屋根用メンブレン:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Roofing Membranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683202

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

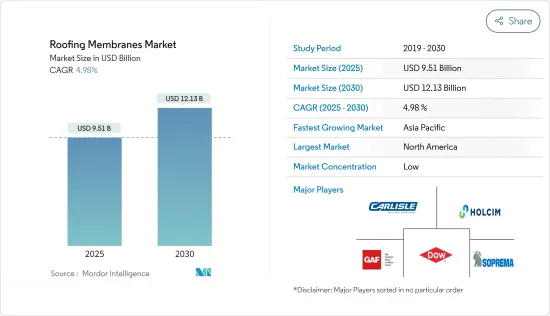

屋根用メンブレン市場規模は2025年に95億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.98%で、2030年には121億3,000万米ドルに達すると予測されます。

主要ハイライト

- 建設プロジェクトにおける軽量材料の採用増加と建設活動の活発化が、屋根用メンブレン市場の成長を促す主要要因です。

- しかし、原料価格の変動や厳しい規制・基準が市場の成長を阻害する可能性が高いです。

- エネルギー効率の高い屋根用メンブレンへの需要の高まりと技術の進歩は、予測期間中に市場に有利な成長機会をもたらす可能性が高いです。

- 北米は建設活動の活発化により屋根用メンブレン市場を独占しています。

屋根用メンブレン市場の動向

市場を独占するのは商業セグメント

- 屋根用メンブレンは業務用途に広く利用されており、その需要は世界の商業建築の急増によって大きく後押しされています。これらの膜は、商業ビルにおいて重要な防水バリアとして機能し、環境要素から建物を保護し、屋根システムの完全性を維持します。

- その強度、耐久性、水に対する不浸透性により、これらの膜は商業施設の屋根用途に好まれる選択肢となっています。

- これらの膜は、工場、鉄道駅、空港、本社、ショッピングセンター、劇場、学校、病院などの商業エリアで使用されています。

- アジア太平洋は、商業建築セグメントで圧倒的な強さを誇っています。この地域では最近、特にインドと中国において、政府の積極的な開発イニシアチブに後押しされ、オフィススペース需要が急増しています。

- 中国国家統計局のデータによると、2022年、中国の商業施設の年間着工面積は約8,155万平方メートルで、前年の1億4,105万平方メートルから減少しました。さらに、2023年末の分譲商業ビルの床面積は6億7,295万平方メートルで、前年比19%増となりました。

- インドでは、床面積76万1,804㎡のオフィスキャンパスの拡大を含むインフォシス・ポーチャラム・オフィス・キャンパスの建設が2023年第3四半期に開始され、2027年第3四半期末までに完成する見込みです。

- 中東では、サウジアラビアビジョン2030やアブダビ経済ビジョン2030など、商業セクターの開発を強化するためのいくつかの政府構想が屋根用メンブレンの消費を大幅に促進するとみられます。

- 様々なホテル建設プロジェクトが屋根用メンブレンの需要をさらに押し上げると予想されます。例えば、観光産業が回復するにつれて、Marriott International Inc.は、ハノイ、ホーチミン市、ダナン、フーコック島を含むベトナムの主要観光地全体で20の高級ホテルとリゾートを発表する予定です。

- Anantara Hotels, Resorts, and Spasは、2025年デビュー予定のブラジルの新リゾート計画を明らかにしました。Anantara Mamucaboは、116室の客室、スイート、プール・ヴィラを備えています。

- 商業施設の建設が増加していることから、商業施設向け屋根用メンブレンの需要は今後数年間で拡大する見込みです。

北米が市場を独占する見込み

- 北米が世界市場で最大のシェアを占めています。米国、カナダ、メキシコなどの国々では、軽量かつ迅速な建設技術の採用が屋根用メンブレンの需要を急増させています。

- 米国は世界最大級の建設産業を誇る。米国国勢調査局によると、2023年の建設総額は19兆7,800億米ドルに達し、2022年から7%増加しました。2024年2月までに建築許可された民間住宅戸数は151万8,000戸に達し、2023年の同時期から2.4%増加しました。

