ボールはパッケージングビジネスにおいて不可欠な要素となっています。シールドエアーは、2025年までに100%リサイクルまたは再利用可能なパッケージングを作ることに注力します。同社のソリューションの約50%はすでにリサイクル素材で作られています。

- 市場での存在感と地位を向上させるため、カナダのベンダーは成長、パートナーシップ、コラボレーションの取り組みに注力しています。同様に、2022年12月、タイタン・コルゲーテッドとその関連会社オール・ボックスド・アップは、米国を拠点とする持株会社UFPインダストリーズの一部門であるUFPパッケージングに買収されました。買収された会社は、オール・ボックスド・アップを通じて米国全土に流通する標準サイズを製造しています。

- 新興国のeコマース市場は、特に運輸・物流分野のプレーヤーから段ボールや紙製品の需要を生み出しています。順応性があり、手頃な価格である紙ベースのパッケージは、多くの品目を運び、保護し、保存するために使用されてきました。

- Worldpayによると、モバイルeコマースは2021年にカナダで280億米ドルを超える収益を上げ、これに対してデスクトップeコマースは530億米ドルです。さらに、この金額は2025年までにモバイルで570億米ドル、デスクトップで810億米ドルに増加すると予測しています。この成長は、指定された期間内に段ボール梱包箱に対する国の需要が比例して増加することを示すと予想されます。

- カナダのeコマース・インフラは高度に発達しており、米国と密接に統合されています。カナダの主要オンライン小売業者には、アマゾン、ウォルマート、カナディアン・タイヤ、コストコ、ベスト・バイ、ハドソンズ・ベイ、エッツィーなどがあります。

- カナダの消費者は、インターネットでの注文に依存しています。インターネットの消費者売上は、従来の小売売上よりも過去10年間で増加しています。カナダの小売企業の多くは、ワイヤレス技術やインターネットベースのシステムを採用し、企業間および企業対消費者間の関係を改善しています。

- カナダは最もインターネットを利用する国のひとつであり、小売チャネルが大きく混乱する中、消費者は電子商取引を受け入れています。Ascential社のEdgeによると、カナダにおける小売チェーンのeコマース総売上は、2022年に473億米ドルに達します。小売eコマースの売上高は、2027年までに739億米ドルになると推定されています。

北米の二次包装産業の概要

北米の二次包装市場は断片化されており、Amcor PLC、International Paper Company、Reynolds Packaging、Westrock Company、Smurfit Kappa Groupなどの大手企業が存在します。市場の既存企業は、買収、パートナーシップ活動、R&Dの重視、革新的活動などを特徴とする強力な競争戦略を採用しています。

- 2023年3月AmcorとNfinite Nanotechnology Inc.は、Nfiniteのナノコーティング技術をリサイクル可能で生分解性のあるパッケージングに応用するための共同研究イニシアチブを開始。

- 2022年6月:モンディは日東電工のパーソナルケアコンポーネント事業(PCC)を企業価値6億1,500万ユーロ(6億8,117万米ドル)で売却。この売却により、モンディは保有株式を合理化し、持続可能なパッケージングの拡大という戦略目標に集中することが可能となりました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- FMCG産業における需要の増加

- セキュリティとトラッキング・ソリューションの需要増加

- 市場の課題

- ユビキタス規格の欠如、安全性への懸念、過酷な気候条件への耐性の欠如

第6章 市場セグメンテーション

- 製品タイプ別

- 段ボール箱

- 折りたたみカートン

- プラスチック箱

- ラップとフィルム

- その他の製品タイプ

- エンドユーザー産業別

- 食品

- 飲料

- ヘルスケア

- 家電製品

- パーソナルケアと家庭用品

- その他のエンドユーザー産業

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Amcor PLC

- International Paper Company

- Reynolds Packaging

- WestRock Company

- Smurfit Kappa Group

- Berry Global Group Inc.

- Packaging Corporation of America

- Deufol SE

- Mondi PLC

- Tranpak Inc.

