|

市場調査レポート

商品コード

1939719

米国のリバースロジスティクス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)United States Reverse Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のリバースロジスティクス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 154 Pages

納期: 2~3営業日

|

概要

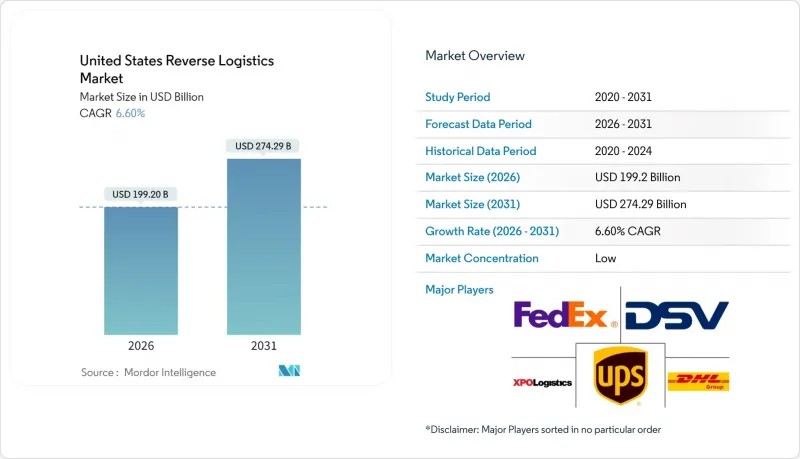

2026年の米国リバースロジスティクス市場規模は1,992億米ドルと推定され、2025年の1,868億7,000万米ドルから成長し、2031年には2,742億9,000万米ドルに達すると予測されています。

2026年から2031年にかけての年間平均成長率(CAGR)は6.6%となる見込みです。

この成長軌道の主な要因は、堅調な電子商取引の成長、電子廃棄物に対する規制当局の監視強化、そして顧客ロイヤルティ獲得のための摩擦のない返品を特徴とするブランド戦略です。返品商品は数百万の分散した住所から発生し、中央処理拠点への迅速な再配置を必要とするため、輸送費が支出の大部分を占め続けています。一方で、ロボティクス、コンピュータービジョン、AI搭載処分エンジンの技術投資により、単価コストが低下し、返品製品が迅速に収益化可能な資産へと転換され、回収率が向上しています。2025年の主要買収事例が示すように、大手物流事業者間の統合が進む中、専用のリバースネットワーク、コールドチェーン資産、コンプライアンス専門知識を有する事業者だけが、この機会を完全に収益化できることが明らかです。

米国リバースロジスティクス市場の動向と洞察

Eコマースの急成長が返品量を増大

オンライン支出の増加は、ほぼ直接的に返品量の増加につながります。小売業者は「ブラケット購入」に頻繁に直面します。これは、買い物客が複数のバリエーションを注文し、その大部分を返品することを想定する行為であり、リバースフローのスピードが購入前のセールスポイントとなっています。主要宅配業者は現在、空車走行距離を最小化するため、ラストマイル配送ルート計画に返品集荷を組み込んでいます。この調整により、滞留時間が短縮され、入荷ドックの混雑が緩和されます。高処理能力のコンベアを備えた返品センターも、休暇後の返品急増に対応するため規模を拡大しており、48時間以内に在庫を再配置することで品切れを防止しています。このサイクルを効率的に運用する全国規模の小売業者は、顧客生涯価値を高めつつ、より多くの運転資金を回収しています。

競争優位性としての寛大な返品ポリシー

かつてはサービスの一環であった寛大な返品期間が、今や購買転換の要となっています。「試してから購入」モデルを創出したD2Cブランドは、顧客満足度を維持するため、数日ではなく数時間以内に処理・返金できるパートナーを求めています。したがって、リバースネットワークは地理的カバー範囲と技術基盤においてフォワードネットワークを模倣し、宅配ロッカー、店頭カウンター、郵送返品チャネルを同一の在庫クラウドに接続します。AI駆動の不正分析は異常な高返品率の顧客を検知し、小売業者が損失率を増加させることなく寛大なポリシーを維持することを可能にします。このバランスを習得したプロバイダーは、アパレルや家電小売業者から長期契約を獲得しています。