- 米国ではいくつかの新しい商業建築プロジェクトが建設中であり、屋根用メンブレンの需要はさらに増加するとみられます。例えば、2024年1月、インディアナ州政府とMeta Platforms Inc.は、フージャー州に8億米ドルの新しいデータセンターキャンパスを建設するために提携しました。このプロジェクトは2026年までに完成する見込みで、リバー・リッジ・コマースセンターに70万平方フィートの施設を建設します。

- カナダ統計局によると、建築物建設への投資総額は1.7%増加し、2023年10月の19兆4,460億米ドルから2023年11月には19兆7,670億米ドルに増加しました。同期間の住宅建設投資は2.2%増の137億米ドル、非住宅建設投資は0.6%増の60億米ドルでした。

- 2023年、国際貿易庁が報告したメキシコの建設産業は、顕著な価値の上昇を示しました。産業全体の価値は、2022年の1,028億8,000万米ドルから1,205億8,000万米ドルに上昇しました。特にインフラ部門は、2022年の388億3,000万米ドルから2023年には約461億米ドルに急増しました。建設とインフラの両セグメントにおけるこうした上昇基調は、今後数年間、メキシコで調査された市場の需要を促進する構えです。

- したがって、このような建設市場の好材料と軽量材料の採用拡大により、予測期間中、北米では屋根用メンブレンの需要が増加すると予測されます。

屋根用メンブレン産業概要

屋根用メンブレン市場は細分化されています。主要参入企業(順不同)には、Carlisle SynTec Systems、Sika AG、HOLCIM、GAF Inc.、Saint-Gobainなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 建設プロジェクトにおける軽量材料の採用増加

- 建設活動の増加

- その他の促進要因

- 市場抑制要因

- 原料価格の変動

- 厳しい規制と基準

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ別

- 熱可塑性ポリオレフィン(TPO)

- エチレンプロピレンジエンモノマー(EPDM)

- ポリ塩化ビニル(PVC)

- 改質ビチューメン(モッドビット)

- その他

- 設置タイプ別

- 機械的接着

- 完全接着

- バラスト

- その他の設置タイプ

- 用途別

- 住宅用

- 商業施設

- 施設

- インフラ

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Carlisle SynTec Systems

- Dow

- GAF Inc.

- Henry Company

- HOLCIM

- IB Roof Systems

- IKO Polymeric

- Johns Manville

- Kingspan Group

- Owens Corning

- Polygomma

- Sika AG

- Siplast Inc.

- SOPREMA

第7章 市場機会と今後の動向

- エネルギー効率の高い屋根用メンブレンへの需要の高まり

- 技術の進歩

- その他の機会

目次

Product Code: 64123

The Roofing Membranes Market size is estimated at USD 9.51 billion in 2025, and is expected to reach USD 12.13 billion by 2030, at a CAGR of 4.98% during the forecast period (2025-2030).

Key Highlights

- The rising adoption of lightweight materials in construction projects and increasing construction activities are the major factors driving the growth of the roofing membranes market.

- However, fluctuating raw material prices and stringent regulations and standards are likely to hinder the growth of the market.

- Nevertheless, the increasing demand for energy-efficient roofing membranes and advancements in technology are likely to create lucrative growth opportunities for the market during the forecast period.

- North America dominates the roofing membranes market owing to the growing construction activities in the region.

Roofing Membranes Market Trends

Commercial Segment to Dominate the Market

- Roofing membranes are widely utilized in commercial applications, and their demand is largely fueled by a surge in global commercial construction. These membranes serve as a vital waterproof barrier in commercial buildings, shielding them from environmental elements and upholding the roofing system's integrity.

- Due to their strength, durability, and impermeability to water, these membranes have become the preferred choice for commercial roofing applications.

- These membranes are used in commercial areas, such as factories, railway stations, airports, company headquarters, shopping centers, theaters, schools, and hospitals.

- Asia-Pacific is a dominant player in the commercial construction arena. The region recently witnessed a boom in office space demand, particularly in India and China, driven by proactive government development initiatives.

- As per the data from the National Bureau of Statistics of China, in 2022, the annual starting construction of commercial properties in China amounted to around 81.55 million square meters, down from 141.05 million square meters from the previous year. Furthermore, at the end of 2023, the floor space of commercial buildings for sale was 672.95 million square meters, up by 19% over the previous year.

- In India, the construction of Infosys Pocharam Office Campus, which includes the expansion of an office campus with a floor area of 761,804 square meters, was initiated in the third quarter of 2023, and it is likely to be completed by the end of Q3 2027.