第8章 投資分析

第9章 市場の将来

目次

The North America Secondary Packaging Market size is estimated at USD 68.71 billion in 2025, and is expected to reach USD 83.36 billion by 2030, at a CAGR of 3.94% during the forecast period (2025-2030).

The United States and Canada are massive consumer markets, and the population's considerable buying power makes it a lucrative market for all package suppliers. As a result, the North American secondary packaging market is anticipated to grow over the upcoming year due to the growing demand for food packaging, a string of successful e-commerce transactions, and the demand for safety in packaging transportation.

Key Highlights

- The rising use of environment-friendly materials in packaging is driving the secondary packaging market in North America. Packaging that is recyclable, biodegradable, reusable, non-toxic, and has a minimal environmental impact is considered eco-friendly. The need for environment-friendly packaging materials is becoming increasingly apparent to end users, including the food and beverage industry and manufacturers of household care products. Packaging formats like folding cartons and corrugated boxes have no adverse effects on the environment because they are constructed of recyclable and biodegradable materials, such as paperboard.

- The demand for convenience foods is on the rise due to the busy lifestyle of people. As corrugated board packaging keeps moisture from the products and withstands long shipping times, companies are increasingly adopting it to offer customers better outcomes, especially secondary or tertiary packaging. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used once, thereby driving the demand.

- Since the corrugated board is easy to recycle and the pulp and paper industry is already skilled at converting it into new generations of containerboard, it is becoming increasingly common in packaging as sustainability concerns become more relevant across the value chain. Due to these benefits, corrugated protective forms have gained popularity over polymer-based substitutes, such as expanded polystyrene (EPS) foams.

- Additionally, increasing courier and messengers' revenue indicates the use of secondary packagings, such as corrugated boards and folding cartons packaging, in transiting the products from one place to another. According to the US Department of Commerce, in 2021, the US couriers and messengers generated almost USD 137.91 billion in operating revenue. UPS is the largest courier and delivery service provider in the United States, with around 40% of the courier market.

- Secondary packaging still raises environmental questions, but there are also other challenges to solve. In online purchasing, all have encountered the bother and disappointment of receiving a flawed, incomplete, or inaccurate product due to subpar or insufficient secondary packaging. However, since secondary packaging comes after primary packaging, any issues resulting from a stoppage impact the rest of the production line. Production and delivery plans are disrupted by downtime, which also increases product waste and brings labor expenses back into the expense column. Production planning should ideally include anticipating and reducing stoppages through advanced planning.

North America Secondary Packaging Market Trends

Consumer Electronics to Witness Significant Growth

- Consumer electronics firms are being pushed by government and legislation in addition to consumer-driven sustainable packaging. This is notably true in the United States, where legislation for expanded producer responsibility programs, single-use packaging limitations, and other issues is being examined.

- Secondary packaging, such as folding cartons and corrugate boxes, is used for heavy and small electrical component packaging. Corrugated boxes pack consumer products, such as home appliances, refrigerators, HVAC units, etc. Apart from these, smaller electrical components and accessories, such as circuit breakers, tapes, light bulbs, etc., also use paper-based materials for secondary packaging.

- According to Consumer Technology Association, the retail sales of consumer electronics (CE) in the US market increased steadily from 2015 to 2022. According to forecasts, retail sales of consumer electronics are expected to grow by USD 485 billion in the United States in 2023. Revenue from OLED Televisions is expected to reach USD 2.3 billion in 2023.

- A strong need for anti-counterfeiting in electronics packaging drives the North American market. The packaging uses overt and covert technology, such as barcodes, holograms, sealing tapes, and radiofrequency identifying devices, to protect the integrity of items. The rapid growth of e-commerce in emerging economies has benefited the worldwide anti-counterfeit electronics packaging industry.