高い輸送・取扱コスト

リバース物流ルートは本質的に不均衡であり、トラックが部分的にしか積載されない状態で戻ることが多いため、単位当たりのコストが上昇します。燃料価格の変動がこの課題をさらに深刻化させており、フリート運営者は高価な設備更新を必要とする新たなフェーズ3温室効果ガス基準への対応が求められています。利益率を守るため、プロバイダーは小包を地域のクロスドックに集約し、積載率向上を図るため動的なバックホール契約を交渉します。しかし低価値商品の場合、輸送費だけで再販利益が消えることもあり、量産品は再生品ではなく清算品として処理される傾向にあります。

セグメント分析

2025年時点で、米国リバースロジスティクス市場規模の64.40%を輸送が占めており、価値回収において回収・再配置が最優先事項であることを示しています。小口貨物およびトラック未満貨物輸送業者は、出荷ルートと連動した専用返品レーンを展開し、ネットワーク密度を最大化しています。航空貨物輸送は、特に医療機器業界からの高価値品や温度管理が必要な返品を継続して取り扱っております。倉庫保管は二次的なコストセンターとして続き、主要港湾や州間高速道路近郊のマルチクライアント型施設は、クロスドッキング商品のサイクルタイム短縮に貢献しております。その他の付加価値サービス(修理、再生、等級判定、認証廃棄)は、ブランドが循環型モデルを追求する中で需要が拡大しており、このサブセグメントの2031年までのCAGRを4.65%に押し上げています。輸送とこれらのサービスを組み合わせたプロバイダーは、処分チェーン全体を管理できるため、プレミアム収益を獲得しています。

第二世代施設では、ロボット仕分け、データ消去済みの試験ラボ、EC用写真ブースを統合し、回収品が到着した当日中にリコマースマーケットプレースへ出品する体制が整っています。この変革により、米国リバースロジスティクス市場内で増収が創出され、清算卸業者への外部委託が削減されました。長距離輸送事業者も同様に、ドックサイドでの選別作業を追加し、無駄な走行距離を削減。機能統合が利益率と持続可能性の両面で成果をもたらすことを実証しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の急成長が返品量を増大させております

- 競争上の差別化要因としての寛大な返品ポリシー

- 持続可能性と電子廃棄物規制

- 返品センターにおける自動化とロボティクス

- AIを活用した予測型返品防止分析

- リコマースマーケットプレースにおける収益化

- 市場抑制要因

- 高い輸送・取扱コスト

- オムニチャネル返品における複雑性

- 返品詐欺の増加

- 大型商品における再生・リサイクル能力のボトルネック

- バリュー/サプライチェーン分析

- テクノロジーの展望

- 規制情勢

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 特集- 米国電子商取引業界

- 変化する消費者行動と嗜好に関する調査

- 返品コストが小売業者に与える影響- アナリストの見解

第5章 市場規模と成長予測

- 機能別

- 交通機関

- 道路

- 航空

- その他の輸送手段

- 倉庫業務(保管、流通、集荷)

- その他の付加価値サービス(返品処理、再在庫化、再生、処分)

- 交通機関

- エンドユーザー別

- 消費者・小売業

- ホーム&インテリア

- 医療・医薬品

- FMCG(日用消費財)

- その他のエンドユーザー

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- United Parcel Service(UPS)

- FedEx Corp.

- XPO Logistics

- DSV

- DHL Supply Chain

- C.H. Robinson Worldwide

- Geodis

- Yusen Logistics

- CEVA Logistics

- Kuehne+Nagel

- ShipBob

- United States Postal Service(USPS)

- Excelsior Integrated LLC

- Ryder

- Kenco Logistics

- Yellow Corporation

- RXO Inc.

- ArcBest

- AP Express

- Bluebird Express