- In the Middle East, several government initiatives to bolster the development of the commercial sector, such as Saudi Arabia Vision 2030 and Abu Dhabi Economic Vision 2030, are likely to substantially drive the consumption of roofing membranes.

- Various hotel construction projects are expected to further propel the demand for roofing membranes. For instance, as the tourism industry rebounds, Marriott International Inc. is set to unveil 20 luxury hotels and resorts across Vietnam's prime tourist spots, including Hanoi, Ho Chi Minh City, Da Nang, and Phu Quoc Island.

- Anantara Hotels, Resorts, and Spas revealed plans for a new resort in Brazil, slated to debut in 2025. Anantara Mamucabo will feature 116 guest rooms, suites, and pool villas.

- Given the growth in commercial construction activities, the demand for roofing membranes in commercial applications is poised for growth in the coming years.

North America Expected to Dominate the Market

- North America holds the largest share of the global market. Countries like the United States, Canada, and Mexico have seen a surge in demand for roofing membranes, driven by the adoption of lightweight and swift construction techniques.

- The United States boasts one of the world's largest construction industries. According to the United States Census Bureau, in 2023, the nation's construction value hit USD 19.78 trillion, marking a robust 7% increase from 2022. By February 2024, the number of privately owned housing units authorized by building permits reached 1,518,000, showing a 2.4% uptick from the same period in 2023.

- Several new commercial construction projects are under construction in the United States, which are likely to increase the demand for roofing membranes further. For instance, in January 2024, the government of Indiana and Meta Platforms Inc. partnered to construct a new USD 800 million data center campus in Hoosier State. The project, which is likely to be completed by the year 2026, is a 700,000-square-foot facility at the River Ridge Commerce Center.

- Statistics Canada reported a 1.7% increase in total investment in building construction, climbing from USD 19,446 billion in October 2023 to USD 19,767 billion in November 2023. In the same period, residential spending saw a 2.2% growth, hitting USD 13.7 billion, while non-residential spending rose by 0.6% to USD 6.0 billion.

- In 2023, Mexico's construction industry, as reported by the International Trade Administration, saw a notable uptick in value. The industry's overall worth climbed to USD 120.58 billion, up from USD 102.88 billion in 2022. Specifically, the infrastructure segment surged to about USD 46.10 billion in 2023, a significant rise from USD 38.83 billion in 2022. These upward trajectories in both the construction and infrastructure sectors are poised to fuel the demand for the market studied in Mexico in the coming years.

- Hence, due to such positive factors in the construction market and the growing adoption of lightweight materials, the demand for roofing membranes is projected to increase in North America during the forecast period.

Roofing Membranes Industry Overview

The roofing membrane market is fragmented in nature. The major players (not in any particular order) include Carlisle SynTec Systems, Sika AG, HOLCIM, GAF Inc., and Saint-Gobain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption of Lightweight Materials in Construction Projects

- 4.1.2 Increasing Construction Activities

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Fluctuating Raw Materials Prices

- 4.2.2 Stringent Regulations and Standards

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 By Product Type

- 5.1.1 Thermoplastic Polyolefin (TPO)

- 5.1.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.1.3 Poly Vinyl Chloride (PVC)

- 5.1.4 Modified Bitumen (Mod-Bit)

- 5.1.5 Other Product Type

- 5.2 By Installation Type

- 5.2.1 Mechanically Attached

- 5.2.2 Fully Adhered

- 5.2.3 Ballasted

- 5.2.4 Other Installation Types

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Institutional

- 5.3.4 Infrastructural

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Carlisle SynTec Systems

- 6.4.2 Dow

- 6.4.3 GAF Inc.

- 6.4.4 Henry Company

- 6.4.5 HOLCIM

- 6.4.6 IB Roof Systems

- 6.4.7 IKO Polymeric

- 6.4.8 Johns Manville

- 6.4.9 Kingspan Group

- 6.4.10 Owens Corning

- 6.4.11 Polygomma

- 6.4.12 Sika AG

- 6.4.13 Siplast Inc.

- 6.4.14 SOPREMA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Energy-efficient Roofing Membranes

- 7.2 Advancements in Technology

- 7.3 Other Opportunities

屋根用メンブレン:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日