- Furthermore, environmental-friendly packaging is becoming popular for electrical devices. Government authorities and regulators have made a strong push for the adoption of green packaging. Both brands and customers are becoming more aware of environmentally friendly packaging and the importance of safeguarding the environment from non-biodegradable packaging trash.

Canada Expected to Witness Significant Growth

- The Canadian secondary packaging market was valued at USD 6.79 billion the year before. Corrugated board packaging is an economical way to safeguard and transport various goods. The corrugated board's qualities, such as light weightiness, biodegradability, and recyclability, have made it a vital component in the packaging business. Sealed Air will focus on creating 100% recyclable or reused packaging by 2025. Around 50% of its solutions have already been made with recycled material.

- To improve their presence and position in the market, vendors in Canada have focused on growth, partnership, and collaboration initiatives. Similarly, in December 2022, Titan Corrugated and its associate All Boxed Up were acquired by UFP Packaging, a branch of UFP Industries, a US-based holding firm. The acquired company manufacture standard-sized distributed across the United States via All Boxed Up.

- The country's developing e-commerce market generates demand for corrugated and paper goods, notably from players in the transportation and logistics sectors. Paper-based packaging, which is adaptable and affordable, has been used to carry, protect, and preserve many items.

- According to Worldpay, mobile e-commerce earned over USD 28 billion in Canada in 2021, compared to USD 53 billion from desktop e-commerce. Additionally, it predicts that these amounts will rise to USD 57 billion and USD 81 billion in mobile and desktop sales by 2025. This growth is anticipated to show a proportionate rise in the nation's demand for corrugated packing boxes within the specified time frame.

- Canada's e-commerce infrastructure is highly developed and closely integrated with the United States. The major online retailers in Canada include Amazon, Wal-Mart, Canadian Tire, Costco, Best Buy, Hudson's Bay, and Etsy.

- Canadian consumers rely upon the internet to place orders. Internet consumer sales have risen more in the past decade than traditional retail sales. Most Canadian retail firms have adopted wireless technologies and internet-based systems to improve business-to-business and business-to-consumer relations.

- As Canada is one of the heaviest internet users, consumers have embraced electronic commerce amid a significant disruption in retail channels. According to Edge by Ascential, retail chain e-commerce gross sales in Canada accounted for USD 47.3 billion in 2022. Retail e-commerce sales are estimated to total USD 73.9 billion by 2027.

North America Secondary Packaging Industry Overview

The North American secondary packaging market is fragmented, with the presence of major players like Amcor PLC, International Paper Company, Reynolds Packaging, Westrock Company, and Smurfit Kappa Group. The market incumbents are adopting powerful competitive strategies characterized by acquisitions, partnerships activities, a strong emphasis on R&D, and innovative activities.

- March 2023: Amcor and Nfinite Nanotechnology Inc. launched a collaborative research initiative to test the application of Nfinite's nanocoating technology to improve recyclable and biodegradable packaging.

- June 2022: Mondi sold Nitto Denko Corporation its Personal Care Components business (PCC) for an enterprise value of EUR 615 million (USD 681.17 million). The sale allowed Mondi to streamline its holdings and concentrate on its strategic goal of expanding in sustainable packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defnition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand in FMCG Industries

- 5.1.2 Increased Demand for Security and Tracking Solutions

- 5.2 Market Challenges

- 5.2.1 Lack of Ubiquitous Standards, Safety Concerns, and Inability to Withstand Harsh Climatic Conditions

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Corrugated Boxes

- 6.1.2 Folding Cartons

- 6.1.3 Plastic Crates

- 6.1.4 Wraps and Films

- 6.1.5 Other Product Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Consumer Electronics

- 6.2.5 Personal Care and Household Care

- 6.2.6 Other End-user Industries

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 International Paper Company

- 7.1.3 Reynolds Packaging

- 7.1.4 WestRock Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 Berry Global Group Inc.

- 7.1.7 Packaging Corporation of America

- 7.1.8 Deufol SE

- 7.1.9 Mondi PLC

- 7.1.10 Tranpak Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日